Slippage

Slippage is the difference between an order's actual execution price and its expected price, and it tends to occur when markets move sharply or liquidity is thin. It is a hard-to-predict hidden trading cost that can work against you — and occasionally in your favour.

Slippage can't be eliminated entirely, but when it strikes — and how hard — is far from random: it tends to spike around major data releases, the market open and close, and thin-liquidity sessions. Grasp those patterns, and a hidden cost becomes something you can plan around.

This article explains the definition of slippage, its common causes, how it compares with the spread, and how to handle it in practice — helping you understand it precisely and optimise your execution and risk control.

- What slippage is, and positive vs negative slippage

- Main causes: thin liquidity, volatility, execution delay, gaps

- Market traits across forex, stocks, futures, and crypto

- Slippage vs spread: the cost-structure breakdown

- Risk control: MT4/MT5 deviation, sessions, limit orders

1. What Is Slippage? Definition and Common Types

Slippage is a common phenomenon in financial trading: a price deviation that appears between the moment an order is submitted and the moment it is actually filled. Put simply, it is the gap between your expected order price and the executed price.

It typically occurs when the market moves quickly or liquidity is insufficient — for example during economic data releases, major event shocks, or periods of very thin volume. Slippage can add cost, but it can also produce an unexpected gain, depending on the direction of the fill and the price move.

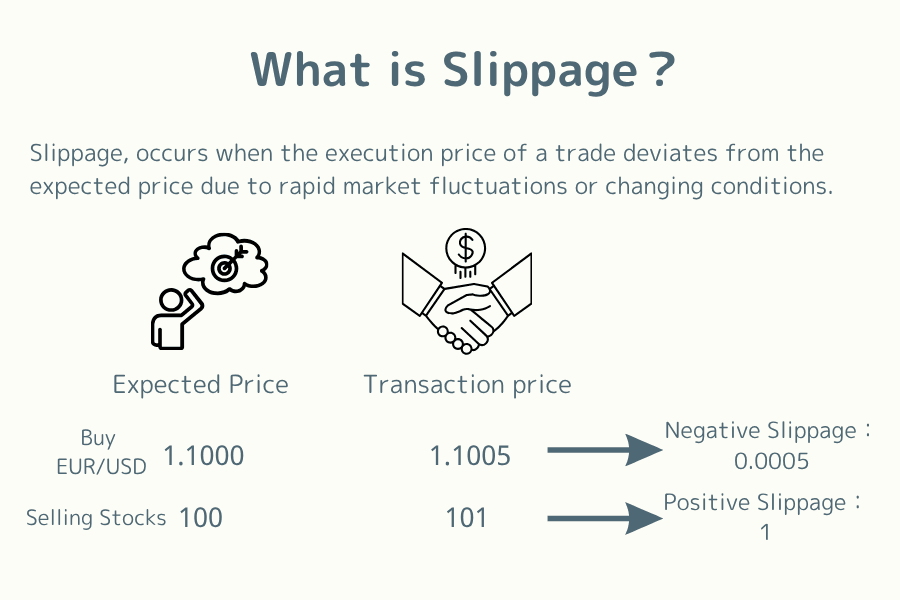

Positive Slippage

When the actual execution price is better than expected, the result is positive slippage. For instance, you intend to buy at 1.1000 but are filled at 1.0995 — cheaper than expected, which works in your favour.

This often appears when sell orders fill in a high-volatility market, or when price slides quickly in a favourable direction during high-liquidity hours.

Negative Slippage

When the actual execution price is worse than expected, it is negative slippage. For example, you expect to sell at 1.1000 but are filled at 1.0990 — a loss of 10 points per unit, an unfavourable outcome.

Negative slippage commonly occurs around major news releases or violent market swings, and the risk is even higher when using market orders.

Slippage essentially reflects the gap between execution speed and liquidity — an easily overlooked yet highly influential variable in trading cost.

2. Why Does Slippage Happen? Common Causes

Slippage is usually tied to the market environment, technical conditions, and trading strategy. The four main drivers are:

- Factor 1: Sharp market volatility

- Factor 2: Insufficient liquidity

- Factor 3: Platform execution delay

- Factor 4: Oversized orders

Factor 1: Sharp Market Volatility

When major economic events are released (rate decisions, non-farm payrolls, central-bank policy statements), prices can jump within a very short window, so orders cannot fill at the original quote.

This is most common during high-volatility windows in the forex and cryptocurrency markets, where market orders are especially exposed.

Factor 2: Insufficient Liquidity

When the order book of a market is too thin — for example minor currency pairs, low-market-cap crypto, or the Asian overnight session — the lack of counterparties can create price gaps and slippage.

Even without violent price moves, sparse executable quotes alone can push fills beyond the expected price.

Factor 3: Platform Execution Delay

A platform's infrastructure, order-matching speed, and the stability of the client's network all affect the timing of actual execution. If processing is slow or there is network latency, price can change in transit and produce slippage.

Factor 4: Oversized Orders

When a single order exceeds the depth the market can absorb in the short term (such as 100 lots at once), the market matches against the next layer of liquidity, so the average fill price drifts away from the initial quote.

Understanding the causes of slippage helps investors pick more suitable trading sessions and order tactics, further optimising cost and execution efficiency.

3. How Slippage Behaves Across Different Markets

Although slippage is a universal trading phenomenon, its frequency and potential impact differ across products and market structures. Here are the three main markets:

Forex Market

As the world's largest and most liquid market, forex carries relatively low slippage risk most of the time. However, during high-volatility events (such as the U.S. non-farm payrolls, Fed rate decisions, or CPI releases), even major pairs like EUR/USD and USD/JPY can show noticeable slippage.

In addition, low-liquidity windows (such as the handover from the New York close to the Tokyo open) can produce price jumps due to thin quotes.

Cryptocurrency Market

Because it trades 24 hours with no centralised matching mechanism, slippage is more common in crypto. The risk is higher in particular when:

- Minor coins (such as newly listed altcoins) have low volume and prices are easily moved by small flows

- High-leverage contract platforms experience execution delays or disconnections

- Sudden news (regulatory action, exchange security incidents) triggers panic selling

Even in mainstream coins like BTC or ETH, price can slip past the expected fill in an instant during news-driven moves.

Equities and Stock-Index Market

Slippage in equities tends to appear in these situations:

- Small-cap or thinly traded stocks have shallow order books and are easily moved by a single large order

- At the opening bell (especially U.S. and Hong Kong opens), a flood of simultaneous orders amplifies slippage risk

- ETFs, index futures, and other derivatives slip in sync during market volatility, particularly those tracking emerging-market indices (such as Malaysia's KLCI or Vietnam's VN-Index)

Slippage risk across markets can be anticipated by analysing volume structure and liquidity traits, helping you choose the right entry timing and product.

4. Slippage vs Spread: The Trading-Cost Structure

In trading, slippage and spread are often confused, yet they are two cost sources of different origin. Understanding the difference helps investors assess real returns and control risk.

Cost Comparison Table

| Cost Type | Definition | Predictable? | Main Cause |

|---|---|---|---|

| Spread | The difference between the Ask and the Bid | Predictable | Broker quoting model and market liquidity |

| Slippage | The gap between the actual fill and your expected order price | Unpredictable | Price jumps, execution delay, liquidity gaps |

| Commission | A fixed or proportional fee a broker charges per trade | Predictable | Set by the broker's fee schedule, usually scaled to volume |

Key Points

- Spread can usually be observed in advance on the platform; it is part of the quote itself.

- Slippage arises at the execution stage and is hard to predict, especially in high-volatility or low-liquidity conditions.

- Commission is an operating cost — transparent and controllable — and is common with ECN-model brokers.

Looking only at the spread makes it easy to overlook the "hidden cost" created by slippage and execution quality. Precise cost management should evaluate all three together.

5. Effective Ways to Reduce Slippage Risk

Slippage cannot be eliminated entirely, but strategic adjustments can sharply reduce its impact and improve stability and cost control.

Use Limit Orders to Control the Fill Price

A limit order sets an explicit upper or lower fill price, avoiding an unfavourable fill caused by a violent move. It may go unfilled if price never reaches the level, but it effectively prevents negative slippage.

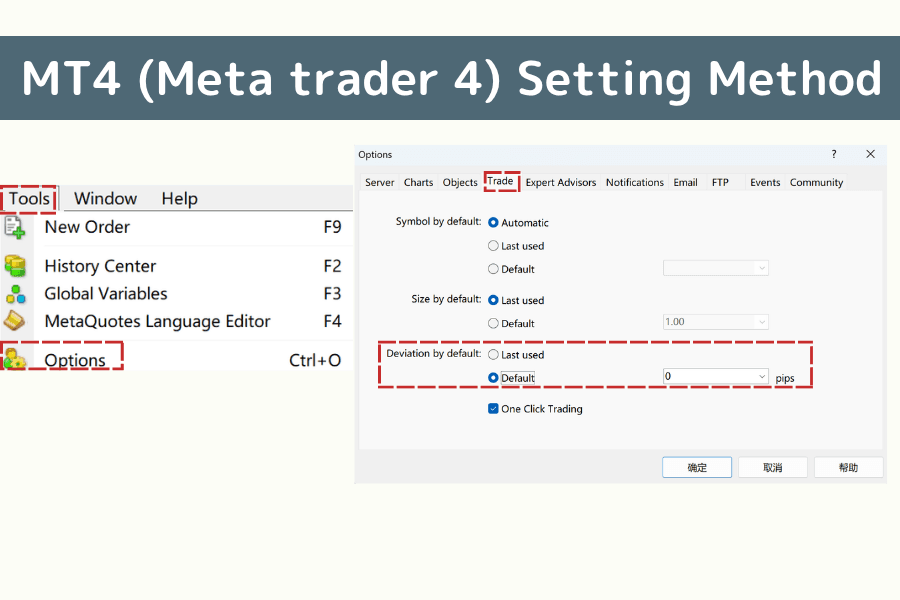

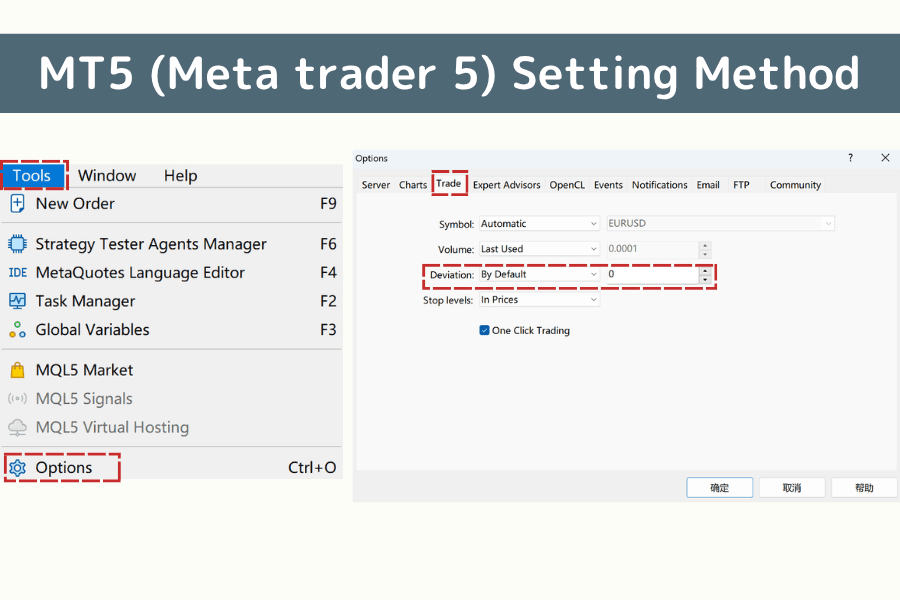

At Titan FX you can trade on the MT4 or MT5 platforms. Below is how to set the allowable deviation range on each.

MT4 (Meta Trader 4) Setup

Go to "Tools" - "Options" - "Trade", select the default value under "Deviation by default", and set the allowable deviation range on the right.

MT5 (Meta Trader 5) Setup

Go to "Tools" - "Options" - "Trade", select "By Default" under "Deviation", and set the allowable deviation range.

Avoid Trading During High-Volatility Windows

Major economic releases (non-farm payrolls, central-bank rate decisions) and the moments around the market open are high-risk windows for slippage; it is best to place orders after volatility eases, when quotes are stable.

Titan FX offers a free indicators tool

Titan FX provides economic-data indicators for major countries worldwide, including the United States, Europe, Japan, and China. You can search by release time, country, and importance.

The economic calendar is a practical tool presented in calendar form, gathering the economic indicators and key data released each day — rate decisions, unemployment, PMI and more — with forecast, actual, and importance levels.

Using the economic calendar, traders can anticipate windows of potential volatility, effectively sidestep high-slippage moments, and optimise entry and exit strategy.

Choose High-Liquidity Instruments

Trading major pairs (such as EUR/USD), popular stocks, or large ETFs improves matching efficiency and lowers the rate of slippage — especially important for short-term or high-frequency strategies.

Improve Your Technical Environment

A low-latency, highly stable platform and a fast network connection help reduce slippage caused by system delay and out-of-sync quotes.

Split Large Orders

Breaking a large order into several smaller orders entered in batches eases pressure on market price and lowers the risk of gaps and liquidity compression — suitable for traders with larger positions.

6. Frequently Asked Questions (FAQ)

Q1: Does a market order always cause slippage?

Not always, but the risk is higher. A market order has no price limit and is therefore exposed to quote movement; during high-volatility or low-liquidity windows, slippage becomes more likely.

Q2: Does slippage only happen on entry?

No — it can occur on exit (closing) as well. This is especially true with a stop-loss order: if the market gaps sharply, the stop is triggered at the next available execution price.

Q3: Why does a limit order sometimes fail to fill?

A limit order only fills when "the quote reaches your set price." If price never touches that level, the order will not execute — that is the trade-off for avoiding slippage.

Q4: Why are high-volatility assets more prone to slippage?

Because price moves quickly and queued orders are hard to process in sync, the actual execution price drifts away from the original quote.

Q5: What does a slippage-aware risk-management strategy look like?

Standard practice includes: ATR-based stop-loss sizing, conservative position sizing, concentrating trading in the deep-liquidity European/US sessions, aligning with the economic calendar, and logging your own average and maximum slippage.

7. Conclusion

Slippage is a pervasive price-deviation phenomenon in financial markets, reflecting the real gap between the quote and the fill. Its causes stem from changes in volatility, liquidity, and execution conditions, and it takes different forms across different markets.

Whether in forex, stocks, or cryptocurrency, slippage is part of the trading process and, alongside other trading costs, shapes the final return. Understanding its mechanics and the conditions behind it helps you grasp how the trading environment itself works.

The existence of slippage is a natural expression of price discovery and order matching in financial markets — a reminder that trading always carries a gap between certainty and timeliness.

Further Reading

Titan FX Research Team. We cover a broad set of financial instruments — foreign exchange, commodities (crude oil, precious metals, agricultural products), equity indices, US equities, and digital assets — producing practical, research-backed educational content for investors.

Primary Sources (by Category)

- Slippage fundamentals: Investopedia — Slippage, BabyPips — Order Types

- MT4/MT5 documentation: MetaQuotes — MT4 Help, MetaQuotes — MT5 Help

- Market liquidity research: BIS — Market Liquidity, CFTC — Flash Crash Report