Merrill Lynch Investment Clock

"Should I buy stocks now, or bonds, or wait in cash?" As the phase of the economy changes, the assets that do best rotate too. The Merrill Lynch Investment Clock organizes that rotation into four phases of the business cycle to help guide asset-allocation decisions.

This model, introduced by Merrill Lynch, holds that by observing the strength of economic growth and the level of inflation, the market can be divided into four phases—recovery, overheat, recession, and stagflation—each with its own favored asset. Many investors use it to understand the macro environment and adjust their allocation accordingly.

This article covers the basic definition and mechanics of the Merrill Lynch Investment Clock, the features and allocation ideas for the four phases, how to apply it in practice, and its limitations and beginner cautions—helping investors build a more systematic view of the economic cycle.

- Grasp the definition and the two core indicators.

- Learn the four phases and where each asset leads.

- See how the clock is applied in modern markets.

- Understand its limits and common beginner mistakes.

- Build macro-cycle thinking into rational allocation.

1. What Is the Merrill Lynch Investment Clock? Cycle and Rotation

The Merrill Lynch Investment Clock is a macro investing framework for analyzing the relationship between the economic cycle and asset performance, introduced by Merrill Lynch.

The model holds that economic activity does not move in only one direction; it varies cyclically with the strength of growth and the level of inflation. By observing these two core indicators, investors can judge which phase of the cycle they are in and adjust their allocation accordingly.

The Merrill Lynch Investment Clock rests on two key variables:

- Economic growth: measured by GDP growth or the output gap, reflecting corporate profits and employment.

- Inflation: tracked mainly through the Consumer Price Index (CPI), reflecting prices and the direction of monetary policy.

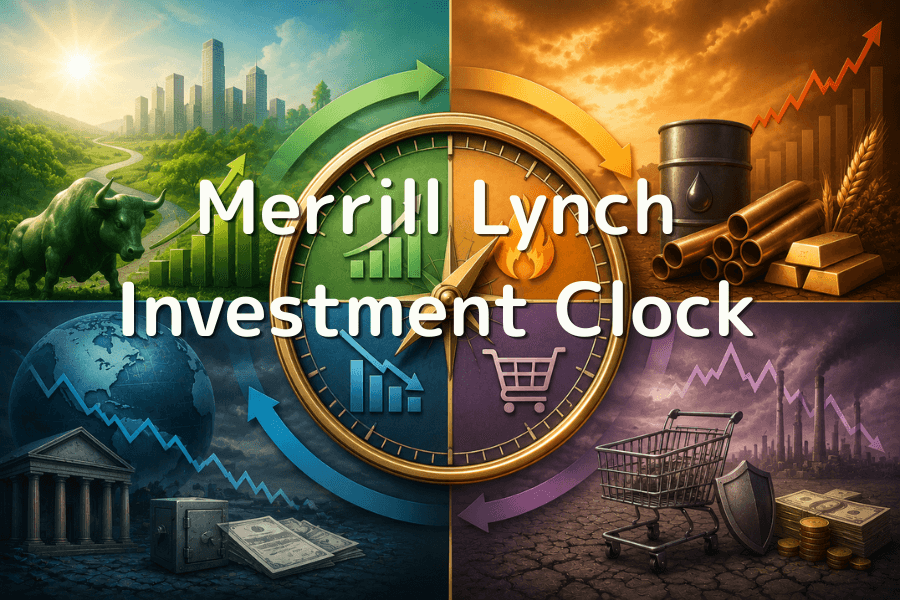

Combining these two indicators, the clock divides the cycle into four phases—recovery, overheat, recession, and stagflation. Each phase favors a different asset class, producing what is known as "asset rotation."

2. The Four Phases Explained: Features and Best Allocation

The Merrill Lynch Investment Clock splits the cycle into four phases; because growth and inflation differ in each, the favored asset class shifts too. Here are the features and allocation direction of each.

Phase 1: Recovery (growth turning up / inflation still low)

In the recovery phase, the stimulus from the earlier monetary easing gradually takes effect, unemployment starts to fall, and corporate orders and profits see their first improvement.

Because overall capacity utilization is not yet saturated, prices and inflation stay low, and the central bank keeps the cost of funds relatively cheap.

In this environment, stocks enter their prime allocation window—especially cyclical stocks tied to the economy and high-growth large caps, which tend to outperform the broad market as expectations for corporate profits surge.

Phase 2: Overheat (strong growth / high inflation)

As economic activity peaks, aggregate demand grows explosively and companies run into capacity limits.

This supply-demand imbalance quickly pushes up wages and prices, sharply increasing inflationary pressure, and the central bank formally enters a rate-hike cycle to keep the economy from running out of control.

In the overheat phase, commodities shine the most: raw materials such as crude oil, gold, energy, and industrial metals surge on strong real demand, making them the most effective hedge for capital against inflation.

Phase 3: Stagflation (growth turning down / high inflation)

This is the most challenging environment for investors. Growth has already lost momentum or even stalled, yet earlier over-issuance of money or supply-chain problems keep prices stubbornly high.

Corporate profits are squeezed hard by high operating costs, and the central bank, wary of side effects, cannot immediately cut rates to rescue the economy.

In the stagflation phase, cash and some defensive, inflation-resistant assets are the best protection. Traditional stocks and bonds mostly face downward pressure here, and raising the cash ratio is what preserves capital.

Phase 4: Recession (growth turning down / inflation falling)

When the overheating breaks, the market enters recession. Aggregate demand is extremely weak, corporate profits shrink sharply, and unemployment climbs.

To rescue the sagging economy, the central bank usually cuts rates repeatedly and eases policy to stimulate activity, driving real rates down quickly.

In a recession, bonds are the asset with the highest expected win rate—especially high-grade government bonds, because falling rates directly push up their prices, offering a hedge along with meaningful capital gains.

3. Limitations and Common Beginner Mistakes

The Merrill Lynch Investment Clock is a practical framework, but it is not flawless. In modern markets it has clear limitations that beginners should watch for.

Limit 1: The cycle is hard to predict precisely

Economic data usually lags. By the time the market confirms it has entered a phase, asset prices have often already reacted ahead of it, making it hard to catch turning points precisely and easy to fall into hindsight.

Limit 2: Interference from central-bank policy and external shocks

Modern central banks often intervene forcefully with unconventional tools such as quantitative easing, disrupting the natural cycle. On top of that, geopolitical events and supply-chain crises can suddenly change the direction of an expected phase shift.

Limit 3: Market expectations often lead the actual data

Financial markets are inherently expectation-driven. Investors often trade ahead of possible policy changes—buying bonds, for example, before the economy has clearly entered recession.

This speeds up phase transitions and can even scramble their order, something the market nicknames the "Merrill Lynch fan."

Common beginner mistakes

Many beginners treat the clock as a precise timer for short-term trading and lean on it too heavily to predict short-term moves.

In reality, the clock is better suited to judging medium- to long-term allocation direction, not as a basis for frequently switching stocks. Applying it too rigidly tends to cause repeated stop-outs amid sharp volatility.

The right way to use it is as a macro reference framework, combined with other technical and fundamental indicators for an overall judgment.

4. How to Apply the Clock in Real Investing

The greatest value of the Merrill Lynch Investment Clock is helping investors build a macro perspective and adjust allocation direction as the economic environment changes.

Application 1: Use central-bank policy as the main guide

Rather than staring at lagging economic data, it is more important to watch the policy stance and statements of major central banks such as the Fed.

A hiking signal usually means the market has entered the overheat phase, while cuts may hint that the economy is about to slow or enter recession. Central-bank signals are often a leading indicator of where capital flows.

Application 2: Combine with sector rotation

Sector performance differs clearly by phase.

In recovery, technology and consumer stocks are usually stronger; in overheat, energy and materials sectors tend to benefit.

Investors can moderately increase the weight of the relatively favored sectors for the current phase.

Application 3: Build a dynamic allocation framework

The clock is suited to guiding medium- to long-term allocation, not frequent short-term trading.

When you judge that a recession or stagflation phase has begun, raise the bond or cash ratio; in recovery, increase stock exposure. Regularly reviewing economic data and adjusting the ratios helps balance risk and return effectively.

Application 4: Strictly cap single-asset risk

Whatever phase the clock points to, you should set a cap on the allocation to any single asset or class (for example, no more than 10–15% of total capital). This limits losses when your judgment is wrong and keeps the account stable even if the phase shift exceeds expectations.

By using the clock as a macro reference tool alongside your own risk-management rules, you can respond more rationally to different economic environments and improve the stability of long-term allocation.

5. FAQ: Questions on the Merrill Lynch Investment Clock

Q1. How do I tell which phase of the clock global markets are in right now?

You can watch several key data points at once: the GDP growth rate, the Consumer Price Index (CPI), the Purchasing Managers' Index (PMI), and the direction of central-bank rate policy.

When growth is strong but inflation is starting to rise, it is usually the overheat phase; if growth slows while inflation stays high, it may be stagflation. Beginners are advised to start tracking the monthly data of major economies.

Q2. Is the clock suitable for short-term trading?

Not really. The clock is mainly for judging medium- to long-term allocation direction and reflects cyclical change on a quarterly or annual scale.

Short-term traders are better served by technical analysis and real-time sentiment, but understanding the current macro phase helps avoid trading against the larger trend.

Q3. What should I do when the phase the clock shows doesn't match the actual market?

This is common. Central-bank policy, geopolitical events, and supply-chain changes can all disrupt the traditional cycle.

Treat the clock as a reference framework rather than an absolute rule, combine it with other indicators for an overall judgment, control risk strictly, and don't bet all your capital on a single-phase forecast.

Q4. How should beginners protect assets during stagflation?

Stagflation is a relatively difficult phase. You can raise the ratio of cash or short-term bonds, allocate moderately to inflation-resistant assets such as gold, and reduce exposure to richly valued growth stocks. The priority is to protect capital and avoid taking excessive risk in a highly uncertain environment.

Q5. Can the clock be used alongside other investing methods?

Yes. Many investors combine it with technical analysis, sector rotation, or value investing. The clock is good at providing macro direction, while other tools handle the specific entry and exit timing—together they improve the overall quality of decisions.

6. Summary

The Merrill Lynch Investment Clock organizes the business cycle into four phases along two axes—growth and inflation—and points to the asset that leads in each: stocks in recovery, commodities in overheat, cash in stagflation, and bonds in recession. It is an intuitive macro framework.

That said, the lag in economic data, central-bank intervention, and the way market expectations run ahead mean the clock often does not turn exactly as theory suggests (the "Merrill Lynch fan"). That is precisely why it should be used as a compass for medium- to long-term allocation rather than a short-term forecasting tool—combined with other indicators, and with a firm cap on single-asset risk. Pairing a macro read of the cycle with disciplined money management is what lets you navigate different economic environments calmly.

Further Reading

- What Is the Business Cycle?

- What Is the Federal Funds Rate?

- What Is GDP?

- What Is CPI?

- What Is Quantitative Easing (QE)?

Titan FX Trading Strategy Lab. We produce investor-education content covering forex, commodities (crude oil, precious metals, agricultural goods), stock indices, US equities, and digital assets.

Primary Sources (by category)

- Model & academic: Trevor Greetham (Merrill Lynch, 2004) "The Investment Clock" — the original source of the Merrill Lynch Investment Clock; empirical work on the cycle and asset rotation

- Official statistics & data: U.S. Bureau of Economic Analysis (BEA) GDP; U.S. Bureau of Labor Statistics (BLS) CPI; ISM Purchasing Managers' Index (PMI)

- Central-bank policy: U.S. Federal Reserve — FOMC statements and rate decisions, a leading reference for reading the phase