Forex Execution Models: DD, NDD, STP, ECN, MM Differences

In the FX world you've likely heard terms like "ECN platform," "STP model," or "Market Maker." All these seemingly complex labels point to the same core concept — the execution model.

The execution model decides how your order is matched, who provides the price, and where the fill comes from. Different models directly affect spreads, execution speed, and pricing transparency — and together they shape the trading experience.

This article walks through the common models — DD, NDD, STP, ECN, MM — with diagrams and side-by-side comparisons. It also introduces Titan FX's STP / ECN account structure to help you decide which account type to start with for the trading environment that fits you.

- The execution model decides how orders are matched, who provides the price, and where fills come from — directly driving spreads, speed, and transparency.

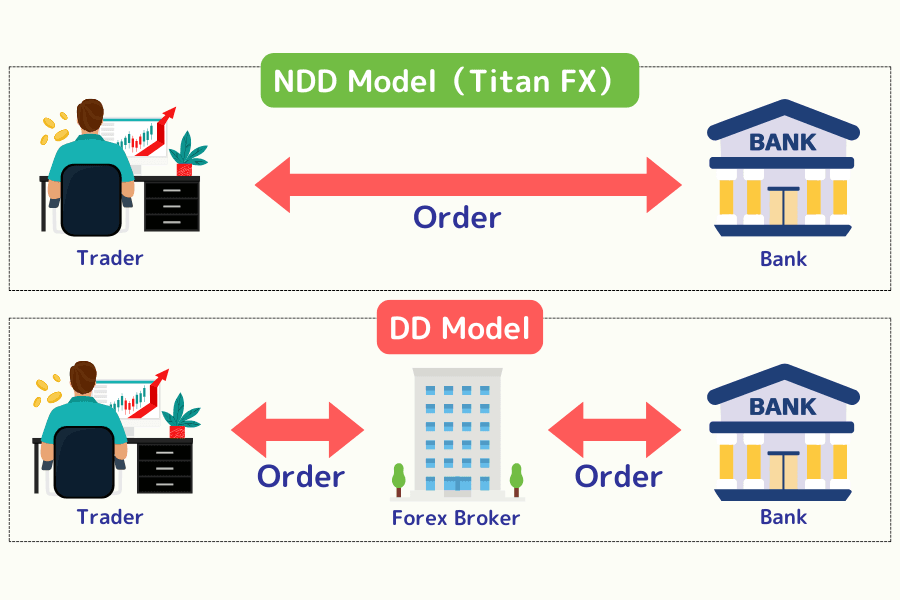

- Two main types: DD (Dealing Desk, Market Maker) handles orders internally and may take the other side; NDD (No Dealing Desk) routes to external liquidity providers.

- NDD splits into STP (direct routing, suits everyday traders and EAs) and ECN (deep liquidity network, suits high-frequency, scalping, professional strategies).

- Pricing differences: DD usually fixed spreads; NDD STP variable spreads with markup; ECN ultra-low variable spreads + fixed commission.

- Titan FX uses an STP / ECN no-dealer-intervention model: Standard (STP, up to 500x), Blade (ECN, $3.5/lot per side), and Micro (STP, up to 1000x).

- 1. What Is a Forex Execution Model?

- 2. DD (Dealing Desk) and the MM (Market Maker) Mechanism

- 3. NDD (No Dealing Desk): The Modern Standard

- 4. STP (Straight Through Processing)

- 5. ECN (Electronic Communication Network)

- 6. Side-by-Side Comparison of All Models

- 7. How to Choose the Right Execution Model

- 8. Titan FX Models and Account Comparison

- 9. Conclusion: From Understanding to Choosing

1. What Is a Forex Execution Model?

In the FX market, the execution model is one of the core factors shaping your trading experience and cost structure. It influences how your order is executed, who matches it, and where the final price comes from.

For beginners, understanding the differences between models is the most effective way to avoid landing in a high-cost, slippage-prone, or non-transparent trading environment.

Why You Should Care About Execution Models

Forex is a decentralised (OTC) market with no single source of truth for quotes. Each broker builds its own execution model from its quote sources, matching mechanics, and risk framework — and that directly shapes:

- ▸ The realism and transparency of quotes

- ▸ Execution speed and slippage risk

- ▸ Whether the broker is on the other side of your trade

- ▸ Total commission and spread cost

Knowing the execution model is like knowing how a car's engine works: cars look similar from the outside, but the internals decide speed, stability, and safety.

The Two Main Buckets

The single most important question is: does the market match your order, or does the broker take the other side?

Based on that core distinction, FX execution models fall into two broad categories:

| Type | Name | How It Works |

|---|---|---|

| DD (Dealing Desk) | Market-maker model | The broker matches orders internally and may become your counterparty. |

| NDD (No Dealing Desk) | Direct-to-market model | Orders flow straight to external liquidity providers; pricing is closer to the real market. |

2. DD (Dealing Desk) and the MM (Market Maker) Mechanism

Two ideas to nail down up front:

- DD (Dealing Desk) is the "with-dealing-desk" model, and MM (Market Maker) is the role that performs the matching inside that model.

DD decides who handles the order; MM decides who matches you and what price they show.

DD — Internal Matching by the Platform

In a DD model, the broker handles and matches orders internally rather than always sending them to the external market. That allows the platform to offer stable quotes and fixed spreads — but it also means the platform may be your counterparty.

Simplified Workflow

- ▸ Step 1 — Order: order enters the platform's internal system.

- ▸ Step 2 — Quote and Match: the platform provides bid/ask quotes from internal or external sources.

- ▸ Step 3 — Internal Fill: with no external liquidity, the platform may fill the trade itself.

Characteristics of the DD Model

- ▸ Quotes come from the platform, not real-time global market quotes

- ▸ Spreads are typically fixed, costs are predictable

- ▸ Execution is usually fast with few requotes or noticeable slippage

DD appeals to beginners, conservative traders, and users who prefer fixed spreads, but is less suitable for traders who want maximum transparency or true market quotes.

DD Pros and Cons

| Pros | Cons |

|---|---|

| Fixed spreads, controlled costs | Platform may be the counterparty |

| Stable quotes, smooth execution | Quotes may differ slightly from the market |

| Simple to use, friendly to beginners | Less ideal for high-frequency or automated strategies |

When choosing a DD platform, focus on regulatory compliance, transparency, and brand reputation.

MM — How Market Makers Implement the DD Model

The MM (Market Maker) is the most common implementation of DD. When the market lacks a natural counterparty, market makers "create the market" by quoting a continuous bid/ask, ensuring traders can always get filled.

Market-Maker Logic

- ▸ Continuous quoting: the market maker shows both Bid and Ask at the same time.

- ▸ Filling orders: when you submit an order, the market maker can become your direct counterparty.

- ▸ Profit source: primarily from the bid/ask spread.

Functions and Behaviour

| Function | Description |

|---|---|

| Provide liquidity | Even when markets are thin, you can still get filled. |

| Maintain price continuity | Avoid price gaps and missing quotes. |

| Take on market risk | When prices move sharply, the market maker absorbs the loss. |

The core strengths of MM are stability, predictability, and fixed spreads — very friendly to beginners. The downside is lower transparency and potentially misaligned interests with the trader.

3. NDD (No Dealing Desk): The Modern Standard

As FX markets have gone electronic and transparency expectations have risen, more traders want real market quotes and a fair matching environment.

That demand has pushed NDD (No Dealing Desk) to the forefront of modern FX trading.

Unlike traditional DD, an NDD platform doesn't run a dealing desk, doesn't quote the market, and doesn't take the other side of your trade.

Every order is automatically routed to external liquidity providers (LPs) — banks and large financial institutions. The platform serves as a "bridge," ensuring traders get the best price available in the market.

NDD's spirit can be captured in three keywords: transparent, market-driven, automated.

The point isn't to simulate the market — it's to put traders directly in touch with real market prices.

Trait 1: Automated Matching, Fast and Stable Execution

Under NDD, every order flows to a liquidity pool. An algorithm compares quotes from multiple LPs in real time and matches at the best available bid/ask.

This fully automated flow has clear benefits:

- ▸ No human intervention

- ▸ Almost no requotes

- ▸ Lower latency, with quotes and fills more in sync

For traders who care about speed and stability — intraday traders or EA users — that's a critical experience difference.

Trait 2: No Counterparty Risk, More Transparent Pricing

NDD platforms don't bet against you, don't manipulate quotes, and don't decide the fill price.

Quotes come entirely from external LPs, so:

- ▸ Fill prices reflect real supply and demand

- ▸ Conflicts of interest are reduced

- ▸ Trading is more fair and trustworthy

The biggest difference vs DD: the platform doesn't take on market risk, and doesn't profit from your losses.

Trait 3: Variable Spreads and Flexible Cost

Because NDD pricing tracks the market, NDD uses floating (variable) spreads.

The behaviour:

- ▸ When the market is active (e.g., London/NY overlap) → spreads are usually very low

- ▸ During low liquidity or high volatility → spreads can widen

NDD platforms typically charge in two ways:

- ▸ A small markup over raw market spreads (Spread Markup)

- ▸ Or a fixed per-lot commission (Commission)

This makes the cost structure more transparent and lets traders match account types to their strategies.

Two Main NDD Implementations

NDD isn't a single thing — it covers two clearly distinct structures:

STP (Straight Through Processing)

- Orders go straight through to liquidity providers

- The platform may add a small markup inside the spread

- Real market pricing + stable execution → suits everyday traders and automated strategies

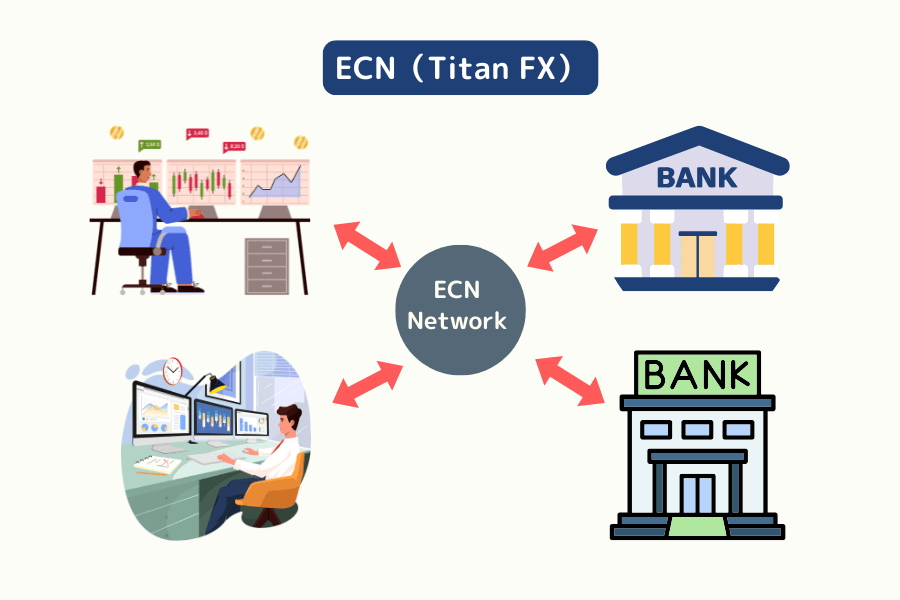

ECN (Electronic Communication Network)

- Orders match within a shared network

- Market depth (Level II) is visible

- Pricing is closest to the interbank market → favoured by high-frequency, scalping, and professional traders

If NDD is the umbrella concept of "no dealer intervention," STP and ECN are the two most common concrete realisations of it. The next sections unpack each in more detail to help you choose the environment that best fits your strategy.

4. STP (Straight Through Processing)

Within the NDD architecture, STP (Straight Through Processing) is the most widely used and accessible execution method for the majority of retail traders.

The core idea of STP: route every order directly to external liquidity providers (LPs) rather than match it internally.

This avoids the quote-intervention and counterparty issues of traditional DD, providing a more transparent, more efficient, and more market-driven trading environment.

Core STP Characteristics

| Trait | Description |

|---|---|

| Automated execution, low latency | Orders flow fully automatically to the external liquidity pool, reducing requotes and latency, supporting intraday and EA strategies. |

| Variable spreads, flexible cost | Quotes come from multiple LPs, spreads move with the market, the platform may add small markup. |

| No counterparty risk | The broker doesn't take the other side; it acts as a "router," reducing conflict of interest. |

| Close to real market prices | Prices reflect competitive quotes from multiple LPs, with high transparency and stable execution quality. |

With STP, traders get both real market liquidity and a stable execution environment — the most common and easiest-to-understand modern model in retail FX.

5. ECN (Electronic Communication Network)

Within the NDD architecture, ECN (Electronic Communication Network) is the most transparent execution model and the closest to professional markets.

ECN connects traders, banks, financial institutions, and other participants into a single shared liquidity network where every order is automatically matched — without relying on broker quotes.

So in an ECN environment: the platform is purely a matching engine, and traders connect directly with each other.

Core ECN Characteristics

| Trait | Description |

|---|---|

| Fully market-driven pricing | Quotes come from banks, financial institutions, and other market participants, with no markup — closest to the real market. |

| Ultra-low spreads + fixed commission | A "ultra-low spread + commission" model with transparent costs, suited to active traders and high-frequency strategies. |

| Market depth (Level II) visible | Shows resting orders at every price level, helping evaluate liquidity, support/resistance, and sentiment. |

| High-frequency matching, very low latency | Direct access to liquidity, fast matching and very low latency — ideal for scalping and automated trading. |

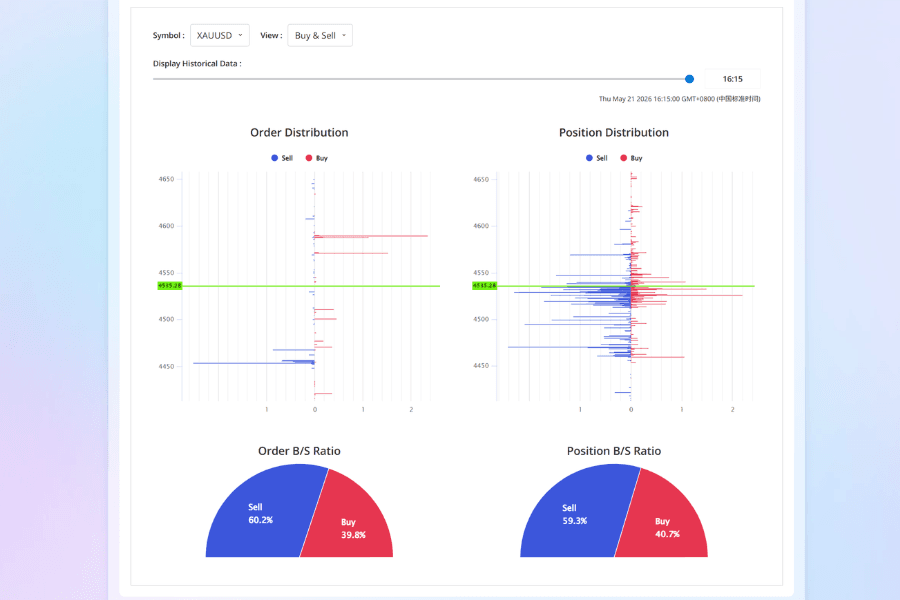

Example: Titan FX Market Depth and Order Book

In addition to ECN execution, Titan FX provides an "order book / open-interest trend chart" that visualises anonymised order data from clients across the Titan FX group, helping read market sentiment.

Order book and open-interest trend

6. Side-by-Side Comparison of All Models

The table below pulls together the main FX execution models — DD (market maker), NDD (no dealing desk) and its two variants STP and ECN.

The differences in pricing transparency, execution mechanics, and cost structure are clear; understanding them helps pick the right environment.

| Category | Sub-model | Dealing desk | Counterparty | Quote source | Spread type | Cost structure | Transparency | Best for |

|---|---|---|---|---|---|---|---|---|

| DD (Market maker) | — | Yes | Yes | Platform internal | Fixed | No commission | Lower | Beginners, conservative traders |

| NDD (No dealing desk) | STP (Straight Through Processing) | No | No | Multiple LPs | Variable | Markup spread | High | Mid-tier, automated traders |

| NDD (No dealing desk) | ECN (Electronic Communication Network) | No | No | Global liquidity pool | Ultra-low variable | Fixed commission | Very high | High-frequency, professional traders |

7. How to Choose the Right Execution Model

Choosing an FX execution model comes down to your trading style and strategy needs. The simplest decision tree:

- ▸ Want transparent, market-driven quotes → choose NDD (STP / ECN)

- ▸ Want stability and predictable cost → choose DD (Market maker)

Within NDD:

- ▸ Everyday trader, EA user, or intraday strategy → STP

- ▸ Need ultra-low spreads, fastest execution, professional strategy → ECN

If you're a beginner, start on a MT5 demo account or a Micro account, then graduate to STP or ECN once you're comfortable.

8. Titan FX Models and Account Comparison

Titan FX uses a highly transparent STP / ECN no-dealer-intervention (NDD) structure, providing instant fills, low latency, and real market quotes.

The table below compares the core differences across Titan FX account types:

| Account | Standard | Blade | Micro |

|---|---|---|---|

| Execution model | STP | ECN | STP |

| Maximum leverage | 500x | 500x | 1,000x |

| Spread | Low | Ultra-low | Low |

| Commission | None | $3.5 per side per lot (USD equivalent) | None |

| Minimum order size | 0.01 lot | 0.01 lot | 0.01 micro lot |

| Best for | Beginners, intermediate traders | Professional and high-frequency traders | EA testing, automated trading users |

Titan FX also supports a rich, free EA (Expert Advisor) suite for MT4 / MT5, with forward and back-test results visible before use.

9. Conclusion: From Understanding to Choosing

The FX market offers many execution models, but the underlying question is always the same: how is your order matched, and who provides the price?

From traditional DD / MM to modern STP / ECN, each model has its place:

- DD provides stability and predictable cost

- NDD prioritises transparency and real prices

- STP and ECN push efficiency and execution closer to professional markets

For traders, understanding the execution model is like understanding the engine of the market. Only when you know whether your order goes "directly to the market" or "through the platform internally" can you really evaluate cost, speed, and risk.

If you value fairness, transparency, and low latency, a no-dealer-intervention NDD (STP / ECN) platform is the more durable long-term direction.

That's exactly the architecture Titan FX is built on — deep liquidity, fast execution, and instant fills providing a professional-grade environment for traders who want better execution quality.

Further Reading

The Titan FX financial market research team. Covering FX, commodities (oil, precious metals, agricultural products), stock indices, US equities, and crypto assets, the team produces educational content for investors across a wide range of financial instruments.

Primary Sources (by category)

- Official references: Titan FX Standard / Blade / Micro account specifications; Titan FX regulatory licences and compliance disclosures; MT4 / MT5 platform manuals

- Industry standards: Broker classification and disclosure standards from NFA, FCA, ASIC, and other regulators; ISDA OTC derivatives standards

- Market data: BIS Triennial Central Bank Survey (FX market size); Bloomberg and Reuters liquidity-provider data

- Industry and third-party references: Investopedia (DD / NDD / STP / ECN entries); Forex Peace Army and Myfxbook broker reviews; Titan FX internal execution-quality and risk-management documentation