Ponzi Scheme

"High return, low risk" investment pitches are hard to resist, yet the traps they hide must not be overlooked. The Ponzi scheme (Ponzi Scheme) — one of the oldest and most far-reaching financial frauds in history — continues to return to markets in new packaging, from postal-coupon arbitrage to hedge funds and fake forex trading platforms, leaving victims in every social class around the world.

This article walks through the mechanics of a Ponzi scheme, its recognizable features, real-world cases, differences from the pyramid scheme, practical protection strategies, and red flags specific to forex margin trading, to help you verify the legitimacy of an investment and keep your capital safe.

- A Ponzi scheme pays "returns" to existing investors out of new investors' principal — it creates no value and inevitably collapses.

- Four classic red flags: guaranteed high returns, unusually consistent returns, opaque structure, aggressive referrals to friends and family.

- Famous cases: Charles Ponzi (1920), Bernie Madoff ($65bn — the largest in history), MMM, Bitconnect.

- Warning signs: "X% per month" guarantees, redemption barriers, referral-bonus structures, no regulatory registration.

- Defensive playbook: verify regulator licensing (SEC / FCA / FINMA / VFSC), diversify, and be wary of emotion-driven sales.

- 1. Historical Background of the Ponzi Scheme

- 2. How a Ponzi Scheme Operates

- 3. Four Defining Characteristics of a Ponzi Scheme

- 4. Ponzi Scheme vs. Pyramid Scheme

- 5. Famous Ponzi Scheme Cases

- 6. Common Scenarios and Red Flags

- 7. Practical Strategies to Avoid Ponzi Schemes

- 8. Forex Margin Trading and Ponzi Schemes

- 9. Summary

1. Historical Background of the Ponzi Scheme

The term "Ponzi scheme" is named after Charles Ponzi, who rose to notoriety in early 20th-century America. In 1919 he launched an "International Postal Coupon arbitrage" operation, promising 50% returns in 45 days and attracting over 40,000 investors and more than USD 15 million in capital.

In reality, Ponzi never executed any substantive investment. He paid existing investors' "interest" with new investor deposits, sustaining an illusion of stable profits.

Although the scheme collapsed in 1920, the pattern has been imitated ever since. The 2008 Bernard Madoff case — estimated at USD 65 billion — stands as one of the largest modern Ponzi schemes, proving that this type of fraud remains a serious threat even in an era of stricter regulation.

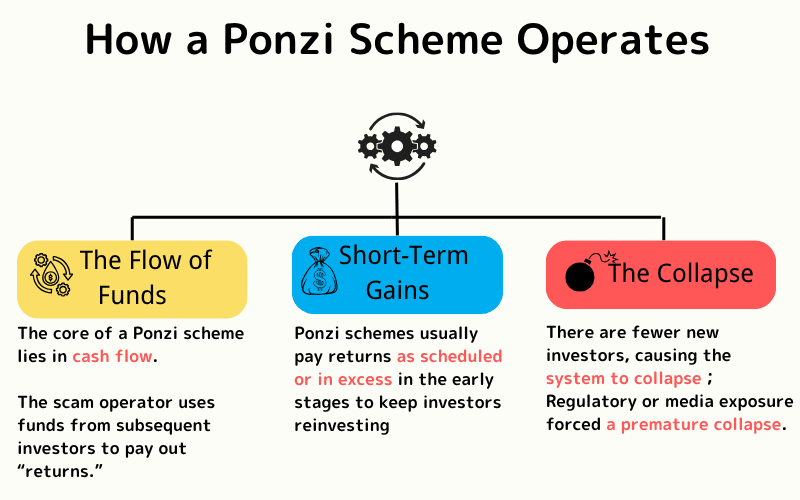

2. How a Ponzi Scheme Operates

At its core a Ponzi scheme does not generate profits by investing. Instead, it uses new capital to paper over earlier promises, maintaining the illusion of "high return, low risk". The typical flow has three stages:

Stage 1: The Illusion of Recycling Capital

The promoter first advertises above-market returns to attract capital, then uses new investors' funds to pay interest and principal back to earlier investors.

This unsustainable "capital pool" model can appear to work smoothly at the start, reinforcing investor trust.

Stage 2: Early Returns and Word-of-Mouth Expansion

Early investors who see profits tend to refer friends and family voluntarily.

This "chain of trust" strategy expands the funding base rapidly while reducing the pressure for detailed due diligence.

Fraudsters also cultivate a professional image, manipulate social media, and recruit endorsers to create an illusion of corporate legitimacy.

Stage 3: Collapse and Funding Breakdown

When the inflow of new capital can no longer sustain past commitments — or when regulators or media expose financial anomalies — the scheme collapses.

Investors can no longer withdraw funds, perpetrators often flee or face criminal charges, and most victim losses become unrecoverable.

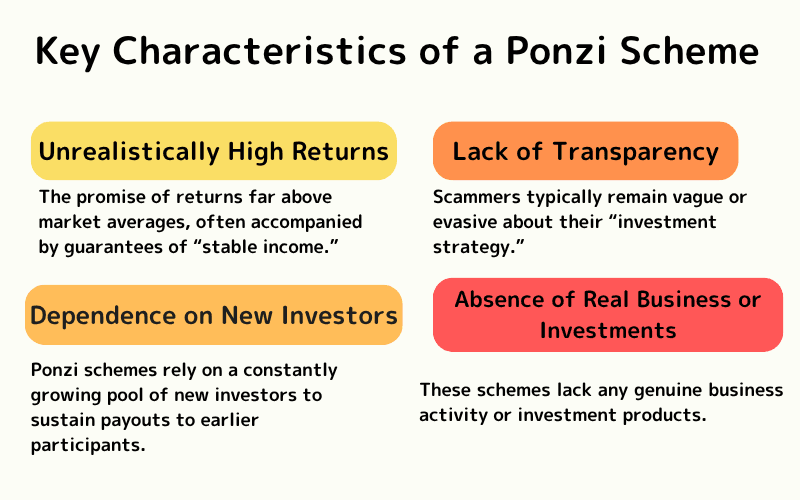

3. Four Defining Characteristics of a Ponzi Scheme

Identifying a Ponzi scheme comes down to observing how it runs and what it advertises. The four most telling red flags are:

Characteristic 1: Abnormally Steady and High Returns

Ponzi schemes advertise performance that ignores market conditions — always "15-20% or more annual" or "steady monthly profits". Real investments produce losses along with gains as markets move; fraud refuses to acknowledge uncertainty.

Characteristic 2: Opaque Investment Strategy

The pitch tends to describe investment with vague phrases such as "proprietary advanced algorithm" or "secret arbitrage method", with no concrete details. Questions are brushed off as "trade secrets".

Characteristic 3: Returns Depend on New Investors

If revenue for existing investors is coming from the capital of new investors — rather than actual business or investment income — that is a textbook Ponzi signature.

Characteristic 4: Absence of a Real Business or Product

Legitimate investments have tangible underlying assets (stocks, bonds, real estate, commodities). A Ponzi scheme offers only abstract "financial products" or "funds" with no concrete target.

4. Ponzi Scheme vs. Pyramid Scheme

Both schemes use new participant capital to pay existing participants, but the structures are clearly different.

Similarities

- New capital is used to pay "returns" to existing members

- No real investment profit is generated, so collapse is eventually inevitable

- Fraudsters pose as professionals or successful investors to win trust

Core Differences

| Comparison | Ponzi Scheme | Pyramid Scheme |

|---|---|---|

| Revenue pretext | Investment fund / trading strategy | Product sales / referral commissions |

| Structure | Centralized (perpetrator manages all funds) | Hierarchical (referral network) |

| Participant perception | Usually perceived as "investing" | Usually perceived as "sales / referral business" |

| Trigger of collapse | Shortfall of new investor capital | Slowdown of recruiting pace |

Real-World Comparison

- Ponzi-type: Bernard Madoff case (USD 65B, hedge-fund form)

- Pyramid-type: 1990s Albanian pyramid scheme in Europe, or various multi-level marketing operations that disguise themselves as product sales

5. Famous Ponzi Scheme Cases

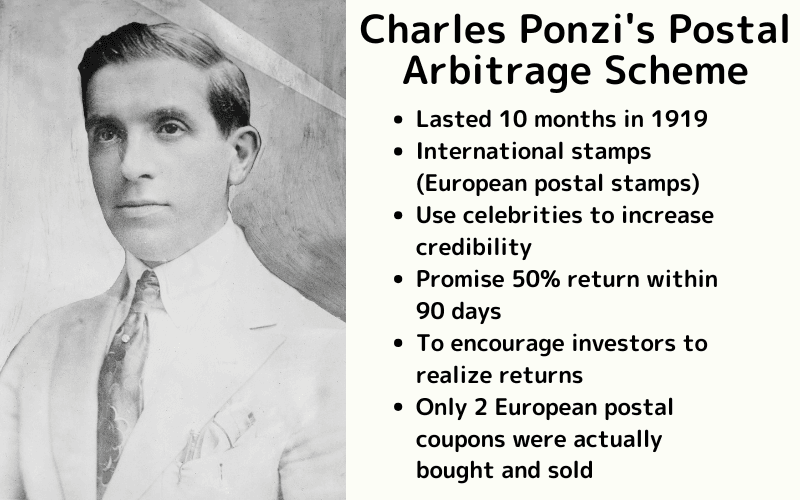

Case 1: Charles Ponzi's Postal Coupon Arbitrage

From 1919 to 1920, Boston-based Charles Ponzi promoted an "International Reply Coupon (IRC)" cross-border price-difference arbitrage, promising 50% returns in 45 days. At its peak it collected over USD 1 million per day and exceeded USD 15 million in total, yet very few actual coupon transactions took place. In August 1920, investigative reporting from the Boston Post exposed the operation and the scheme collapsed. Ponzi received a five-year federal prison sentence for fraud.

Case 2: The Collapse of Bernard Madoff's Financial Empire

In December 2008 it became public that the hedge fund of former NASDAQ chairman Bernard Madoff was a Ponzi scheme of roughly USD 65 billion. For about two decades Madoff falsified steady annual returns of 10-12% under a fictional "Split-Strike Conversion" strategy. Victims included celebrities, charities, and institutional investors, making it the largest individual financial fraud on record. Madoff was sentenced to 150 years in prison in 2009 and died in prison in 2021.

6. Common Scenarios and Red Flags

Ponzi schemes succeed not because investors are greedy, but because perpetrators understand human psychology and manipulate it skilfully. Below are three typical scenarios that lower guard, plus a summary of the red flags to remember (for a deeper list see the official Investor.gov Ponzi-scheme page run by the US SEC).

Scenario 1: Exploiting Personal Trust

Fraudulent plans often spread through family, friends, community leaders, or religious groups, creating a "hard to refuse" atmosphere that turns investing into an obligation of social courtesy.

Scenario 2: Time Pressure and Social Proof

Promoters use phrases like "limited slots" or "miss today and miss out forever" to create urgency, and show "already profitable" examples from other participants to activate bandwagon psychology.

Scenario 3: Jargon as a Smokescreen

Unfamiliar jargon such as "automated arbitrage", "high-frequency back-test model", "HFT (high-frequency trading)", or "capital pool" creates an impression of sophistication and safety, while in reality there is no real operation behind the curtain.

Red Flag Summary

- Cannot explain where money is actually deployed, only emphasizes return rate

- Dodges every question as a "trade secret"

- Access only through referral links; no public website or documentation

- Returns disconnected from market movement; no record of losses

Quick check: If an investment requires you to "recruit others, pay quickly, and not hesitate", it is much more likely a trap than an opportunity.

7. Practical Strategies to Avoid Ponzi Schemes

Recognizing red flags is only the first step. To genuinely protect yourself from Ponzi schemes, systematic capital management and pre-investment vetting are essential.

Strategy 1: Question Unreasonable Returns

Treat any plan offering "15-20% annual, steady" or "risk-free investment" with immediate skepticism. The long-term average annual return of the S&P 500 is about 10%; US Treasuries deliver 3-5%. Returns far above this range combined with "no risk" are almost never achievable.

Strategy 2: Verify Regulation and Background

Confirm on the official website whether the company is licensed by a major international regulator (FCA, ASIC, SEC, JFSA, CySEC, and so on). Be skeptical of vague claims such as "offshore regulation" or "holds an international license".

Strategy 3: Check Capital Flow and Reporting Transparency

Legitimate financial institutions publish segregated client funds, third-party audits, and regular financial reports. If none of these are available, or if "trade secrets" are used to refuse disclosure, the probability of fraud is high.

Strategy 4: Avoid Overconcentration on a Single Target

Even if a single opportunity is legitimate, concentrating most of your assets on it is a significant risk. Spread across asset classes, regions, and currencies to contain the damage from any single failure.

Strategy 5: Verify a Legal Exit Mechanism

Regulated brokers and financial firms typically guarantee withdrawals within 3-5 business days. Frequent "review", "delay", or "limit" on withdrawals suggests that the money may not exist.

Strategy 6: Keep Written Records and Communication Evidence

Preserve every contract, statement, email, and chat log. These records are critical evidence if you ever need to file a report or pursue legal action.

8. Forex Margin Trading and Ponzi Schemes

Forex margin trading (Forex Margin Trading) is a regulated, legitimate financial investment method used by many professional traders to build capital. Unfortunately, Ponzi operators frequently disguise their schemes as "legitimate trading platforms" to lure unsuspecting investors.

These frauds typically advertise "steady high returns" and "zero-risk guaranteed principal", and claim to operate a proprietary trading system or star trader. In practice, no real trades take place — capital from later investors simply flows to earlier participants.

Key Differences Between Regulated Forex Trading and Ponzi-Disguised Forex

| Item | Regulated Forex Margin Trading | Ponzi-Disguised Forex |

|---|---|---|

| Legality & regulation | Supervised by major financial regulators (ASIC, FCA, JFSA, etc.) | No license, or claims "offshore regulation" |

| Fund usage | Funds are deployed in real market trading; platform provides transparent statements | No real trading; fund flow undisclosed |

| Return profile | Returns fluctuate with the market (gains and losses, inherent uncertainty) | Advertises fixed returns (e.g. 10% monthly, 30% annual) |

| Withdrawal mechanism | Free withdrawal any time, typically within 3-5 business days | Reviewed, delayed, or restricted |

| Trade records & tools | MT4/MT5 platforms, technical indicators, risk-management tools | No real trading screens; only fake account statements or slides |

How Investors Can Protect Themselves

- Confirm that the trading platform is licensed by a major international regulator (FCA, ASIC, CySEC, etc.)

- Refuse any "guaranteed return" or "zero-loss" investment promise

- Choose a regulated broker such as Titan FX, with transparent quotes, free withdrawals, and segregated client funds

- When an unknown party actively pitches an investment plan, treat it with strong suspicion and refuse any private transfer

If a "forex investment opportunity" sounds too good to be true, it almost always is. Real forex trading carries risk and cannot escape market volatility. Only through professional knowledge, disciplined strategy, and a regulated platform can you achieve stable growth.

Further reading: Common Forex Trading Scams and How to Avoid Them

9. Summary

The danger of a Ponzi scheme lies not only in its disguised professionalism and tempting return promises, but in its manipulation of trust and social-proof instincts. By examining historical cases, operating mechanics, and warning signals, we can more clearly recognize the fraud's underlying nature.

Investors who maintain risk awareness, proactively verify a platform's legitimacy, focus on the transparency of capital flow, and reject every "guaranteed return" or "recruit-to-earn" pitch can put significant distance between themselves and the trap.

Even while pursuing asset growth, protecting principal should always be the first priority. Disciplined investing and refusing to follow the crowd are the only real path to controlling your own wealth.

Further Reading

- Insider Trading — A parallel category of financial crime; helps frame market integrity.

- IPO (Initial Public Offering) — Legitimate capital-raising vs the Ponzi structure.

- Derivatives — Regulated financial instruments, contrasted with disguised-investment frauds.

- Inflation — The "real return" concept exposes why guaranteed-rate offers are implausible.

- Monetary Policy — Framework for understanding the role of regulators and central banks.

- Asset Allocation — Diversification as a core defence against fraud and concentration risk.

The Titan FX Research team covers global macroeconomic indicators, foreign exchange (FX), commodities (oil, precious metals, agriculture), equity indices, US stocks, and crypto assets, producing educational content for investors and traders.

Primary Sources by Category

- Official data and regulators: U.S. Securities and Exchange Commission (SEC) — "Ponzi Schemes" investor bulletin; Investor.gov; Federal Trade Commission (FTC) — investment scam alerts; U.S. Department of Justice (DOJ) — Madoff prosecution records; Financial Industry Regulatory Authority (FINRA).

- International institutions and research: Financial Action Task Force (FATF) — anti-money-laundering guidelines; International Monetary Fund (IMF) — financial-integrity reports; International Organization of Securities Commissions (IOSCO) — cross-border fraud studies.

- Media and historical references: Bloomberg, Reuters, Wall Street Journal, Financial Times; Charles Ponzi (1920), Bernie Madoff (the 2008 collapse, $65bn — the largest in history), Allen Stanford ($8bn, 2009), MMM (Russia, 1990s), Bitconnect (2018), OneCoin (2014–2019).