FED (Federal Reserve System)

The FED (Federal Reserve System) is the central banking system of the United States, made up of the policy-setting FRB (Board of Governors), 12 regional Federal Reserve Banks, and the FOMC that votes on rates — shaping global markets through interest-rate and balance-sheet policy.

The U.S. central banking system — the Federal Reserve System (FED) — often appears in the news simply as "the Fed."

Yet the terms FED, FRB, and FOMC are easy to confuse: who sets policy, who carries it out, and who actually votes? This article maps out the FED's structure, functions, and decision-making process, and explains how it influences global markets through interest rates and balance-sheet operations, so you can quickly grasp what the "U.S. central bank" really is.

- "FED" is the entire Federal Reserve System, "FRB" is its core Board of Governors, and "FOMC" is the committee that actually votes on policy

- The FRB has 7 governors; its Chair leads the FOMC and is the most-watched figure in global finance

- The FOMC has 12 votes: 7 governors + 5 regional Fed presidents (New York permanent, the other 4 rotate), deciding the policy rate and balance-sheet size

- The FED's dual mandate is maximum employment and price stability, making CPI and non-farm payrolls the core data for decisions

- Three policy tools: the policy rate, open-market operations (QE/QT), and forward guidance

- 1. A Quick Guide to the U.S. Central Bank: FED vs FRB

- 2. The Structure of the Federal Reserve System: FRB and the 12 Reserve Banks

- 3. What is the FOMC? Members, Voting, and Meeting Process

- 4. How the FED Moves Markets: Policy Tools and Transmission

- 5. The FED's Impact on Markets: FX, Equities, Bonds, and Commodities

- 6. Frequently Asked Questions (FAQ)

- 7. Summary: The Practical Points for Reading the FED

1. A Quick Guide to the U.S. Central Bank: FED vs FRB

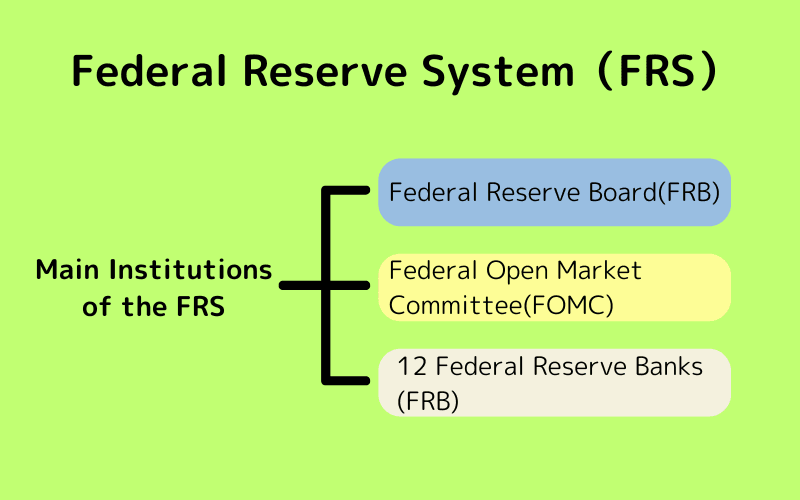

The Federal Reserve System (FED) is the central banking system of the United States.

Its core institution is the Federal Reserve Board (FRB), which sets monetary policy and supervises the country's 12 Federal Reserve Banks. The FOMC (Federal Open Market Committee), formed by the FRB and the regional bank presidents, is the body that actually decides the direction of policy.

Why a "system" rather than a single central bank

The U.S. design principle is decentralisation and checks and balances. The FED is not a single central bank but a system made up of the FRB in Washington and 12 Federal Reserve Banks across the country.

- The FRB in Washington: sets national-level policy.

- The 12 regional Reserve Banks: handle regional financial stability and policy execution.

This "system" design keeps national policy consistent while preserving local flexibility, and avoids an over-concentration of power.

The FED's dual mandate

U.S. law gives the FED two explicit goals:

- Maximum employment: ensuring growth keeps creating jobs.

- Price stability: containing inflation to preserve purchasing power.

To balance these, the FED uses interest-rate adjustments (hikes and cuts), balance-sheet management (QE / QT), and forward guidance.

2. The Structure of the Federal Reserve System: FRB and the 12 Reserve Banks

The system follows a two-layer design: central decision-making plus regional execution. The FRB handles policy and supervision, while the 12 Reserve Banks carry out regional operations and market actions.

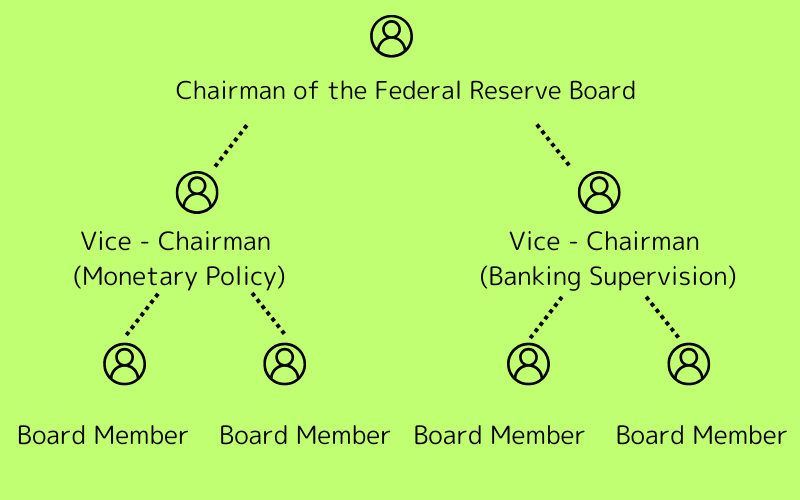

The FRB (Federal Reserve Board)

The FRB (Federal Reserve Board) is the core decision body of the Federal Reserve System, responsible for setting monetary policy and overseeing the financial system.

- Composition: 7 governors (including 1 Chair and 2 Vice Chairs). Governors serve 14-year terms; the Chair and Vice Chairs serve 4-year terms.

- Appointment: nominated by the President and confirmed by the Senate.

- Main duties: framing the monetary-policy framework, bank-supervision standards, and the payment/clearing system, and maintaining financial stability.

The 12 regional Federal Reserve Banks

The 12 Federal Reserve Banks are the FED's regional execution arms, spread across the major economic districts.

- Distribution: located in 12 districts (e.g. New York, Chicago, San Francisco), structured as joint-stock entities.

- Functions: managing district banks' required reserves; providing payment and clearing services; conducting regional economic research; and supporting policy execution (such as market operations).

- FOMC role: each president may attend FOMC meetings; the New York Fed president is a permanent voting member, while the other 4 voting seats rotate among the remaining 11 banks.

Division of responsibilities

- FRB (Washington): sets policy goals and supervisory rules — the hub of the system.

- New York Fed: executes open-market operations (buying/selling Treasuries and MBS) and manages the SOMA portfolio, making it the key unit for putting policy into practice.

3. What is the FOMC? Members, Voting, and Meeting Process

The FOMC (Federal Open Market Committee) is the top decision body for U.S. monetary policy, setting the direction of the policy rate and open-market operations. In other financial systems, it corresponds to the policy-making bodies of other central banks, for example:

| Country/Region | Central Bank | Abbreviation |

|---|---|---|

| United States | Federal Reserve Board | FRB |

| Taiwan | Central Bank of the R.O.C. | - |

| Hong Kong | Hong Kong Monetary Authority | HKMA |

| Japan | Bank of Japan | BOJ |

| Singapore | Monetary Authority of Singapore | MAS |

Composition and voting

- 12 voting members: 7 FRB governors + 5 regional Fed presidents (New York permanent, the other 4 rotating).

- The Chair leads the meeting, and decisions pass by simple majority.

Meeting rhythm

- 8 scheduled meetings a year (usually two days each).

- On day two, the policy statement and (at certain meetings) the dot plot / economic projections (SEP) are released, followed by a press conference; the minutes come out about three weeks later.

For the exact schedule, see the FRB website.

Documents and output

- Policy statement: the current decision and forward guidance.

- SEP / dot plot: projections for GDP, inflation, unemployment, and the terminal rate.

- Minutes: a fuller account of the discussion and the balance of risks.

Further reading: A deep dive into the FOMC — schedule and outlook

4. How the FED Moves Markets: Policy Tools and Transmission

The FED never tells the market directly that "stocks will rise" or "the dollar will fall." Instead, it uses a set of tools to influence funding costs, liquidity, and expectations, which then transmit indirectly to financial markets and the real economy.

Tool 1: The policy rate (federal funds rate)

- Central role: the anchor for short-term rates.

- Transmission: it affects banks' borrowing costs, then household and business lending rates, then consumption and investment.

- Market reaction: changes in the discount rate quickly feed into equity valuations, bond prices, and exchange rates.

Tool 2: Balance-sheet operations (QE / QT)

- QE (quantitative easing): buying Treasuries and MBS to lower long-term rates and release liquidity.

- QT (quantitative tightening): shrinking the balance sheet to withdraw liquidity and push long-term rates up.

- Market reaction: QE tends to lift risk assets, while QT tightens financial conditions.

Tool 3: Forward guidance and daily liquidity management

- Forward guidance: shaping expectations of future rates through public statements.

- Standing tools: such as the overnight reverse repo (ON RRP) and the discount window, keeping short-term rates within the policy band.

- Market reaction: steadying or steering sentiment so rates don't drift far from the policy target.

These tools form the "bridge" between the FED and markets. The next section looks at how they play out across different markets.

5. The FED's Impact on Markets: FX, Equities, Bonds, and Commodities

Although policy is led by the FRB and decided by the FOMC, markets usually use "the FED" as shorthand for the overall stance. Its rates, QE/QT, and guidance ripple through funding costs and expectations into FX, equities, bonds, and commodities.

FX: dollar strength and capital flows

- Rate differentials: hikes or a hawkish turn tend to lift the US dollar; cuts or a dovish turn weigh on it.

- Risk sentiment: as the global reserve currency, the dollar can strengthen on safe-haven demand even when the FED is dovish.

Bonds: the yield curve and credit spreads

- Hikes / hawkish: yields rise, long-bond prices fall, and the curve flattens or inverts.

- Cuts / dovish: long-term yields fall and duration assets benefit; credit spreads often narrow.

Equities: valuations and sector rotation

- Rates drive valuations: hikes raise the discount rate and pressure growth stocks; cuts lift the valuation anchor.

- Allocation shifts: easing lifts risk appetite and high-beta sectors; tightening favours defensives and financials.

Commodities: the dollar and demand

- Dollar effect: a stronger dollar weighs on dollar-priced commodities; a dovish stance is often bullish for gold and oil.

- Demand-side: if easing fuels a recovery, demand for energy and industrial metals picks up.

Four-market quick-reference

| Market | Hawkish (hikes/tightening) | Dovish (cuts/easing) |

|---|---|---|

| FX | Dollar strengthens, capital flows to the US | Dollar weakens, capital flows to higher-yield markets |

| Bonds | Yields up, long-bond prices down | Long-bond prices up, credit spreads narrow |

| Equities | Valuations compress, growth stocks pressured | Valuation anchor rises, growth/high-beta benefit |

| Commodities | A strong dollar weighs on gold and oil | A weak dollar and recovery support raw materials |

The FED's stance is not simply "bullish" or "bearish" for one market — it moves all four at once through different channels. What really drives prices is the gap between the policy tone and market expectations.

6. Frequently Asked Questions (FAQ)

Q1. How are the FED, FRB, Federal Reserve Banks, and FOMC different?

| Term | Common name | One-line role | Key feature |

|---|---|---|---|

| FED | Federal Reserve System | The umbrella name for the U.S. central banking system | FRB + 12 Reserve Banks + FOMC |

| FRB | Federal Reserve Board | Sets the policy framework and supervises banks | In Washington, 7 governors; the Chair (e.g. Powell) is the market focal point |

| Federal Reserve Bank | District/regional Fed | Regional execution — payments, clearing, research | 12 banks; the New York Fed runs open-market operations |

| FOMC | Federal Open Market Committee | The body that actually decides rates and QE/QT | 12 votes: 7 governors + 5 regional presidents (NY permanent, others rotate) |

A simple analogy: the FED is the whole company, the FRB is the head-office board, the 12 Reserve Banks are the branches, and the FOMC is the board meeting that takes the final vote.

Q2. What is the "dual mandate" and why does it matter?

The Federal Reserve Act requires the FED to pursue maximum employment and price stability at the same time. These can be in tension, so the FED constantly balances supporting jobs against containing inflation. Core CPI, Core PCE, and the unemployment rate sit at the centre of every policy debate.

Q3. Why do headlines sometimes treat "FRB" as the U.S. central bank?

Because the FRB is the FED's core decision body and its most visible interface — its Chair speaks for the system. Strictly, though, rate decisions and the scale of QE/QT are voted on by the FOMC, not the FRB alone.

Q4. Are FED decisions made by the FRB or the FOMC?

The policy framework and bank supervision belong to the FRB, but the actual votes on rates and asset purchases happen in the FOMC. To read the FED's stance, markets watch the FRB Chair, the rest of the Board, and the regional presidents together.

Q5. How do I track FED policy signals in practice?

- Documents: the policy statement, minutes, and dot plot / SEP.

- Data: core inflation, employment/unemployment, wages, and financial-conditions indices.

- Officials' remarks: voting members' views matter most; a hawkish member softening is often the earliest sign of a pivot.

7. Summary: The Practical Points for Reading the FED

The FED is a decentralised central-banking system: the FRB sets the framework, the 12 regional banks execute operations, and the FOMC takes the final decisions. Through rate changes, QE/QT, and forward guidance, it shapes funding costs, liquidity, and expectations.

For investors, the key is to read the FED's documents, data, and officials' tone — and to gauge the gap between the policy stance and market expectations, which is what really drives market moves.

Further Reading

- What is the FOMC? Explained

- Quantitative Easing (QE)

- Policy Interest Rate

- What is Monetary Policy?

- U.S. Economic Indicators Calendar

Titan FX Research. We produce investor-education content across forex, precious metals, energy, indices, US equities, and crypto, helping readers interpret monetary-policy news and turn it into trading decisions.

Primary Sources (by Category)

- Central bank: Federal Reserve Board, FOMC statements

- District banks: New York Fed (open-market operations)

- Macro data: BEA, BLS