Net Asset Value (NAV)

When you buy into or redeem a mutual fund, the NAV is the price your money is converted at. It is the single figure that translates the value of everything the fund owns into a per-unit number you can act on.

NAV also reflects how the underlying portfolio is being valued on a given day. As the stocks, bonds, and cash held by the fund rise or fall in value, the NAV moves with them — which is why it is recalculated at the close of every trading day.

This article explains what NAV means, how it is calculated, whether a higher or lower NAV matters, what drives it up and down, and where you can look it up — so you can read the number correctly instead of being misled by it.

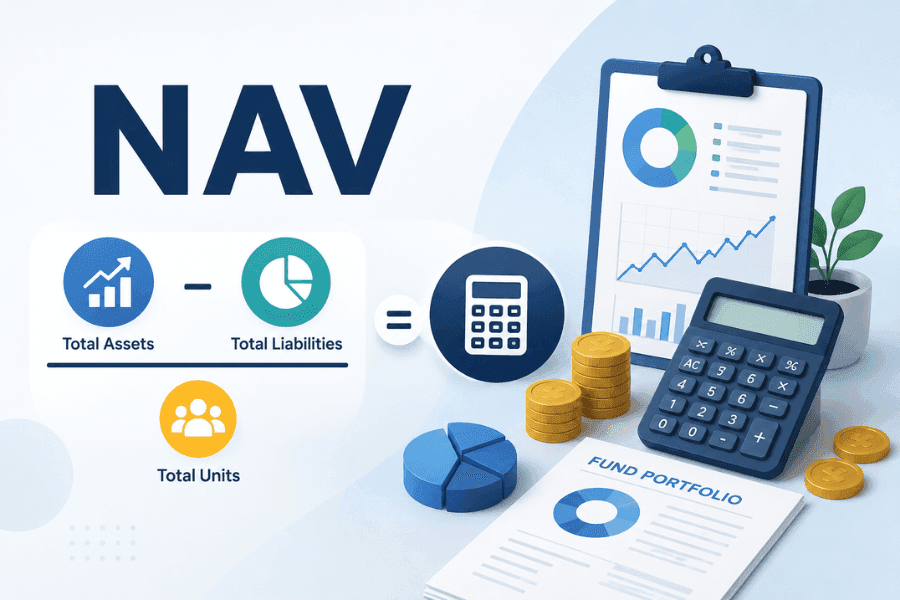

- NAV measures the per-unit value of a fund's net assets.

- NAV equals total assets minus total liabilities, divided by units outstanding.

- A high or low NAV alone says nothing about whether a fund is good.

- Market moves, currency shifts, internal fees, and distributions all affect NAV.

- NAV is the price basis when you buy or redeem fund units.

- Judge a fund on return, risk, fees, and strategy — not NAV level.

1. What Is NAV? The Core Concept

Net asset value (NAV) is the actual per-unit value of the assets a fund holds. It is also the main price basis used when investors buy or redeem units of that fund.

A mutual fund pools money from many investors and hands it to a professional management team to invest. The pool buys and holds assets such as stocks, bonds, and cash on behalf of everyone who has invested.

Take the total value of everything that pool owns, subtract the fund's operating costs and other liabilities, and divide by the total number of units outstanding. The result is the per-unit NAV you see quoted each day.

When you buy into a fund, your money is converted into a corresponding number of units. If the assets the fund holds rise in value, the NAV typically rises too, and you earn a capital gain; if markets fall and the assets lose value, the NAV falls in step.

2. How NAV Is Calculated: Formula and Example

Calculating NAV is relatively straightforward. The core formula is:

After each trading day closes, the fund company recalculates and publishes the latest NAV based on that day's closing prices.

Breaking Down the Components

- Total assets: the current market value of everything the fund holds — stocks, bonds, and short-term instruments — plus cash in the fund's account and any receivable dividends and interest.

- Total liabilities: the internal costs of running the fund, such as management fees, custodian fees, audit fees, transaction costs, and other payables.

- Units outstanding: the total number of units currently held across all investors in the fund.

A Worked Example

Suppose a fund has total assets of $1 billion, total liabilities of $50 million, and 95 million units outstanding:

NAV = ($1,000,000,000 − $50,000,000) ÷ 95,000,000 ≈ $10.00

This figure represents the actual value of a single fund unit. When you buy or redeem, your transaction is priced off this NAV.

The NAV is typically calculated by the fund company and, under applicable rules, checked by a custodian or other party — a process designed to keep the numbers transparent.

3. Is a Higher or Lower NAV Better? Busting a Common Myth

Many new investors assume that a lower NAV is "cheaper" and a higher NAV is "better." That is a common misunderstanding.

The NAV level on its own is neither good nor bad. What matters is the fund's long-term performance and your own cost of entry.

Myth 1: A Low NAV Is a Better Deal

The key to fund returns is the rate of return, not how many units you buy.

Suppose an investor puts $100,000 into a fund:

- Fund A has a NAV of $10, buying 10,000 units

- Fund B has a NAV of $100, buying 1,000 units

If both funds then rise 10%, Fund A becomes $11 (total value $110,000) and Fund B becomes $110 (also $110,000). The profit is identical. The number of units you hold does not change your return.

Myth 2: A High NAV Means the Fund Has Already Risen Too Much

A high NAV usually belongs to a fund that has been running for a long time with steady long-term performance. After years of compounding, the NAV naturally climbs — which may actually point to capable management, not to the fund being "too expensive."

How to Judge a Fund Properly

When investing in a fund, focus on:

- Long-term return and volatility

- Performance versus similar funds

- Consistency of the manager and the investment strategy

- The expense ratio

Understanding these points helps you view NAV rationally and avoid a common judgment trap.

4. What Drives NAV Up and Down

NAV moves every day, driven by a mix of internal and external factors. Understanding them helps you take daily swings in stride.

1. Market Performance of the Holdings

This is the most direct and most important driver. An equity fund's NAV rises and falls with the prices of its holdings — when the market rises, the NAV usually rises, and vice versa. A bond fund's NAV likewise reflects changes in bond prices.

2. Currency and FX Moves

Funds that invest overseas or hold assets denominated in foreign currencies are exposed to exchange rates. Even if the underlying asset prices are unchanged, a foreign currency weakening against your home currency can pull the converted NAV down.

3. Internal Fees

Operating costs such as management and custodian fees are deducted from fund assets daily and, over time, weigh on the NAV. All else equal, a fund with a lower expense ratio tends to have an edge in NAV performance.

4. Distributions and the Ex-Distribution Effect

When an income-paying fund makes a distribution, it hands part of its assets to investors. Total assets fall, and the NAV drops accordingly on the ex-distribution date. This is normal — it does not mean the fund has performed worse.

Keep a long-term perspective on these movements, and judge a fund alongside its type and your own risk tolerance rather than fixating on short-term NAV changes.

5. How to Check a Fund's NAV

Looking up a fund's NAV is a routine part of investing, and it is simple to do.

Where to Look

- The fund company's official website

- Your bank's or broker's investment platform

- The relevant fund industry association's website

- Financial-data sites (such as major finance portals)

How to Look It Up

Once you are on a platform, search for the fund by name or code to see the latest NAV and its historical chart. It is worth tracking the NAV regularly to observe the long-term trend and support your decisions.

6. NAV FAQ

Q1. Why does the NAV I look up today show yesterday's date?

A fund can only complete its asset valuation and reconciliation once every market it holds — at home and abroad — has closed for the day.

As a result, the final NAV for a trading day is usually published late that night or early the next morning. This is standard operating procedure, not an error.

Q2. Can a fund's NAV fall to zero?

For a well-diversified fund, the odds of the NAV hitting zero are low, but not impossible. If a fund's holdings fall sharply, its size shrinks too far, liquidity deteriorates, or performance lags for a long time, it may face liquidation, merger, or delisting. In that case the fund returns assets to investors in proportion to their holdings, based on the remaining asset value.

Q3. What is cumulative NAV, and how does it differ from regular NAV?

Cumulative NAV adds back every distribution the fund has paid since inception to its current NAV.

It gives a truer picture of the fund's total return — what it would have earned if distributions had been reinvested rather than paid out. For judging long-term performance, cumulative NAV is more useful than the plain NAV.

Q4. How can a beginner use NAV swings to lower risk?

Consider regular fixed-amount investing. By contributing a fixed sum on a set schedule, you buy more units when the NAV is low and fewer when it is high. Over time this averages your cost and eases the pressure of trying to judge whether the NAV is high or low at any single moment.

Q5. If the NAV drops after a distribution, does that mean the fund is doing worse?

No. This is the normal ex-distribution effect: part of the fund's assets has simply been converted to cash and paid out to investors. To judge performance, look at the cumulative NAV rather than the single-day drop right after the distribution.

7. Summary

NAV is one of the most central reference points when investing in a fund. It reflects the fund's actual value at a point in time and serves as the basis for buying, redeeming, and evaluating performance.

By understanding how NAV is calculated, what drives it, and the myths around it, you can avoid making decisions on a single number. Take a long-term view and weigh NAV alongside return, expense ratio, and your own risk tolerance.

Whether you invest a fixed amount on a schedule, track the long-term trend, or watch for the effect of distributions, these habits all help your assets grow steadily over time.

Related Articles

Titan FX Trading Strategy Lab. We produce investor-education content covering forex, commodities (crude oil, precious metals, agricultural goods), stock indices, US equities, and digital assets.

Key Sources (by category)

- Metric definitions & math: NAV = (total assets − total liabilities) ÷ units outstanding — the standard framework; general definitions of cumulative NAV and the expense ratio.

- Fund operation & disclosure: The general practice of valuing a fund and publishing NAV each trading day; the standard ex-distribution NAV adjustment.

- Investor education: Investor-education materials from financial regulators and fund associations — checking NAV and assessing performance.