What Is a Cash Flow Statement? Three Components & Free Cash Flow Explained

In financial analysis, there is a well-known saying: "Earnings are an opinion, but cash is a fact." Plenty of companies report substantial profits on their income statements yet fail because they cannot produce enough actual cash to cover payroll or supplier bills. This phenomenon is known as "profitable but insolvent" — a painful lesson that cash is the ultimate arbiter.

The Cash Flow Statement exists precisely to strip out the accounting illusions and show investors the real money moving in and out of a company's pockets. It is the most honest yardstick for measuring the quality of a company's operations.

- 1. What Is a Cash Flow Statement?

- 2. The Three Components of a Cash Flow Statement

- 3. Free Cash Flow: The Core Measure of a Company's "Real Earning Power"

- 4. Cross-Analysis: Cash Flow vs. Income Statement & Balance Sheet

- 5. Reading Logic for Beginners: What the Sign Combinations Tell You

- 6. FAQ: Common Misconceptions in Cash Flow Analysis

- 7. Summary: The Investment Core of the Cash Flow Statement

1. What Is a Cash Flow Statement?

A Cash Flow Statement is a financial report that tracks the flow of cash into and out of a company over a specific period. Alongside the balance sheet and the income statement, it forms one of the three core financial statements.

Unlike the income statement, which follows the accrual basis (transactions are recorded when they occur), the cash flow statement uses the cash basis: only transactions in which cash actually changes hands are recorded.

For example, if a company sells US$1 million of goods but the buyer has not yet paid, the income statement still recognizes the revenue. The cash flow statement, however, does not — because the cash has not physically arrived.

Because of this difference, the cash flow statement becomes an indispensable tool for assessing a firm's real financial condition. Investors can see whether the company has stable cash sources, whether it is over-reliant on borrowing, and where its cash is actually going.

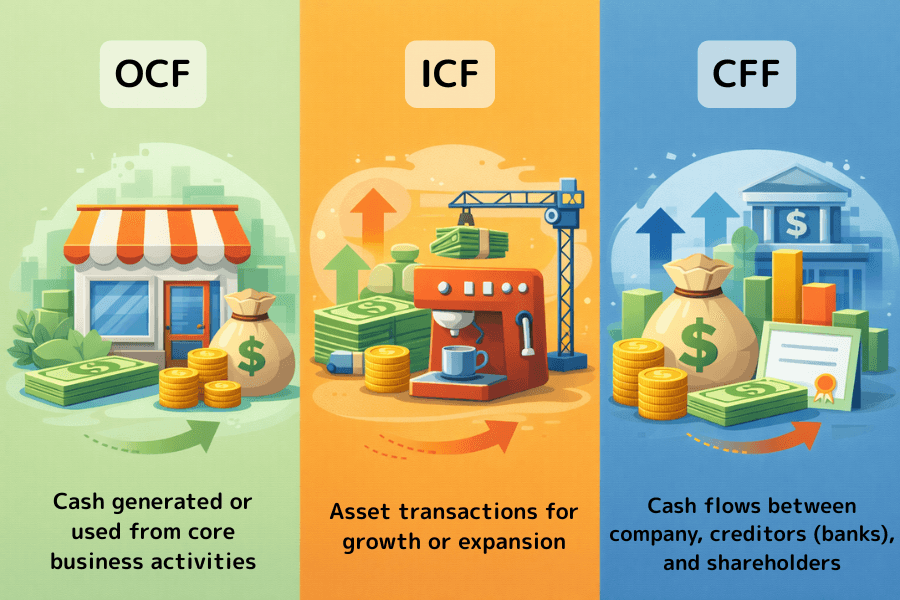

2. The Three Components of a Cash Flow Statement

The cash flow statement organizes every cash movement into three broad categories. Using Mr. Tanaka's coffee shop scenario, we can unpack what each category means and what the sign of the number signals.

Component 1: Operating Cash Flow (OCF)

This is the cash generated or consumed by the company's core business activities. It shows whether, without borrowing or selling assets, the company can sustain itself through its own operations.

- Positive: Means the coffee shop's cash from selling coffee is enough to cover beans, wages, and rent — the business is self-sustaining.

- Negative: The core business is running at a deficit. Either sales are not translating into collections, or costs are too high — the shortfall must be covered by savings or outside funding.

Component 2: Investing Cash Flow (ICF)

This records asset purchases and sales the company undertakes to maintain its competitive edge or expand for the future.

- Positive: The company is "monetizing" assets — for example, selling an old espresso machine or disposing of a property, bringing cash back into the business.

- Negative: The company is "investing" — for example, Tanaka buys a roasting machine to develop new blends or opens a second location in a prime area. Often a sign of ambition and growth intent.

Component 3: Cash Flow from Financing (CFF)

This reflects cash flows between the company and its creditors (banks) and shareholders.

- Positive: The company is "raising money" — Tanaka takes out another US$20,000 bank loan or brings in new investors, and cash flows in.

- Negative: The company is "returning money" — repaying a portion of the bank loan's interest, or paying dividends to shareholders.

3. Free Cash Flow: The Core Measure of a Company's "Real Earning Power"

Free Cash Flow (FCF) is one of the most closely watched metrics among professional investors. The formula is refreshingly direct:

Free Cash Flow = Operating Cash Flow − Capital Expenditure (CapEx)

"Capital expenditure" here refers to the hard investment required just to maintain the current scale and competitiveness of the business (for instance, replacing a broken coffee machine).

Investment Meaning: What a Company Can Truly Spend at Its Own Discretion

Free cash flow represents the surplus a company has after operating its business, paying all required costs, and refreshing its equipment — the cash that management can freely deploy. The uses are wide-ranging: building a reserve against downturns, funding a new product line, paying down long-term debt, or — most welcome to investors — returning capital via dividends or share buybacks.

4. Cross-Analysis: Cash Flow vs. Income Statement & Balance Sheet

Financial statements are not isolated numbers; they are gears that turn each other.

| Dimension | Income Statement | Balance Sheet | Cash Flow Statement |

|---|---|---|---|

| Main focus | Whether the company made a profit | Financial position at a point in time | Actual cash flows in and out |

| Functional role | Report card for earning power | Health check of corporate strength | Monitor of cash safety |

| Key perspective | Book profit or loss (including depreciation and receivables) | Asset, liability, and equity structure | Real sources and uses of cash |

| Core question | How much was "earned" during the period | How much the company "has" at this moment | How much came "in and out" during the period |

| Data basis | Accrual basis (record when transaction occurs) | Stock concept (balances of assets and debts) | Cash basis (record only when cash moves) |

Cash Flow vs. Income Statement (Quality of Earnings)

Net income can be adjusted through accounting choices, but cash flow is far harder to manipulate. If Tanaka's coffee shop has grown net income rapidly for three straight years yet operating cash flow is negative, it usually means money is stuck in receivables or piled up in inventory — a classic sign of low-quality earnings with genuine bankruptcy risk.

Cash Flow vs. Balance Sheet (Asset Liquidity)

The cash flow statement explains how the "cash" line on the balance sheet moved from the beginning of the period to the end. When financing inflows appear, cash and debt on the balance sheet rise together — allowing investors to see whether the increase in assets was earned or simply borrowed.

Three-Statement Linkage (Practical Example)

Say Tanaka spends US$50,000 on a top-end coffee machine. Here is how the movement ripples through all three statements.

- Balance sheet: Fixed assets (property, plant & equipment) rises by US$50,000.

- Cash flow statement: Investing cash flow (ICF) records a US$50,000 outflow.

- Income statement: The US$50,000 is not expensed in one shot; instead, it flows through the P&L as monthly depreciation over an assumed 5-year useful life.

5. Reading Logic for Beginners: What the Sign Combinations Tell You

By lining up the signs of Operating (O), Investing (I), and Financing (F) cash flows, the company's survival state becomes vivid.

| O | I | F | Profile | Interpretation |

|---|---|---|---|---|

| + | − | − | Stable Operator | Core business generates steady cash, funds investment needs, and still has room to reduce debt or return capital. Financial structure is healthy. |

| + | − | + | Growth Expansion | Core business is already cash-generating, but the company is also tapping outside capital to scale up. Typical of active expansion phases. |

| + | + | − | Asset Restructuring | Core business remains positive, while asset sales generate additional cash used to pay down debt or optimize capital structure. |

| − | − | + | Growth Investment | Core business has not yet turned cash-positive, yet capital spending continues. Heavily reliant on external funding. |

| − | + | + | Under Cash Pressure | Operating cash flow is negative; the company leans on asset disposals and outside financing to keep things running. Watch sustainability closely. |

6. FAQ: Common Misconceptions in Cash Flow Analysis

Q1: Is negative or positive Investing Cash Flow (ICF) a good thing?

For companies in a growth phase, a negative investing cash flow is usually healthy — evidence that the firm is investing in future capacity. Conversely, if a manufacturer's ICF has been positive for years, the company is likely selling off assets to keep the lights on, often a sign that competitiveness is fading.

Q2: Why do some companies report high net income but low operating cash flow?

Two main reasons: first, accounts receivable are too high — the goods sold but the money has not been collected. Second, inventory is piling up, with capital tied up in unsold stock in the warehouse. Both reflect weak bargaining power with customers or channels.

Q3: Can Free Cash Flow (FCF) be negative?

Short-term negative FCF is acceptable — especially in years when a company undertakes large-scale capacity additions (for example, a semiconductor manufacturer building a new fab). However, persistent long-term negative FCF means the company is generating less cash than it needs and must continually raise capital or borrow to survive — a business model that is fundamentally unstable.

7. Summary: The Investment Core of the Cash Flow Statement

The cash flow statement is the last line of defense for financial transparency. It tells investors whether profits are backed by real cash or are merely paper gains, whether the pace of expansion is overreaching, and whether there is enough slack to return capital to shareholders. When analyzing a company, beginners should prioritize those with positive operating cash flow and stable free cash flow. Once you can read the flow of cash to understand the real operating truth of a business, you will avoid countless investment traps that look shiny but are hollow inside.

Titan FX Trading Strategy Research Institute

The financial markets research team at Titan FX. Produces educational content for investors across a broad range of asset classes, including foreign exchange (FX), commodities (crude oil, precious metals, agricultural products), stock indices, US equities, and cryptocurrencies.

Primary sources: SEC EDGAR, IFRS, U.S. GAAP (FASB), FASB Statement No. 95 — Statement of Cash Flows, Bloomberg, Reuters