Inflation

Inflation is the sustained rise in the general price level, eroding the purchasing power of money over time. Most central banks target ~2% annual inflation as the sweet spot — above it signals overheating, below it risks deflation.

Inflation is one of the core phenomena of modern economics, touching every purchase we make, every paycheque we earn, and every investment return we count on. As prices quietly rise, the purchasing power of money quietly falls.

But what exactly is inflation? Why do central banks around the world target a 2% inflation rate? Should we be worried, or reassured?

This article walks through inflation from the ground up: definition, mechanics, drivers, and impacts, with plain-English answers to the questions newcomers ask most. Whether you are a student, a salaried professional, or an investor, this is a foundational primer worth keeping close.

- Inflation = sustained rise in prices that erodes the purchasing power of money.

- Impact is asymmetric: savers and fixed incomes lose; debtors and real-asset holders gain.

- Three main drivers: cost-push, demand-pull, and currency-depreciation (imported) inflation.

- Why 2% target: to dodge the deflation trap and keep policy room for central banks.

- The new normal calls for information judgement, flexible allocation, and resilience.

1. What is Inflation? Definition and Concept

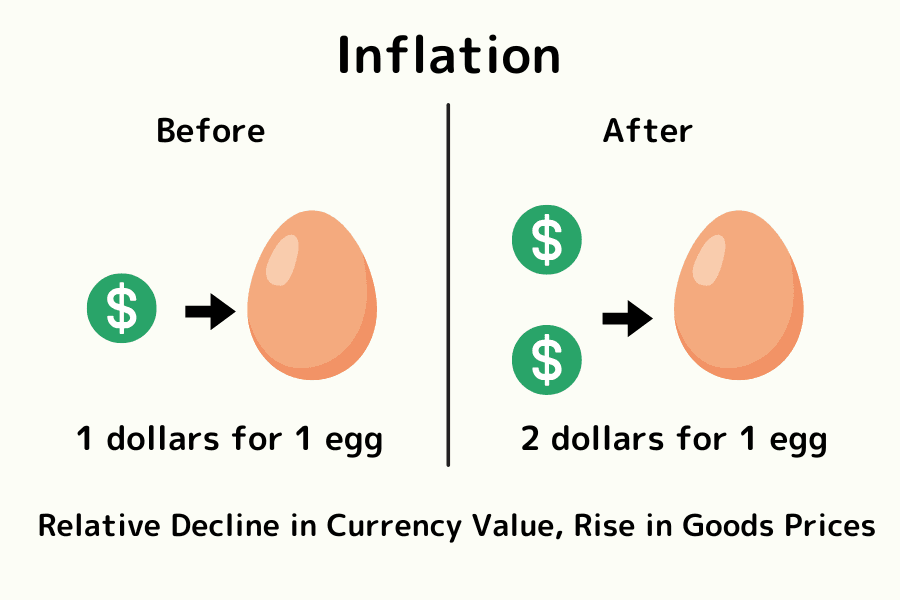

Inflation refers to the sustained, long-term rise in the overall price level of goods and services, resulting in a decline in the real purchasing power of money. As money depreciates, the same unit of currency buys fewer goods or services over time.

The most common gauge of inflation is the inflation rate, typically expressed as an annual percentage. It captures the average rate at which prices rise across the economy and reflects the speed at which money is losing value.

For example:

If $1 bought you two eggs last year but only one egg today, prices have risen 100% — meaning the inflation rate is 100%.

Inflation does not just affect daily consumption — it ripples into the value of savings, investment returns, corporate cost structures, and policy interest rates.

Moderate inflation is generally a sign of healthy economic activity, encouraging consumption and investment. By contrast, excessive inflation — such as hyperinflation — can cause living costs to spiral and asset distributions to distort, doing long-term damage to the broader economy.

2. Pros and Cons of Inflation

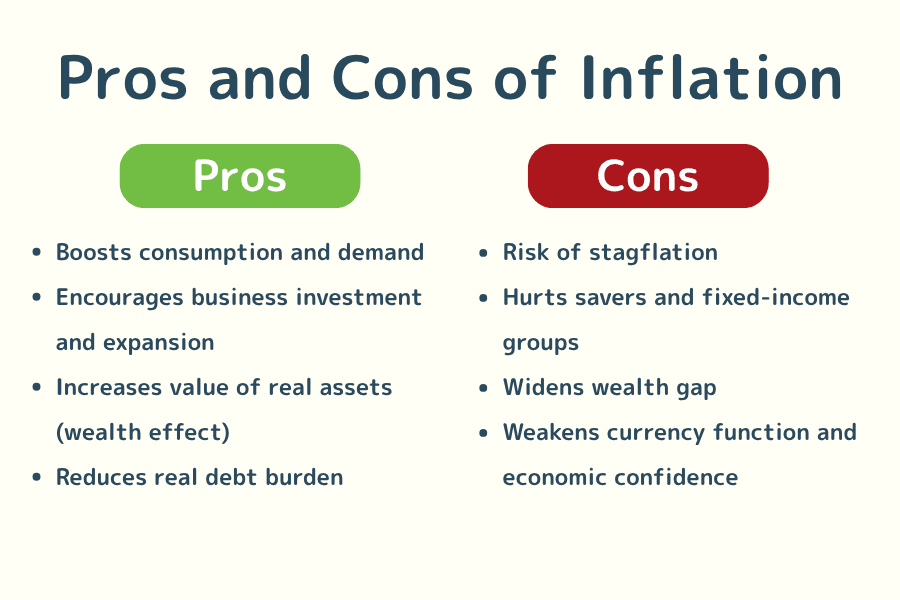

Inflation is a double-edged sword. When mild and well-controlled, it supports economic growth and corporate expansion; when it spirals, it erodes consumer purchasing power, eats into savings, and produces asset misallocation and social inequality.

The Upside: Moderate Inflation Lubricates the Economic Cycle

- Stimulates consumption and demand

- Encourages corporate investment and capacity expansion

- Lifts real-asset values, supporting wealth accumulation

- Reduces the real burden of debt

Stimulates consumption and demand

A modest inflationary trend leads people to expect prices to keep rising, which encourages them to bring purchases forward rather than postpone them. That dynamic boosts consumer demand and is a meaningful lever in domestic-demand-driven economies.

Encourages corporate investment and capacity expansion

When prices are gradually rising, businesses are more willing to invest in capital equipment and R&D because their selling prices and profit margins are likely to expand in tandem. This contributes positively to job creation and productivity.

Lifts real-asset values, supporting wealth accumulation

In inflationary periods, real assets such as land, real estate, and equities tend to drift higher, lifting household wealth perception and feeding further spending and investment behaviour. This is the well-known "wealth effect."

Reduces the real burden of debt

For borrowers, paying back loans in tomorrow's "cheaper" inflated currency means a lighter real repayment. That can ease debt pressure on companies and governments, freeing up capital to recirculate into the productive economy.

The Downside: Excessive Inflation Undermines Economic Stability

- Stagflation risk

- Punishes savers and fixed-income groups

- Widens inequality and forces asset redistribution

- Damages the functions of money and economic trust

Stagflation risk

When prices rise but growth slows and unemployment stays elevated, the economy enters a dangerous combination of high inflation and weak growth — stagflation. Real household incomes contract, corporate profits compress, and traditional policy levers struggle to respond.

Punishes savers and fixed-income groups

In a high-inflation environment, the real purchasing power of cash, bank deposits, and fixed-income bonds declines. That is particularly painful for retirees and conservative investors who depend on savings.

Widens inequality and forces asset redistribution

Wealthier households tend to hold more inflation-resilient assets (property, equities), while lower-income households rely more on wages and cash. As inflation runs, the rich-get-richer dynamic intensifies and the gap widens.

Damages the functions of money and economic trust

The three core functions of money — measure of value, store of value, and medium of exchange — can all be eroded by inflation.

| Function | What goes wrong |

|---|---|

| Measure of value | Unstable prices garble pricing signals and disrupt rational comparisons |

| Store of value | Real purchasing power of savings declines, making wealth preservation harder |

| Medium of exchange | In severe inflation, barter or foreign-currency transactions can re-emerge |

Bottom line: moderate inflation supports investment, employment, and wealth growth, but rapid or persistent inflation does serious damage to economic stability and personal finances. Understanding both sides early is the key to navigating inflationary periods.

3. Main Causes of Inflation

Inflation drivers can be grouped into three broad categories: cost-push, demand-pull, and currency-depreciation / imported inflation. Below are the underlying mechanics and real-world examples for each.

Rising Commodity Prices (Cost-Push Inflation)

When raw materials such as oil, natural gas, wheat, copper, or lithium become more expensive, production costs across manufacturing and services rise in tandem and are eventually passed through to consumer prices, creating economy-wide inflation.

- For instance, the 2022 Russia–Ukraine war disrupted global energy and grain supply, sent oil and food prices soaring, and triggered inflation crises in many economies.

- Extreme weather (droughts, frosts) likewise cuts agricultural output and pushes up food prices.

Loose Fiscal and Monetary Policy (Demand-Pull Inflation)

When governments deploy large-scale spending — tax cuts, cash transfers, infrastructure programmes — or central banks pursue rate cuts and quantitative easing (QE), the money supply expands rapidly and market liquidity surges.

- If demand growth outpaces the economy's ability to expand supply, the prices of goods and services rise.

- During the 2020 COVID-19 episode, for example, multiple rounds of US fiscal stimulus combined with ultra-low interest rates pushed up housing, vehicle, and commodity prices.

Falling Sovereign Credit and Currency Depreciation (Imported Inflation)

When international markets lose confidence in a country's fiscal discipline or political stability, capital can flee, leading to a sharp depreciation of the domestic currency. Imports become more expensive, and that pass-through lifts the broader price level.

- Emerging markets such as Argentina and Türkiye have repeatedly experienced this combination of currency weakness and high inflation.

- Economies that rely heavily on imported raw materials or energy (Japan, for example) are particularly sensitive to currency moves.

Summary Table: Three Categories of Inflation Drivers

| Driver | Mechanism | Representative example |

|---|---|---|

| Commodity price up | Supply-constrained raw materials raise cost | 2022 energy and food crisis |

| Policy-led | Government and central-bank stimulus boost aggregate demand | Pandemic-era QE and cash transfers |

| Credit risk | Currency depreciation lifts import prices | Argentina peso crisis, lira slide |

Practical observation: these drivers often coexist, especially in today's globally interconnected markets where geopolitical events and policy shifts can transmit rapidly through the price system.

4. Inflation Q&A

Q1: What is hyperinflation, and why does it happen?

Hyperinflation is an extreme state in which prices spiral upward in a very short period and the currency loses almost all its value, with annual inflation rates running into the hundreds, sometimes thousands of percent.

Common drivers include:

- Massive money printing to plug fiscal deficits

- Sovereign credit collapse or political turmoil

- Severe supply-chain breakdowns or war

Historical episodes:

- 1920s Weimar Republic (Germany): war reparations and money printing produced runaway hyperinflation

- 2000s Zimbabwe: annual inflation rate at one point exceeded 100 million percent

- More recently, Venezuela: repeated currency redenominations have failed to contain price increases

In such extremes, people switch to foreign currency, gold, or even barter, and money's normal functions collapse.

Q2: How is inflation different from deflation?

| Comparison | Inflation | Deflation |

|---|---|---|

| Price trend | Goods and services prices keep rising | Goods and services prices keep falling |

| Purchasing power | Falls (same money buys less) | Rises (same money buys more) |

| Consumer behaviour | Encourages bringing purchases forward | Encourages delaying purchases |

| Investment | Asset values rise; appetite increases | Returns weaken; capital turns conservative |

| Economic risk | Borrowers gain, lenders lose | Corporate profits drop, unemployment rises |

Note: Deflation may look attractive to consumers, but if it persists it depresses corporate revenues and employment, ultimately hurting the broader economy.

Q3: Who does inflation hurt the most?

Although inflation affects everyone, the impact is uneven across groups:

- Salaried workers: pay rises lag price rises, eroding real income.

- Retirees and depositors: people relying on cash or fixed-income assets see real wealth shrink.

- Lenders/creditors: receive back money worth less than what they lent.

- Lower-income households: spend a larger share of income on essentials, so inflation directly compresses their living standards.

- Borrowers/debtors: real repayment burden falls.

- Holders of real assets: real estate and equities tend to appreciate during inflation.

Q4: Why do central banks "tolerate" or even target a positive inflation rate?

Most central banks — the Federal Reserve, European Central Bank, Bank of Japan and others — set an inflation target around 2% rather than zero.

The reasons:

- Avoiding deflation risk: inflation that is too low — let alone deflation — drags economies into stagnation.

- Supporting wage and profit growth: moderate inflation encourages corporate investment and wage rises.

- Preserving policy room: a positive inflation rate gives central banks more room to cut or raise rates when needed.

Bottom line: moderate inflation is a sign of a normally functioning economy. Problems show up at the extremes — too high or too low.

5. Conclusion: Inflation as the New Normal and the Importance of Economic Resilience

Inflation is no longer a one-off anomaly tied to specific events. Geopolitical conflict, supply-chain reorganisation, demographic shifts, and the energy transition give price pressures an increasingly structural character — quite different from the short, cyclical episodes of the past.

That means: future inflation is likely to be more complex, more recurrent, and central banks will have less room to manoeuvre.

For individuals and businesses alike, the practical response is not to wait for "the low-inflation era to return," but to recognise and accept volatility as a baseline of the economic environment. In that environment, three capabilities become especially important:

- Information judgement: the ability to quickly distinguish the substance and impact of inflation data and policy moves.

- Flexible asset allocation: not concentrating capital in a single asset class, building inflation resilience across currencies and instruments.

- Mental and financial resilience: maintaining a steady mindset and a financial buffer when prices and markets are noisy.

Inflation is not just an economic indicator; it reflects deeper structural change and reminds us that wealth-building rests as much on understanding risk and adapting to change as on chasing returns. To master inflation is, in effect, to take ownership of one's economic future.

Further Reading

- Monetary Policy — The core policy framework central banks use to maintain price stability and promote employment.

- Raise Interest Rates — The standard policy response to elevated inflation pressure.

- Cut Interest Rates — The policy option in deflationary or slowdown environments.

- GDP (Gross Domestic Product) — Alongside inflation, a fundamental macro indicator of economic health.

- Unemployment Rate — A labour-market indicator closely tied to inflation through the Phillips curve.

- Asset Allocation — Portfolio management thinking for an inflationary era.

The Titan FX Research team covers global macroeconomic indicators, foreign exchange (FX), commodities (oil, precious metals, agriculture), equity indices, US stocks, and crypto assets, producing educational content for investors and traders.

Primary Sources by Category

- Official data and regulators: U.S. Bureau of Labor Statistics — Consumer Price Index (CPI); Federal Reserve — "Why does the Federal Reserve aim for inflation of 2 percent over the longer run?"; European Central Bank — "Our inflation target"; Bank of England — "Monetary Policy Report"; Bank of Japan — "Price Stability Target".

- International institutions and research: International Monetary Fund (IMF) — World Economic Outlook; IMF Finance & Development — "Inflation: Prices on the Rise"; Bank for International Settlements (BIS) — Annual Economic Report; OECD — Consumer Price Indices statistics.

- Media and historical references: Bloomberg; Reuters; Federal Reserve History — "The Great Inflation (1965-1982)"; hyperinflation case studies — Weimar Republic (1921-1923), Zimbabwe (2007-2008), Venezuela (2016-), recent Argentina and Türkiye inflation episodes.