Insider Trading

Insider trading is the buying or selling of securities by someone who holds "material, non-public" information about a company — or tipping others to trade on it. It breaches fairness and fiduciary duty and is a criminal offence in every major market.

In financial markets, "information is power" has never been merely a slogan. When information is distributed unevenly and a small group can move prices, the very foundation of market integrity is threatened — insider trading is the textbook example of this kind of misconduct, violating fair trading and eroding investors' fundamental trust in the market.

This article walks through the definition of insider trading, the elements required for a violation, real-world historical cases, legal consequences across major jurisdictions, and practical prevention strategies — helping readers build a compliant, risk-aware investing framework.

- Definition: trading securities on material, non-public information — a crime almost everywhere

- Five elements: insider status, MNPI, the trade, breach of duty, intent

- Penalties: SEC up to 3x disgorgement + 20 years; Japan 5y, Taiwan 10y

- Famous cases: Rajaratnam, Martha Stewart, Steve Cohen, Archegos

- Prevention: blackout windows, watchlists, Chinese Walls, audits

- 1. What is Insider Trading? Definition and Principles

- 2. The Five Elements of an Insider Trading Violation

- 3. Impact on Markets and Investors

- 4. Global Historical Cases

- 5. Legal Consequences Across Jurisdictions

- 6. How to Identify Suspicious Insider Trading Signals

- 7. How to Prevent Insider Trading Risk

- 8. Extended FAQ

- 9. Conclusion: Lessons From Insider Trading

1. What is Insider Trading? Definition and Principles

Insider trading refers to the buying or selling of publicly traded securities by individuals who possess material, non-public information about a company, in order to gain an unfair advantage. Such conduct violates the principle of information symmetry and causes serious harm to market fairness and investor interests.

Unlike ordinary market participants who can rely only on publicly available information, insiders often know key facts in advance — about earnings, strategic deals, or regulatory decisions — that allow them to anticipate future price moves. Two dimensions of asymmetry lie at the core of any insider trading case:

- Information asymmetry: a small group holds material non-public information that the market does not

- Timing advantage: those with access trade ahead of the public disclosure

Insider trading is not illegal because "trading produced a profit." It is illegal because the trade was based on material information that had not yet been made public — a breach of the market's rules of equal access. Even a loss-making trade can still qualify as insider trading if the decision rested on inside information.

How Does Insider Trading Occur?

- Company executives, finance teams, or in-house legal staff gain an information edge

- External consultants, auditors, lawyers, or accounting firms pick up sensitive data indirectly

- Investors encounter non-public information through personal relationships with insiders

- Media, analysts, or research organizations receive early disclosures about material decisions

Any trade executed before such information is public can amount to insider trading.

Distinguishing Legal "Informed Trading"

Legal trading rests on publicly disclosed information. Company executives may own and trade their own company's stock, but only after the relevant information has been disclosed through proper channels. Trading outside that window — even by an executive — can trigger a violation of insider trading rules.

An Illustrative Example

Imagine a company is about to announce a significant loss. An executive who knows this before the public release sells stock to avoid the impending decline — that trade is insider trading. The same sale after the news is public, and the market has processed it, is a legitimate transaction. The damage insider trading inflicts is to the trust foundation of open markets, preventing other investors from competing on equal terms.

2. The Five Elements of an Insider Trading Violation

Not every early trade amounts to insider trading. A case is typically evaluated against five core elements, all of which generally must be present for liability to attach:

- Element 1: Qualified status as an insider

- Element 2: Actual knowledge of non-public information

- Element 3: Information is material and specific

- Element 4: Trade occurs before the information becomes public

- Element 5: Instrument falls within the relevant statute

Element 1: Qualified Insider Status

The person in question must fall within a legally defined category of insiders. Common examples include:

- Company directors, supervisors, officers, and senior management

- Significant shareholders holding above a threshold (e.g., 10% in the US)

- Brokers, lawyers, accountants, and others with access through professional duties

- Tippees — individuals who receive inside information from a qualified insider and trade on it

Element 2: Actual Knowledge of Non-Public Information

The person must actually know the specific, non-public material information. Vague rumors or speculation are insufficient. Investigators typically focus on how the information was obtained and the sequence of trades relative to the information.

Element 3: The Information Is Material and Specific

The information must have a substantive effect on the security's price, such as:

- Earnings or loss revisions

- Major mergers, acquisitions, or divestitures

- Significant changes in dividend policy

- Senior management changes or corporate restructuring

- Material contracts, product approvals, or litigation outcomes

The information must be likely to influence a reasonable investor's decision.

Element 4: The Trade Occurs Before Public Disclosure

Trading must take place before the information becomes public, or during a short post-disclosure "digestion window" defined by the local regulator. Once the information is fully disclosed and absorbed by the market, trading is no longer an insider trading violation.

Element 5: Instrument Falls Within the Relevant Statute

Applicable instruments typically include listed equities, convertible bonds, warrants, and other equity-linked instruments. Pure foreign exchange, futures, or commodity trades are generally outside insider trading rules, unless they are indirectly linked to non-public corporate information.

All five elements typically need to be verified. A mere "insider trade" by status alone does not automatically become a violation.

3. Impact on Markets and Investors

Insider trading disrupts market mechanisms, damages transparency and public trust, and imposes long-run costs on both institutions and retail investors.

Impact 1: Damaged Market Fairness

Insider trading gives those with an information edge a head start, forcing other participants to absorb the risk and the loss — a direct breach of the principle of information equality.

Impact 2: Weakened Investor Confidence

When ordinary investors believe the market is driven by inside moves, participation declines, capital flows out, and trading thins, weakening the capital-market function over the long term.

Impact 3: Distorted Price Discovery

Trades ahead of disclosures push prices to abnormal levels before public information is available. The resulting price signals fail to reflect real supply, demand, or fundamentals, reducing the efficiency of capital allocation.

Impact 4: Higher Regulatory Enforcement Costs

Governments must devote more resources to detecting suspicious trades, prosecuting violations, and educating the market — costs ultimately borne by taxpayers and the financial system.

Impact 5: Corporate Reputation and Valuation Damage

When insider trading scandals involve a listed company, the stock often drops sharply, corporate governance credibility erodes, and future fundraising and strategic development are impaired.

4. Global Historical Cases

The following historical cases span multiple jurisdictions, illustrating how insider trading has arisen — and been addressed — across different markets.

Case 1: Martha Stewart (United States, 2001–2004)

American businesswoman Martha Stewart sold her ImClone Systems stock in December 2001, one day before the FDA announced the rejection of the company's cancer drug Erbitux application. Alerted by ImClone CEO Sam Waksal, Stewart avoided losses of approximately USD 45,000.

The US Securities and Exchange Commission (SEC) investigated, and Stewart was convicted of obstruction of justice and perjury (the insider trading itself was settled civilly). In 2004 she received a 5-month prison sentence, 5 months of home confinement, and paid approximately USD 195,000 in civil penalties. The case remains a milestone in US insider trading enforcement.

Case 2: Olympus Accounting Scandal (Japan, 2011)

In October 2011, Japanese optical-equipment manufacturer Olympus was revealed to have concealed around JPY 117 billion in investment losses over roughly 20 years through inflated "advisory fees" paid via complex acquisitions. Former CEO Michael Woodford's whistleblower disclosures prompted a broader investigation that included pre-disclosure trades by related parties.

Japan's FSA (Financial Services Agency) pursued liability under the Financial Instruments and Exchange Act. Executives involved received prison sentences and fines, Olympus itself paid more than JPY 700 million in fines, and the stock dropped roughly 80% in the weeks after the scandal broke.

Case 3: CITIC Pacific Derivatives Event (Hong Kong, 2008)

In October 2008, Hong Kong-listed CITIC Pacific (later CITIC Ltd) disclosed approximately HKD 15.5 billion in accounting losses on Accumulator hedges tied to Australian dollar exposure for its iron-ore project. The stock fell roughly 55% in a single session after the announcement.

Hong Kong's Securities and Futures Commission (SFC) investigated and alleged that executives had known of the potential loss before the formal disclosure but delayed announcement. Several directors were charged and the chairman resigned. The case led to reforms in Hong Kong's disclosure regime.

Case 4: Galleon Group (United States, 2009–2011)

Raj Rajaratnam, founder of hedge fund Galleon Group, was convicted in 2011 and sentenced to 11 years in prison along with approximately USD 156 million in fines and disgorgement — one of the most serious hedge-fund insider trading cases in US history. The SEC, for the first time, used wiretap recordings extensively as evidence, ensnaring former McKinsey director Rajat Gupta among other tippees.

Case 5: Asiasons Capital (Singapore, 2013)

In October 2013, shares of Singapore-listed Asiasons Capital (later Attilan Group) and two correlated stocks crashed more than 90% within two days, wiping out roughly SGD 8 billion in market capitalization. The Monetary Authority of Singapore (MAS) and the Commercial Affairs Department (CAD) launched a cross-border investigation, alleging market manipulation and insider trading. The case drove Singapore to strengthen real-time monitoring and amend the market-abuse provisions of the Securities and Futures Act.

Case 6: Taiwan Technology Company Acquisition (Taiwan, 2019)

A Taiwan-listed technology company planned an overseas acquisition in 2019. Before the public announcement, a senior executive tipped a family member, who purchased shares in advance and sold them after the price rose — realizing gains of more than TWD 10 million. Taiwan's Financial Supervisory Commission pursued charges under Article 157-1 of the Securities and Exchange Act; the individuals involved received prison sentences, fines, and were ordered to disgorge the gains.

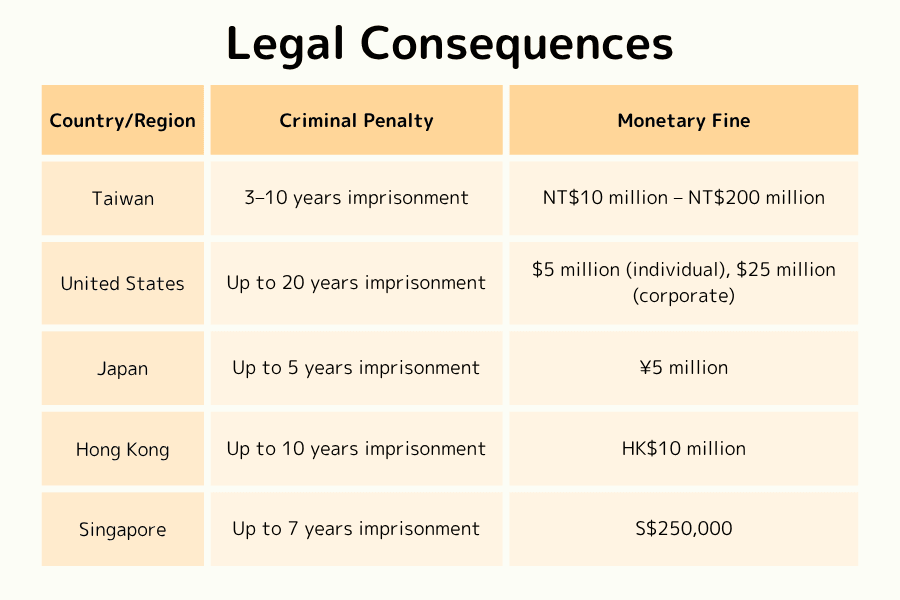

5. Legal Consequences Across Jurisdictions

Insider trading is a financial crime in most jurisdictions. The penalty frameworks below summarize the main markets; the actual penalties depend on the year and specific statute applied.

United States (Securities Exchange Act of 1934)

- Individuals: up to 20 years' imprisonment; fines up to USD 5 million

- Companies: fines up to USD 25 million; potential 3× disgorgement as punitive damages

- Regulators: SEC and the Department of Justice (DOJ)

Japan (Financial Instruments and Exchange Act)

- Imprisonment: up to 5 years

- Fines: individuals up to JPY 5 million; corporations up to JPY 500 million; plus administrative surcharge equal to illicit gains

- Regulators: Financial Services Agency (FSA) and Securities and Exchange Surveillance Commission (SESC)

Hong Kong (Securities and Futures Ordinance, Parts XIII/XIV)

- Imprisonment: up to 10 years

- Fines: up to HKD 10 million

- Civil sanctions: the Market Misconduct Tribunal can impose disqualification, cold-shoulder orders, and compensation orders

- Regulator: Securities and Futures Commission (SFC)

Singapore (Securities and Futures Act)

- Imprisonment: up to 7 years

- Fines: up to SGD 250,000; plus 3× illicit gains available as civil penalties

- Regulators: Monetary Authority of Singapore (MAS) and Commercial Affairs Department (CAD)

Taiwan (Securities and Exchange Act, Article 171)

- Imprisonment: 3 to 10 years

- Fines: TWD 10 million to TWD 200 million

- Administrative remedies: disgorgement of illicit gains and civil damages

- Regulators: Financial Supervisory Commission (FSC) and Taiwan Stock Exchange (TWSE)

6. How to Identify Suspicious Insider Trading Signals

For ordinary investors, recognizing suspicious trading signals helps avoid falling for fake "inside tips" and protects personal interests. Common warning signs include:

Signal 1: Abnormal Volume Before a Material Announcement

Unusual volume spikes 1–5 trading days before a major announcement (M&A, earnings, executive change, regulatory decision) are a classic warning sign. Regulators typically look back at such anomalies.

Signal 2: Atypical Options and Derivatives Activity

Short-dated out-of-the-money calls or puts spiking in open interest before a disclosure can signal that someone holds directional information. Since 2010, the SEC, SFC, and other regulators have made options markets a priority monitoring target.

Signal 3: Clustered Insider Filings

Listed-company directors and senior management must disclose holdings changes (such as US Form 4, or corresponding filings in other jurisdictions). Clustered buys or sells ahead of an announcement is a common red flag for both regulators and analysts.

Signal 4: Dubious Tip Sources

If a "can't-lose tip" comes from a contact, chat group, or paid community that lacks a public information trail, do not follow the trade — even if the tip turns out to be correct, trading on it can itself be illegal.

Signal 5: Stock Performance Diverging From the Broader Market

When the broader market is flat or mixed but an individual stock moves sharply in one direction without a public fundamental or technical explanation, check whether the company is approaching a material disclosure.

7. How to Prevent Insider Trading Risk

Effective prevention requires effort across institutional design, legal compliance, and individual conduct. Below are concrete steps for both companies and investors.

Strategy 1: Strengthen Corporate Governance

Companies should build strict internal controls and information classification. Access to highly sensitive data should be permissioned, and leakage risk should be reviewed periodically.

Strategy 2: Reinforce Timely Disclosure

Companies must proactively and promptly disclose information that could affect the share price, avoiding a situation in which only a small group holds material news and reducing information asymmetry at the source.

Strategy 3: Compliance Training for Employees

Regular legal-compliance training for insiders should emphasize that job duties or relationships must not be used to trade on non-public information. Written insider trading prevention rules and a reporting hotline should be in place.

Strategy 4: Internal Blackout Periods and Trading Restrictions

Executives and designated employees should be subject to blackout periods around earnings announcements and other material events. The US SEC's Rule 10b5-1 also offers a written pre-planned trading plan as a safe harbor, letting executives schedule future trades during non-material periods.

Strategy 5: Individual Investor Discipline

Ordinary investors who come into possible insider information should avoid trading the affected security and consult a professional to ensure their actions comply with the law and that the information source is legitimate.

Strategy 6: Reporting and Cooperation Mechanisms

When suspicious trades or information leaks come to light, report to the relevant regulator (SEC, FSA, SFC, MAS, local FSC, etc.). Most jurisdictions offer a whistleblower reward program — for example, the SEC Whistleblower Program pays 10%–30% of sanctions exceeding USD 1 million to qualifying tipsters.

Trade Global Markets Safely With Titan FX Titan FX provides FX, metals, stock indices, crude oil, and crypto CFDs on MT4/MT5. All quotes come from open markets — no single-stock inside-information risk. Up to 500× leverage, tight spreads, full long and short flexibility.

8. Extended FAQ

Q1. Does media-leaked information constitute insider trading?

Once information has been reported in mainstream media or formally announced on a company's disclosure platform, it enters the "public domain" and is no longer inside information. You should still verify the source's reliability and the exact time of public disclosure — some jurisdictions treat the first few hours after disclosure as an "absorption window."

Q2. Are analyst pre-publication reports considered inside information?

No. Reports that analysts publish based on public data and proprietary models are not non-public information; they are part of normal market activity. However, if an analyst obtained undisclosed material information from the company during research and used it as the basis for publication, that conduct could separately violate research-integrity rules.

Q3. Is there a statute of limitations for insider trading?

Yes. Limitation periods vary. The SEC's civil enforcement window is typically 5 years from the act (with some extensions), and Japan's Financial Instruments and Exchange Act provides 7 years. Loss of insider status (such as retirement) does not cleanse trades made while using information gathered during employment.

Q4. Does trading have to be profitable to constitute insider trading?

No. Even if the trade produces no profit — or a loss — it can still be an insider trading violation when built on material non-public information. The legal focus is on the information advantage, not on the realized gain.

Q5. Is giving inside tips without trading illegal?

Yes. Passing along or spreading material non-public information to others who then trade on it creates tipper/tippee liability, exposing the tipper to the same criminal, civil, and administrative consequences.

Q6. Does insider trading apply to FX (forex margin trading)?

Generally no. Insider trading rules apply primarily to equity markets and company-related instruments (corporate bonds, convertibles). There are narrow situations where similar legal risks can still arise:

① Company-Related Forex Trades

If someone uses non-public corporate information that directly affects exchange rates (e.g., an impending restructuring involving a large JPY-to-USD flow), a forex trade on that information may constitute insider trading or violate related market-abuse rules.

Example: A multinational is about to announce a capital restructuring involving a large transfer from JPY to USD. An insider trades FX in advance to profit, potentially breaching market rules.

② Non-Public Government or Central Bank Decisions

Using non-public government or central bank decisions (rate changes, monetary policy adjustments) to trade FX can trigger insider-trading-like liability, especially in jurisdictions with strict disclosure regimes.

Example: Someone learns through a private contact that a central bank is about to raise rates and buys that currency ahead of the announcement — potentially a violation.

Q7. Do ETFs and index products fall within insider trading?

Broad-based index ETFs (such as the S&P 500 or Nasdaq 100 ETFs) are usually too diversified for single-stock inside information to offer a tradable edge. However, sector ETFs or themed ETFs with concentrated holdings can become insider trading vehicles — if someone holds material non-public information on a heavily weighted component, buying the sector ETF can still attract liability.

9. Conclusion: Lessons From Insider Trading

Insider trading is not just a legal violation — it strikes at the very principle of a fair market. It represents a privileged few undermining the capital market's core value of information symmetry.

For investors, the takeaway is clear: lawful information sources and reasoned inference are the foundation of every trading decision. There are no shortcuts worth taking, and no reason to gamble on grey-area information.

Choosing legal, transparent, and compliant trading models is the only path to sustainable wealth accumulation. In an era of information overload, the scarcest commodity has never been inside information — it is discipline and principles.

Further Reading

- Ponzi Scheme — A parallel category of financial crime alongside insider trading.

- IPO (Initial Public Offering) — A setting where material non-public information frequently arises.

- Derivatives — Insider trades often use options or futures leverage to amplify gains.

- Monetary Policy — Pre-decision blackout regimes and the central-bank insider-information context.

- VIX Volatility Index — Unusual VIX moves have been used as enforcement clues.

- Asset Allocation — Diversification and avoiding suspicious information sources are basic personal risk management.

The Titan FX Research team covers global macroeconomic indicators, foreign exchange (FX), commodities (oil, precious metals, agriculture), equity indices, US stocks, and crypto assets, producing educational content for investors and traders.

Primary Sources by Category

- Official data and regulators: U.S. Securities and Exchange Commission (SEC) — Insider Trading Enforcement; U.S. Department of Justice (DOJ) — securities-fraud prosecutions; Financial Industry Regulatory Authority (FINRA); Japan FSA; Hong Kong SFC; Singapore MAS; Taiwan FSC; UK Financial Conduct Authority (FCA).

- International institutions and research: International Organization of Securities Commissions (IOSCO) — cross-border insider trading enforcement; Bank for International Settlements (BIS) — market-integrity studies; OECD — Corporate Governance Principles.

- Media and historical references: Bloomberg, Reuters, Wall Street Journal, Financial Times; landmark cases including Raj Rajaratnam / Galleon Group (2011, 11-year sentence), Martha Stewart (2004), Steve Cohen / SAC Capital (2013 settlement), Bill Hwang / Archegos (2024 verdict), Joseph Nacchio / Qwest (2007), and Mark Cuban / Mamma.com (acquitted 2013).