QE(Quantitative Easing)

Quantitative Easing (QE) is an unconventional monetary policy in which a central bank, after interest rates have already fallen close to zero and conventional rate cuts have lost their effect, injects money into the market by purchasing large amounts of assets such as government bonds — aiming to push down long-term interest rates, boost liquidity, and stimulate the economy.

During the 2008 financial crisis and the 2020 COVID-19 pandemic, the term "quantitative easing" repeatedly made headlines, becoming the central weapon central banks used to fight crises. It matters because once the benchmark interest rate has fallen close to zero and conventional monetary policy stops working, QE is almost the only tool a central bank has to stimulate the economy on a large scale — and it deeply shapes the direction of stock, currency, and bond markets.

This article takes an in-depth look at the basic mechanics of QE, real-world examples around the globe, its impact on equities and exchange rates, its side effects and risks, and how investors should respond and position themselves — helping you gain a complete grasp of this key monetary policy tool.

- QE defined: its policy role once rates hit the zero lower bound

- Asset purchases: government bonds, MBS, corporate bonds, ETFs

- Impact across FX, equities, bonds, real estate, and commodities

- Case studies: Fed QE1–QE4, BoJ QQE, ECB APP/PEPP, BoE QE

- Side effects, the shift to Quantitative Tightening (QT), and investor strategy

1. What Is Quantitative Easing (QE)?

When conventional monetary policy (such as rate cuts) can no longer effectively stimulate the economy, a central bank launches "quantitative easing." QE works by purchasing large amounts of assets such as government bonds, corporate bonds, or mortgage-backed securities (MBS), which increases reserves in the banking system and thereby indirectly expands the money supply, encouraging credit expansion and economic activity.

In simple terms, QE is often described as "the central bank printing money to buy assets." While this is a slightly oversimplified metaphor, it captures how the market perceives QE's role in driving growth in the monetary base. Once funds flow into the market, they help push down interest rates, lift asset prices, and stimulate investment and consumption, in turn boosting the broader economy.

The History of QE

The First Experiment: Japan (2001)

The Bank of Japan was the first to implement QE in 2001, in an attempt to end prolonged deflation and economic stagnation — making it the first central bank in the world to adopt this tool.

Going Global: After the Financial Crisis (2008)

Following the outbreak of the 2008 global financial crisis, the U.S. Federal Reserve (Fed) launched a large-scale QE program that became the model other major central banks — such as the ECB, the Bank of England (BoE), and the Bank of Japan (BoJ) — would follow.

The Pandemic Era: Unprecedented Easing (2020)

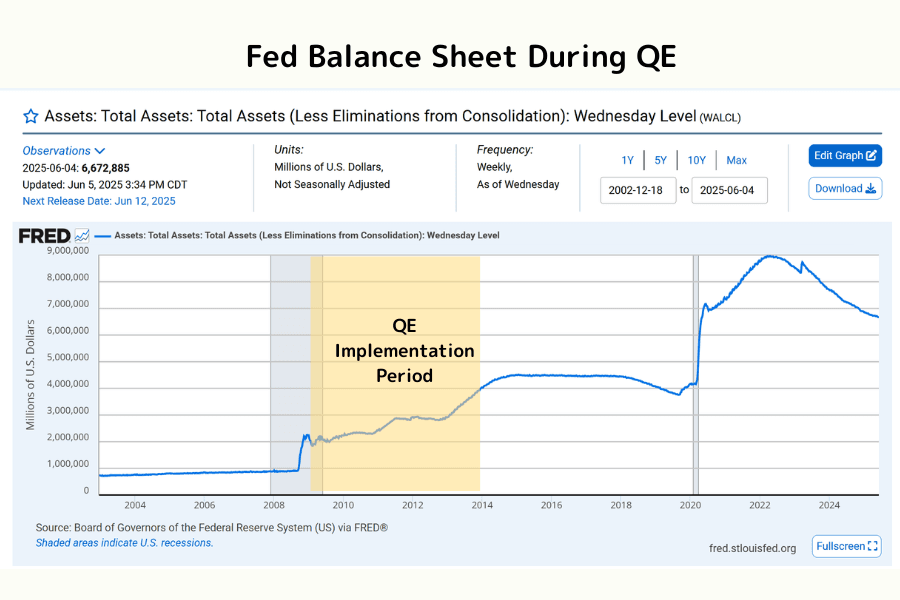

As COVID-19 spread in 2020, central banks worldwide acted swiftly to prevent economic collapse. In just three months, the Federal Reserve expanded its balance sheet from $4.2 trillion to $7.2 trillion, the fastest expansion on record. That year, central banks around the world bought more than $6 trillion in assets — far exceeding the combined total of all previous rounds of QE.

The Core Goals of QE

Goal 1: Boosting Market Liquidity

Injecting funds into the banking system to ease the pressure of a funding squeeze and credit contraction.

Goal 2: Lowering Long-Term Interest Rates

Pushing down yields on government and corporate bonds to reduce financing costs for businesses and households.

Goal 3: Stimulating Economic Activity

Encouraging corporate investment and consumer spending to drive GDP growth.

Goal 4: Stabilizing Financial Markets

Supporting asset prices such as stocks and housing to restore market confidence and the wealth effect.

2. How QE Works

When the economy faces recession risk, deflationary pressure mounts, unemployment rises, and conventional rate cuts have already approached the zero lower bound (ZLB), a central bank will launch quantitative easing (QE) as an unconventional monetary stimulus to prevent the downturn from spiraling out of control.

QE does not adjust interest rates directly. Instead, it actively intervenes in asset markets to inject large amounts of liquidity, further compressing financing costs, lifting investment and consumer confidence, and ultimately driving an economic recovery.

Its full mechanism can be broken down into the following four key stages:

① Asset Purchases (the starting point of liquidity injection)

Using newly created money, the central bank purchases large amounts of financial assets such as government bonds, corporate bonds, and mortgage-backed securities (MBS) in the open market.

The counterparties to these purchases are mainly commercial banks and financial institutions. By transferring these assets, the central bank effectively pays the new funds into the market, expanding the monetary base.

② Liquidity Spreads (banks' lending capacity rises)

Because commercial banks receive large amounts of funding from selling assets, their reserves increase sharply.

With ample funds and active financing demand, banks become more willing to lend and invest, fueling credit expansion. Market liquidity stays loose, helping to ease the risk of a credit crunch.

③ Interest Rates Fall (financing costs compress)

By buying bonds on a large scale, the central bank pushes bond prices higher, directly lowering bond yields — long-term rates in particular fall in tandem.

This brings about a decline in overall financing costs: corporate expansion and consumer credit become easier, while mortgage and auto loan rates fall as well, stimulating broader capital expenditure and consumption.

④ Economic Stimulus (aggregate demand recovers)

As corporate investment expands and household spending rises, the labor market warms up and consumer confidence recovers. Aggregate demand increases, putting economic growth back on track and modestly lifting inflationary pressure — helping the economy escape the risk of deflation and stagnation.

This is the cycle of outcomes QE ultimately aims to achieve.

The Economic Effects of QE (in theory)

Short-Term Effects

- Lowers corporate and household borrowing costs, quickly boosting the appetite for investment and consumption.

- Raises asset prices such as stocks and real estate, creating a wealth effect that further drives consumption.

- Strengthens financial market liquidity, preventing a funding squeeze and the spread of systemic risk.

- Improves bank balance sheets, increasing the capacity for credit expansion.

- If accompanied by currency depreciation, it can help boost export competitiveness.

Potential Long-Term Effects

- Sustained easy money can inflate asset bubbles, overheating markets such as tech stocks and real estate.

- Once asset prices decouple from the real economy, a future correction could trigger turmoil in financial markets.

- Long-term expansion of the money supply builds up inflationary pressure, eroding consumers' real purchasing power.

- Prolonged low rates squeeze the profitability of financial institutions, affecting bank lending and overall financial stability.

- Imbalances in global capital flows increase exposure to exchange rate and cross-border funding risks.

3. QE's Impact on Markets

QE affects not only the broad economic fundamentals but also directly reshapes the structure of financial markets. Investors can grasp its real-world effects through the following angles:

Impact 1: Inflation and Currency Depreciation

Because the money supply in the market increases, QE often pushes up inflationary pressure. With more money circulating, the purchasing power of the currency can decline — and on international markets, the currency's value often comes under depreciation pressure as a result. In addition, QE can channel funds into the stock market or other high-risk assets, pushing asset prices even higher and raising the risk of asset bubbles.

Impact 2: Liquidity in Equity and Capital Markets

QE usually raises market liquidity in the short term and lifts the stock market as a whole. After a central bank buys large amounts of government bonds and pushes interest rates down, funds tend to rotate into equities, real estate, and other risk assets. This flow of money helps invigorate capital markets and encourages companies to expand investment and financing.

Take stock indices as an example: during the periods of U.S. QE, major indices such as the S&P 500 and the Nasdaq 100 (NAS100) posted sharp gains. The NAS100 in particular benefited from money chasing the tech growth sector, with especially pronounced gains — making it one of the classic examples of QE's liquidity effect.

This approach, however, also carries risk. When funds are abundant and rates are too low, the risk awareness of companies and investors can decline, leading to high-risk investment behavior and increasing the potential for future market volatility.

Impact 3: Exchange Rate Effects

Quantitative easing usually leads to depreciation of the domestic currency. When a central bank injects large amounts of money into the market, it creates an oversupply of currency, which puts downward pressure on the exchange rate. In international trade, a weaker domestic currency can make exports more competitive, but it also increases the cost of imports.

4. Global QE Case Studies

QE in the United States

The United States was one of the pioneers of quantitative easing. Since the outbreak of the 2008 global financial crisis, the Federal Reserve has implemented three rounds of QE — QE1, QE2, and QE3.

QE1 (November 2008 – June 2010)

In this round, the Federal Reserve injected a total of $1.7 trillion to address the funding shortages caused by the financial crisis. The Fed bought government bonds and other financial assets on a large scale to lower market interest rates and increase liquidity, which effectively kept financial markets from collapsing.

QE2 (November 2010 – June 2011)

In this round, the U.S. injected another $600 billion to spur recovery and reduce unemployment. The goal of QE2 was to raise asset prices and encourage households and businesses to spend and invest more. The Fed further used bond purchases to push down long-term interest rates.

QE3 (September 2012 – October 2014)

QE3 was an open-ended quantitative easing program in which the U.S. injected $85 billion per month until gradually tapering from January 2014. This round of QE3 was aimed primarily at further reducing unemployment and stimulating economic growth. The move gave a strong boost to the stock market and improved credit markets.

QE in Japan

Japan was the first in the world to implement quantitative easing. Since 2001, the Bank of Japan has adopted a variety of unconventional monetary policies to combat economic weakness and actively promote recovery.

QE (March 2001 – March 2006)

This was Japan's earliest round of quantitative easing, increasing the money supply by changing the way financial markets were managed. With the Japanese economy mired in weakness, the Bank of Japan decided to adopt a zero interest rate policy and boost the supply of funds in the market by buying government bonds.

QQE (Quantitative and Qualitative Easing, April 2013 onward)

Under this policy, the Bank of Japan shifted its target from the unsecured overnight rate to expanding the monetary base, and began large-scale purchases of Japanese government bonds. The aim of QQE was to counter deflationary pressure and reach a 2% inflation target, thereby stimulating economic growth.

Negative Interest Rate Policy (January 2016 onward)

Japan went a step further with a negative interest rate policy, applying a negative rate to a portion of reserves to further stimulate liquidity. This policy was designed to encourage commercial banks to lend to businesses and to spur household consumption.

QE at the European Central Bank

The European Central Bank (ECB) began large-scale QE in 2015, primarily to address economic weakness and overly low inflation in the eurozone. The ECB's QE program included purchases of government bonds and other financial assets, injecting hundreds of billions of euros into the market each month.

QE (March 2015 – December 2018)

In this round, the ECB bought €60 billion of government bonds per month and kept interest rates relatively low, with the aim of promoting growth, reducing unemployment, and pushing prices higher. The policy helped the eurozone maintain relatively stable economic growth.

Continuation of QE and Balance Sheet Reduction

From 2018, the ECB began to reduce the pace of asset purchases and cut rates further in 2019. However, with the recovery still unstable, QE remained in effect.

QE in the United Kingdom

The UK's quantitative easing began in 2009, when the Bank of England started buying government bonds to address the post-crisis economic slump.

QE (March 2009 – October 2012)

The UK central bank first injected £200 billion, later raising the amount to £375 billion. The policy aimed to lower market interest rates and further stimulate economic growth.

Continuation and Adjustment of QE

As the post-crisis recovery progressed, the Bank of England continually adjusted the scale of its QE program, easing alongside other economies to achieve its economic and inflation targets.

5. Side Effects and Challenges of QE

While QE effectively stabilized the financial system and supported recovery during crises, structural risks gradually surfaced after prolonged implementation, and its costs must be assessed carefully:

Asset Bubble Risk

A flood of liquidity into the market pushes up the prices of stocks, real estate, and other high-yield assets, potentially causing asset prices to decouple from fundamentals. For example, after large-scale QE during the 2020 pandemic in the U.S., the S&P 500 and NAS100 repeatedly hit record highs, and U.S. home prices rose more than 15% in a single year. Once the market corrects or a rate-hike cycle begins, asset bubbles can burst sharply, triggering systemic financial turmoil.

Side Effects of Prolonged Low Rates

QE pushes long-term interest rates down, and a sustained low-rate environment squeezes banks' net interest margins, weakening the profitability of banks and insurers and affecting the stable development of the financial sector. In addition, prolonged low rates tend to induce excessive leverage and borrowing by businesses and households, building up debt risk and intensifying the pressure of future economic adjustment.

Rising Instability in the Financial System

An easy-money environment readily breeds high-leverage, high-risk investment behavior — for instance, the 2021 U.S. retail trading frenzy (the GameStop episode), the SPAC craze, and the wave of cryptocurrency speculation, all reflecting the excess-liquidity effect driven by QE. When market sentiment reverses, financial market volatility can be amplified rapidly.

Inflation and Purchasing Power Risk

As QE is sustained over the long term, the money supply rises sharply, pushing up inflationary pressure. In 2022, U.S. CPI surged to a 40-year high of 8.5%, forcing the Fed to accelerate rate hikes and tighten policy. If inflation is not brought under control in time, it can erode people's real purchasing power and even lead to a hard landing for the economy.

Widening Wealth Gap

QE reinforces the rise in asset prices, and asset holders (the wealthy) benefit the most, while lower-income groups face the dual pressure of rising living costs and soaring asset prices — further skewing wealth distribution. Wealth held by the top 1% of U.S. households expanded dramatically during the QE period, intensifying debate over social inequality.

6. QE Compared with Other Monetary Policies

Having understood the operating logic and practical impact of QE, we can compare it with conventional interest rate tools (such as rate cuts) and the corresponding tightening policy (QT). The table below summarizes the main differences among the three in terms of core goals, suitable timing, and potential risks:

| Policy Tool | Core Goal | When It's Used | Potential Risks |

|---|---|---|---|

| Rate Cuts | Lower financing costs, stimulate aggregate demand | When the economy slows but there is still room to cut rates | Zero-rate trap, runaway inflation expectations |

| QE | Add liquidity, push down long-end rates, stabilize financial markets | Financial crises, deflation, zero-rate environments | Asset bubbles, currency depreciation, worsening wealth distribution |

| QT | Drain liquidity, curb economic overheating | When inflation is high and liquidity is excessive | Credit contraction, asset repricing, recession risk |

As the table shows, the three policy tools each have their own application conditions and side effects. When choosing a strategy, a central bank must adapt to the current economic environment and market structure.

7. Frequently Asked Questions (FAQ)

Q1. How does QE differ from Quantitative Tightening (QT)?

QE increases the money supply to stimulate the economy; QT reduces liquidity to control inflation. QE lifts asset prices, while QT can weigh on both equity and bond markets.

Q2. How does QE affect investors?

QE lifts equities (such as the NAS100) and pushes down bond yields, favoring growth stocks and high-risk assets. Investors can trade indices and FX through Titan FX CFDs to capture these moves.

We recommend pairing this with the following Titan FX tools:

Real-Time Economic Calendar

Real-Time Economic Calendar: keep track of major global announcements

Global Economic Indicator Lookup Tool

Global Economic Indicator Lookup: track changes in data such as PMI and GDP

Q3. Could QE trigger hyperinflation?

If overdone, QE can push inflation higher, but hyperinflation requires the money supply to spiral out of control (as in 1920s Germany). The 2020–2022 QE did not trigger hyperinflation, though inflation did reach a 40-year high.

Q4. How can you trade the market opportunities QE creates?

Equities

QE lifts the NAS100 and S&P 500; we suggest using the RSI and Bollinger Bands to capture trends.

FX

Currency depreciation favors USD/JPY, EUR/USD, and other currency pairs.

Q5. How should investors position themselves during QE?

QE periods typically extend a "risk-on" environment. Common strategies include:

- Overweighting equities, real estate, and commodities

- Adding long-dated bonds (falling yields drive prices up)

- Diversifying into emerging market assets (low rates in developed economies drive inflows)

- Considering inflation hedges such as gold and crypto assets

Conversely, during QT, raise the weighting of cash and short-term bonds to cope with rising volatility. Shifts in central bank policy direction should be tracked continuously, with the portfolio adjusted step by step.

8. Conclusion

Quantitative easing (QE) is a key unconventional policy tool that central banks deploy in times of crisis, injecting large amounts of liquidity to stimulate economic growth and exerting a profound influence on stock, currency, and bond markets. From the U.S. QE1 through QE3 launched in 2008, to Japan's Quantitative and Qualitative Easing (QQE), QE played a pivotal role in driving the global recovery. At the same time, its implementation brings potential risks such as asset price bubbles, inflationary pressure, and uneven wealth distribution — so policy design and the timing of an exit must be handled with care.

Further Reading

- Open Market Operations (OMO) and Central Bank Policy

- Introduction to the Policy Interest Rate

- CPI (Consumer Price Index) Explained

- Profit Factor Explained

Titan FX Research Team. We cover a broad set of financial instruments — foreign exchange, commodities, equity indices, US equities, and digital assets — producing practical, research-backed educational content for traders.

Primary Sources (by Category)

- Central bank QE programmes: Federal Reserve, ECB Asset Purchase, Bank of Japan

- QE effectiveness research: BIS Unconventional Monetary Policies, IMF Quantitative Easing

- QT / Tapering data: FRB Balance Sheet Normalization, FRED Federal Reserve Total Assets