OTC(Over-the-Counter)

Over-the-counter (OTC) trading is the buying and selling of assets directly between two parties without an exchange — the dominant model in forex and bond markets.

In financial markets, investors regularly encounter two distinct trading modes: exchange-traded and over-the-counter (OTC) markets. Exchange-traded transactions are matched through a centralized order book, with standardized contracts and transparent pricing. By contrast, OTC trading takes place directly between two counterparties — banks, brokers, market makers, and institutional or retail investors — who negotiate price and size on a bilateral basis.

As foreign exchange, bonds, and OTC derivatives markets have expanded, OTC has become an indispensable pillar of global capital flows. Currencies trade around the clock across a decentralized dealer network, corporate bonds change hands via request-for-quote pipelines, and bespoke derivatives are structured to meet specific hedging needs that no exchange-listed product can match.

This article unpacks the definition, mechanics, applications, advantages, and risks of OTC markets, and answers common questions, helping investors build a complete framework for using both exchange and OTC venues effectively.

- The structural difference between exchange-traded and OTC markets, and the economic rationale for each

- The participants, trading flow, and price-formation mechanics of OTC markets

- Forex, bonds, OTC derivatives, private equity, commodities, and crypto OTC desks: where OTC plays a central role

- The advantages (flexibility, breadth, block-trade efficiency) and inherent risks (information asymmetry, counterparty risk, liquidity risk)

- What individual investors should verify before participating in OTC markets

1. Exchange-Traded vs OTC: The Basic Distinction

Financial-market transactions broadly fall into two categories: exchange-traded and over-the-counter (OTC). Understanding the differences is the first step in mastering OTC markets.

Exchange-Traded Markets

Exchange-traded markets refer to transactions conducted on regulated venues such as the New York Stock Exchange (NYSE), Nasdaq, Tokyo Stock Exchange (JPX), London Stock Exchange (LSE), and major futures exchanges (CME, ICE). Contract specifications are standardized by the exchange, and an automated matching engine pairs incoming buy and sell orders.

- Instruments: listed equities, exchange-traded funds (ETFs), equity-index futures, commodity futures, and listed options

- Characteristics: real-time disclosure of prices and volumes, exchange-operated clearing house, settlement guarantees

Over-the-Counter (OTC) Markets

OTC trading bypasses centralized exchanges. Counterparties negotiate price, size, and other terms bilaterally — either one-on-one or through dealer-to-dealer networks such as electronic communication networks (ECNs) and request-for-quote (RFQ) platforms.

- Instruments: foreign exchange, corporate and government bonds, OTC derivatives, private equity, certain crypto assets

- Characteristics: terms can be customized to specific needs, price transparency is lower than on-exchange, counterparty credit risk must be managed individually

The Core Difference

Exchange-traded markets prioritize centralization, transparency, and standardization, whereas OTC markets emphasize decentralization, flexibility, and customization. Investors should pair the two depending on their objectives, position sizes, and required liquidity.

2. Mechanics and Market Architecture of OTC

Market Architecture

OTC markets are not anchored to a single exchange but instead consist of a distributed network of financial institutions and investors. Key participants include:

- Market makers and banks — continuously provide bid/offer quotes to supply liquidity

- Brokers and trading platforms — intermediate between investors and liquidity providers, managing risk and execution

- Institutional investors — funds, insurance companies, pension funds, and multinational corporations

- Retail investors — participate in forex margin trading and contracts for difference (CFDs) through brokers

Trading Flow

- The investor sends a request-for-quote (RFQ) to a broker or market maker, specifying price and size

- The quoting party returns bid (buy) and ask (sell) prices

- Both sides confirm price, size, settlement date, and other terms; if aligned, the trade is executed

- The transaction is then cleared and settled per the agreed terms

Defining Features

- Highly customizable: size, tenor, and reference asset can all be tailored to demand

- Non-standardized: the same product may carry different terms, spreads, and costs across counterparties

- Counterparty dependence: clearing and settlement guarantees are not as centralized as on-exchange, so the counterparty's credit and regulatory status must be assessed individually

The flexibility of OTC markets shifts more counterparty risk onto each participant. That is why selecting brokers and banks with strong regulation and balance sheets is the foundation of any OTC strategy.

3. Core Differences Between OTC and Exchange Trading

Exchanges exist to provide a unified rulebook and oversight framework. OTC markets, by contrast, function more like direct supply-and-demand matching — closer to a free-form bilateral economic model. The table below summarizes the key contrasts.

Comparison Table

| Dimension | Exchange-Traded | Over-the-Counter (OTC) |

|---|---|---|

| Contract spec | Standardized by the exchange | Non-standardized, bilaterally customized |

| Trading mode | Continuous auction, matched by the order book | Negotiated bilaterally between counterparties |

| Venue | Exchange floor or electronic trading platform | Decentralized network spanning banks, brokers, and platforms |

| Main instruments | Listed equities, ETFs, equity-index futures, commodity futures | Forex, bonds, OTC derivatives, private equity, certain crypto |

| Regulation | Strictly regulated, transparent rules | Regulatory depth varies by jurisdiction and product |

| Information transparency | Prices and volumes broadly disclosed | Disclosure is partial, information asymmetry possible |

| Liquidity | High due to order-book aggregation | Varies materially by product and currency pair |

| Trading costs | Fees are explicit but fixed components add up | Spread-based; cost structure depends on counterparty and platform |

Additional Notes

Product Design and Flexibility

Exchanges run on standardized contracts that allow many investors to participate under the same terms. OTC markets adapt to demand, accommodating special tenors, currencies, and notional sizes that exchanges cannot list.

Trading Mechanism and Transparency

Continuous auction trading on exchanges produces fair and transparent prices. OTC pricing comes from negotiation, so the same currency pair may be quoted differently by different dealers, making multi-broker price comparison essential.

Regulation and Counterparty Risk

On-exchange transactions are backstopped by clearing houses and regulators, materially reducing performance risk. Many OTC trades are not centrally cleared, so investors must independently assess each counterparty's capital adequacy and regulatory status.

Cost and Operational Overhead

Exchange trading benefits from standardized workflows but accumulates fixed costs (fees, exchange charges). OTC markets typically rely on spread-based pricing, and complex products bring additional risk-management overhead.

Takeaway

Exchanges deliver transparency and safety; OTC delivers flexibility and breadth. They are complementary, and sophisticated investors combine the two based on strategic intent.

4. Common Applications of OTC Markets

Most non-standardized financial products trade in OTC venues. The main domains are:

Foreign Exchange

Foreign exchange is the world's largest OTC market, with daily turnover measured in trillions of dollars. Central banks, commercial banks, hedge funds, corporates, and retail traders participate 24 hours a day across global time zones, with interbank quotes anchoring a tiered structure that brokers then distribute to retail clients.

- Participants: central banks, commercial banks, hedge funds, multinationals, retail investors

- Characteristics: continuous 24-hour trading, distributed price formation, regulatory regimes vary by jurisdiction

Bond Markets

Most corporate, municipal, and emerging-market sovereign bonds trade OTC rather than on-exchange. Bonds carry a wide range of maturities, coupons, and credit ratings that resist standardization. Investors typically obtain quotes individually from dealers and settle bilaterally.

OTC Derivatives

Forwards, swaps, OTC options, and credit default swaps (CDS) form a core part of corporate hedging and asset-liability management. Reference assets, tenors, and notional sizes can be tailored to specific risk exposures — capabilities that exchange-listed contracts rarely offer.

Private Equity and Pre-IPO Stock

Shares in private companies and pre-IPO ventures change hands through specialist platforms and investment banks. Disclosure standards are lower and volatility tends to be higher, so thorough due diligence is critical.

Commodity Forwards

Energy producers, airlines, and industrial users frequently rely on OTC forward contracts for crude oil, natural gas, and base metals to lock in delivery schedules and price exposure that fit their operational calendars.

Cryptocurrency OTC Desks

Institutional and high-net-worth crypto trades often route through OTC desks to avoid the price impact that comes with placing large orders into exchange order books. Liquidity providers quote bilaterally and settle outside the open market.

Across every domain, OTC's value proposition is customization and bilateral negotiation — meeting needs that exchanges cannot.

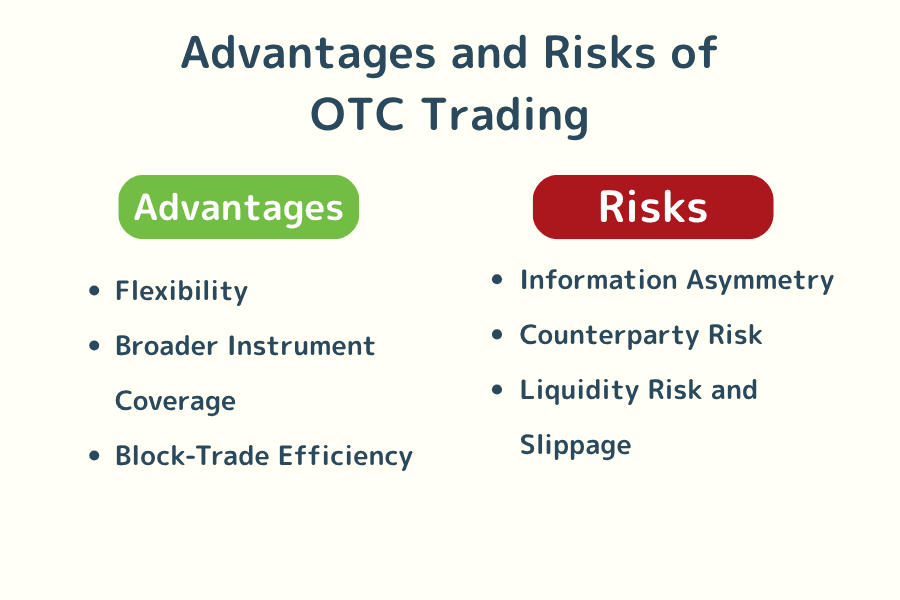

5. Advantages and Risks of OTC Trading

OTC accommodates diverse needs, but participants also inherit risks that on-exchange trading mitigates. Understanding both sides is a prerequisite for sound risk management.

Advantages

Advantage 1: Flexibility

Contract terms can be tailored to demand — size, tenor, underlying, and settlement method are all adjustable. Corporates and hedge funds can match risk exposures precisely.

Advantage 2: Broader Instrument Coverage

Beyond forex, OTC covers bonds, derivatives, private equity, commodity forwards, and crypto, giving access to instruments that exchanges cannot list.

Advantage 3: Block-Trade Efficiency

Placing very large orders on a centralized exchange can disrupt prices. OTC counterparties negotiate directly, allowing block trades to execute without sweeping the order book.

Risks

Risk 1: Information Asymmetry

Different dealers may quote different prices for the same instrument. Without multi-broker comparison, investors risk executing on the wrong side of an unfair spread.

Risk 2: Counterparty Risk

With no central clearing house standing in the middle, a counterparty default can leave unsettled positions exposed. This is precisely why the regulatory and capital standing of the counterparty matters.

Risk 3: Liquidity Risk and Slippage

For exotic products or during market stress, finding the other side of the trade can be difficult, and slippage can widen unexpectedly. Position sizing and exit planning should be defined in advance.

Capturing the upside of OTC markets requires quantifying these risks and choosing counterparties with regulatory standing, capital strength, and reliable liquidity provision.

6. Frequently Asked Questions (FAQ)

The questions below address common misconceptions about OTC markets.

Q1. Why is the foreign exchange market predominantly OTC?

Foreign exchange is a global, 24-hour market with participants across every time zone. A centralized exchange would struggle to deliver continuous liquidity to such a dispersed user base. A decentralized network of banks and brokers exchanging liquidity is more efficient — and that structure became the dominant FX model.

Q2. Does OTC mean "unsafe"?

No. OTC is a legal, regulated form of trading; its risk profile depends on the counterparty and the regulatory regime they operate under. Brokers regulated by recognized authorities (VFSC, ASIC, FCA, CFTC, etc.) must meet capital requirements, segregate client funds, and report trades. Trading with unlicensed counterparties materially raises credit and withdrawal risk.

Q3. Is OTC the same as a black market?

No. OTC refers to legal bilateral trading, most of which involves regulated financial institutions. Black markets are unlawful, unregulated, and offer no legal protection.

Q4. Why are some products only available on OTC?

Listing on an exchange requires standardized contract terms, sufficient liquidity, and a robust clearing infrastructure. Corporate bonds, OTC derivatives, and private-company shares — where each transaction has unique terms — do not fit into a centralized order book. OTC venues accommodate that non-standardized demand.

Q5. What should retail investors check before using OTC markets?

- Regulatory status: confirm the counterparty's regulator, registration status, and capital adequacy

- Client fund segregation: verify the existence of trust or segregated-account arrangements

- Pricing competitiveness: compare spreads and execution speed across multiple brokers

- Clearing and withdrawal flow: review deposit/withdrawal procedures, platform stability, and incident-response support

7. Summary

Over-the-counter trading is not a substitute for exchanges; it is a complementary backbone of the financial system. OTC markets have grown alongside global capital flows because demand for non-standardized, customized, and cross-border liquidity has continued to expand. Forex, bonds, derivatives, commodities, and crypto each rely on OTC mechanisms to deliver capabilities exchanges cannot replicate.

The greatest strength of OTC is flexibility. Its inherent challenges — information asymmetry, counterparty risk, and liquidity risk — must be managed with the right counterparties, diligent oversight, and well-defined risk processes.

Investors who understand both exchange and OTC venues, and who can choose between them based on strategic intent, are in the best position to navigate modern financial markets.

Further Reading

- Forex Margin Trading Basics

- Bid Price: Quote Mechanics and Practical Use

- Ask Price and the Spread Relationship

- CFTC (Commodity Futures Trading Commission) Overview

The financial markets research team at Titan FX. We produce educational content across a broad range of instruments, including forex (FX), commodities (crude oil, precious metals, agricultural products), equity indices, U.S. stocks, and crypto assets.

Primary Sources by Category

- OTC derivatives market overview: BIS — OTC derivatives statistics, BIS — Triennial Central Bank Survey of FX and OTC derivatives

- Regulatory and operational frameworks: IOSCO — OTC Markets Reports, ESMA — OTC Derivatives

- Market structure and statistics: SEC — Over-the-Counter Markets, FINRA — OTC Markets