Shareholder's Equity

When reading financial statements or using stock-screening tools, investors often search for "what is shareholder's equity," "how to calculate shareholder's equity," "how to read book value per share," or "price-to-book (P/B) ratio." Shareholder's Equity is one of the core data points on the balance sheet, representing the real residual value attributable to shareholders after all debts are paid off.

This guide starts from the basic concept, breaks down the shareholder's equity formula along with the meaning of paid-in capital, capital surplus, and retained earnings, and shows how to use the statement of changes in equity, book value per share, and ROE to judge a company's fundamental health — so you can identify financially solid, potentially undervalued names in your portfolio.

- 1. What Is Shareholder's Equity? Core Concept

- 2. Shareholder's Equity Formula and Book Value Per Share

- 3. Components: Paid-in Capital, Capital Surplus, and Retained Earnings

- 4. What Moves Shareholder's Equity? Reading the Statement of Changes

- 5. Practical Use in Investment Decisions

- 6. Judging Equity via ROE and P/B

- 7. FAQ: Real-World Questions About Equity and Book Value

- 8. Summary: Building a Proper View of Corporate Value

1. What Is Shareholder's Equity? Core Concept

Shareholder's Equity is the portion of a company's assets that truly belongs to shareholders after every liability is paid off — also known as "net assets" or "book value of equity." Put simply, it answers one question: "If we sold every asset the company owns right now and cleared every debt, how much would be left for the shareholders?"

If we compare a company to a house, the market value of the house (total assets) minus the mortgage (total liabilities) is what the owner actually owns — that is shareholder's equity. A higher figure generally indicates a more solid financial foundation and more value accruing to shareholders. On the balance sheet, shareholder's equity sits after liabilities and, together with liabilities, forms the sources of capital for the company.

2. Shareholder's Equity Formula and Book Value Per Share

Understanding how shareholder's equity is calculated helps you quickly size up a company's financial posture.

Core formula:

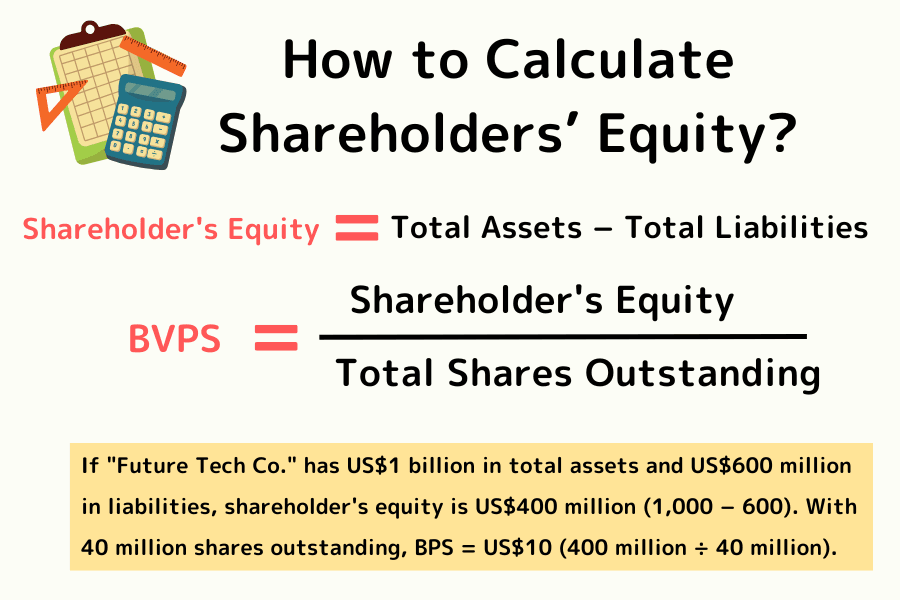

Shareholder's Equity = Total Assets − Total Liabilities

This is also the foundational balance-sheet identity (Assets = Liabilities + Equity).

The figure appears directly at the bottom of the balance sheet. In stock selection, investors more often use Book Value Per Share (BPS), which tells you how much real value sits behind each share.

Book Value Per Share formula:

Book Value Per Share = Shareholder's Equity ÷ Total Shares Outstanding

Worked Example

If "Future Tech Co." has US$1 billion in total assets and US$600 million in liabilities, shareholder's equity is US$400 million (1,000 − 600). With 40 million shares outstanding, BPS = US$10 (400 million ÷ 40 million).

3. Components: Paid-in Capital, Capital Surplus, and Retained Earnings

Shareholder's equity is mainly composed of three items:

| Component | Meaning | Main Source | What to Watch |

|---|---|---|---|

| Paid-in Capital | The original capital received when shares were issued | Shareholder contributions | Company's legal capital base |

| Capital Surplus | Premium-issuance and other non-operating capital gains | Premium issuance, asset revaluation | Lower quality than retained earnings |

| Retained Earnings | Cumulative profits retained after dividends over the years | Core business profits | Best reflects a company's real earning power |

Retained earnings are the most valuable of the three, because they represent money the company genuinely earned from its core business. Capital surplus also grows equity but usually comes from one-off capital transactions, so its quality is typically lower.

4. What Moves Shareholder's Equity? Reading the Statement of Changes

Shareholder's equity is not static — it moves with operating activities and dividend policy. The statement of changes in equity lays out exactly how corporate value moved up or down.

Driver 1: Operating Profit or Loss

The company's net income adds to retained earnings and therefore lifts equity. A loss shrinks equity.

Driver 2: Cash Dividends

When the company pays cash dividends to shareholders, cash flows out of assets and retained earnings drop on the equity side. That is why a stock's price drops by the dividend amount on the ex-dividend date — because the company's book value has literally decreased.

Driver 3: Equity Issuance or Reduction

Asking shareholders for more capital (equity issuance) increases equity. Buying back shares (treasury stock) or a cash capital reduction lowers equity.

5. Practical Use in Investment Decisions

Tracking shareholder's equity movements helps distinguish companies that are genuinely growing from those propping up the facade through financial maneuvers.

Strategy 1: Watch Retained Earnings Growth

Quality companies should consistently generate profits and turn them into retained earnings. If equity is rising because retained earnings are compounding, the core business is usually doing well.

Strategy 2: Beware of Capital-Surplus-Driven Growth

If a company's core business has been losing money, yet equity is propped up by repeated equity issuances, it's burning through shareholder capital to stay alive rather than making money through operations. Long-term investment value deserves close scrutiny.

Strategy 3: Assess Financial-Structure Safety

The higher the ratio of shareholder's equity to total assets (i.e., the lower the debt ratio), the stronger the company's financial defenses. Such businesses have higher survival rates through recessions and rate-hiking cycles.

6. Judging Equity via ROE and P/B

Looking at the absolute size of shareholder's equity or BPS alone is not enough. "Book value" reflects past accumulation, while "share price" reflects market expectations about the future. To properly judge whether a company is investable, cross-reference earning power (ROE) with market valuation (P/B).

Core Metrics

-

Price-to-Book Ratio (P/B Ratio): Judges whether a share price is expensive or cheap. Formula: Share Price ÷ Book Value Per Share. Generally, P/B < 1 means the share price is below book value — potentially undervalued.

-

Return on Equity (ROE): Measures how efficiently the company uses shareholder's equity to generate earnings. ROE = Net Income ÷ Shareholder's Equity. A high book value means little if the company cannot put it to work.

Practical: The ROE × P/B Stock-Selection Matrix

Combining these two metrics lets you quickly classify stocks and identify the genuinely high-value names:

| Combination | Evaluation | Practical Guidance |

|---|---|---|

| High ROE + Low P/B | Undervalued | The most desirable profile. Strong earning power, but the share price hasn't caught up. Worth deep research. |

| High ROE + High P/B | Quality Growth | The market has already awarded a premium. Suits long-term holders, but watch entry points and growth durability. |

| Low ROE + Low P/B | Value Trap | Cheap on the surface but weak operationally — stock can stay depressed for years. Handle with care. |

| Low ROE + High P/B | Significantly Overvalued | Highest risk. Weak earning power with an inflated valuation. Best avoided. |

Reading Tips

- (1) Book value is the floor, ROE is the ceiling: Equity provides the lower bound of value; ROE sets the upper bound of growth.

- (2) Beware "one-off" high ROE: A sudden ROE spike from asset disposals (rather than retained-earnings growth from operations) typically doesn't persist.

- (3) Quality companies usually combine stable equity growth + high ROE + reasonable P/B.

Apply this cross-analysis framework and you can quickly identify companies with genuinely solid fundamentals when screening or reading financial statements.

7. FAQ: Real-World Questions About Equity and Book Value

Q1: Does high shareholder's equity (book value) always mean the stock price will rise?

Not necessarily. Book value is an accounting record of the past, while share price reflects the market's future expectations. A company with ample book value but lacking growth momentum can trade near or even below its book value for a long time.

Q2: Why do some quality stocks trade at very high P/B?

For software or brand-driven companies, the bulk of value comes from intangible patents or brand, which may not be fully reflected in book value. The market is willing to pay several times book value because it expects strong future profitability.

Q3: What happens if book value turns negative?

When total liabilities exceed total assets, shareholder's equity turns negative - known as "negative equity" or "book insolvency." These companies often face delisting risk, because the company's liabilities outstrip its assets; risk is extremely high.

Q4: Is higher book value per share always better?

A higher BPS means more net assets per share, but you still need to read it alongside ROE and earning power. If the company cannot effectively put those assets to work, a high BPS means little.

Q5: Does a high ratio of retained earnings automatically mean a great company?

Not necessarily. A high retained-earnings share usually signals strong earning power, but watch whether the funds are deployed effectively (check ROE). If a company parks large retained earnings in low-yield bank deposits or poor-return investments, it's not the best choice for shareholders either.

8. Summary: Building a Proper View of Corporate Value

Shareholder's equity is a core indicator of a company's financial foundation, calculated as Total Assets minus Total Liabilities. The three main components are paid-in capital, capital surplus, and retained earnings — with retained earnings best reflecting real earning power.

Beginner Investment Checklist:

- Is shareholder's equity growing steadily?

- Is the growth driven mainly by retained earnings, or by capital surplus and equity issuance?

- Are you cross-referencing with ROE and P/B for a comprehensive judgment?

- Are you avoiding companies with negative book value or over-reliance on equity raises?

With a firm grasp of shareholder's equity, you can more accurately evaluate corporate value — in both Japanese and US equities — and make steadier long-term investment decisions.

Titan FX Trading Strategy Research Institute

The financial markets research team at Titan FX. Produces educational content for investors across a broad range of asset classes, including foreign exchange (FX), commodities (crude oil, precious metals, agricultural products), stock indices, US equities, and cryptocurrencies.

Primary sources: SEC EDGAR, NYSE Listed Companies, IFRS, U.S. GAAP (FASB), Bloomberg, Reuters