IRR(Internal Rate of Return)

IRR (Internal Rate of Return) is the discount rate that makes an investment’s net present value (NPV) zero, expressing its profitability as an annualized percentage.

The Internal Rate of Return (IRR) is a widely used metric in investment decision-making, measuring the annualized return of a project or investment.

It’s commonly applied in corporate finance, real estate, and startup evaluations to assess whether an investment is worthwhile.

However, IRR has limitations that can sometimes lead to flawed decisions.

Understanding its calculation, strengths, weaknesses, and proper application is crucial for investors and financial decision-makers.

This article explores IRR from its basics, detailing its calculation methods, its role in decision-making, and how to use it effectively for sound investment choices.

- What IRR measures and how it relates to the time value of money

- How to calculate IRR by finding the discount rate where NPV equals zero

- Using IRR vs. cost of capital to evaluate investment viability

- Limitations of IRR (reinvestment assumption, multiple solutions) and how MIRR addresses them

1. Definition and Basics of IRR

What is IRR?

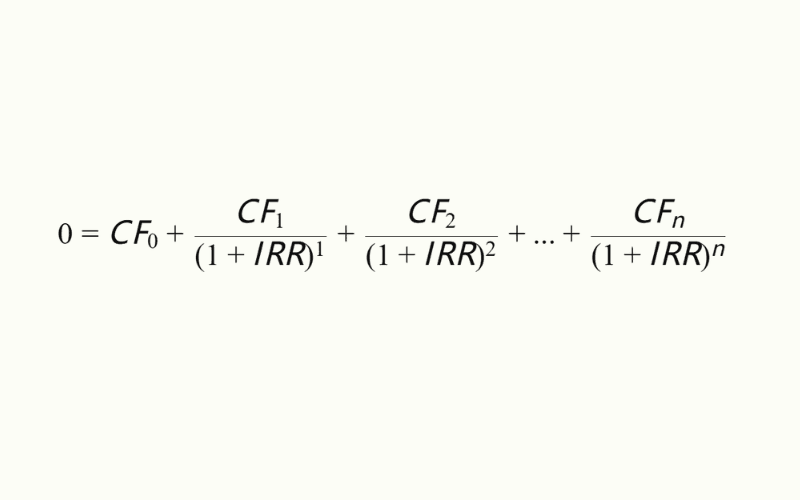

The Internal Rate of Return (IRR) is the discount rate that makes the Net Present Value (NPV) of an investment equal to zero. In simpler terms, it’s the annualized return at which the present value of future cash flows equals the initial investment.

IRR is rooted in the time value of money: a dollar today is worth more than a dollar in the future. It allows investors to evaluate how cash flows over time contribute to overall returns and decide if an investment is viable.

Comparison with Other Financial Metrics

| Metric | Meaning | Considers Time Value? | Best Use Case |

|---|---|---|---|

| IRR | Discount rate where NPV = 0 | Yes | Assessing long-term cash flow returns |

| NPV | Total discounted cash flow value | Yes | Determining if value is created |

| ROI | Total return ÷ total cost | No | Quick return estimation |

Where IRR is Used

IRR is a key tool in capital budgeting and investment analysis, with common applications including:

- Corporate Investments: Evaluating new equipment, production lines, or projects.

- Real Estate: Assessing rental income, resale value, and holding costs.

- Startups and Equity: Comparing potential returns across ventures or companies.

IRR provides a time-adjusted perspective on returns, helping decision-makers objectively compare options and select the most promising one.

2. How to Calculate IRR

IRR Formula

IRR is found by solving this equation to make NPV = 0:

Where:

- CF₀ = Initial investment (typically negative)

- CF₁, CF₂, ..., CFₙ = Cash flows per period

- IRR = The internal rate of return to be calculated

Calculation Examples

Simple Example

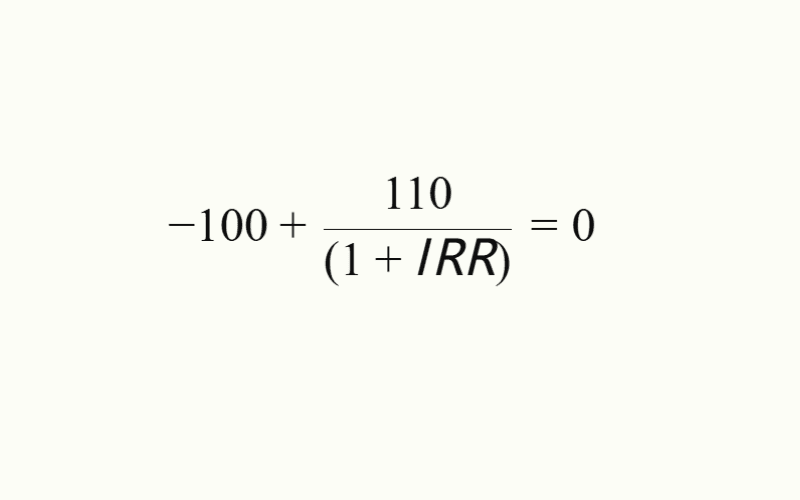

Suppose an investment costs $1 million and returns $1.1 million after one year. The IRR equation is:

Solving gives IRR = 10%, meaning the annualized return is 10%.

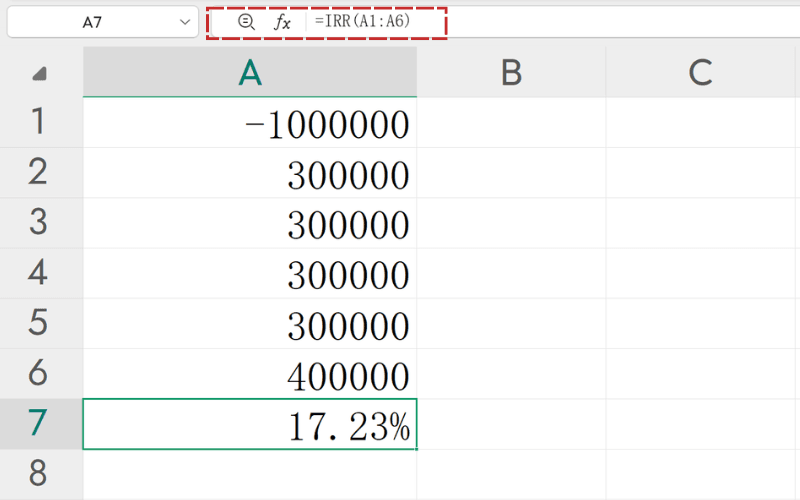

Excel Calculation

For more complex cash flows—say, an investment of $1 million with returns of $300,000 annually for four years, then $400,000 in year five—use Excel:

- ①Enter in cells A1:A6:

[-1000000, 300000, 300000, 300000, 300000, 400000] - ②In A7, input:

=IRR(A1:A6) - ③Result: IRR ≈ 17.23%

3. Using IRR in Investment Decisions

Is an Investment Worthwhile?

IRR is often compared to the cost of capital or a hurdle rate (minimum acceptable return):

- IRR > Cost of Capital: The investment is viable, promising positive returns above funding costs.

- IRR < Cost of Capital: The investment is risky, likely unable to cover funding costs.

This comparison is a standard practice for businesses and investors.

Case Study

A company considers buying equipment for $5 million, expecting annual savings of $1.5 million for five years. IRR calculation yields 14%. If the company’s cost of capital is 8%, since IRR exceeds it, the investment is economically sound.

Corporate Applications

IRR is used in scenarios like:

- Evaluating equipment purchases or upgrades.

- Allocating funds to new projects.

- Ranking multiple investment options.

Companies often set a minimum IRR threshold (e.g., 10%) for project approval.

IRR Ranges by Risk Level

| Risk Level | Typical IRR Range | Examples |

|---|---|---|

| Low Risk | 1%–5% | Savings accounts, bonds |

| Medium Risk | 5%–10% | Bond funds, balanced funds |

| High Risk | 15%+ | Stocks, venture capital |

Higher IRR isn’t always better—investors must align it with their risk tolerance and goals.

4. Advantages and Disadvantages of IRR

Advantages

- Time Value Consideration: IRR accounts for the time value of money, offering a more accurate return measure than ROI.

- Clear and Intuitive: Expressed as a percentage, it’s easy to understand and compare across options.

- Versatile: Useful for corporate projects, real estate, or startup evaluations.

- Ranking Tool: Helps prioritize investments when resources are limited.

Disadvantages

- Unrealistic Reinvestment Assumption: IRR assumes cash flows are reinvested at the IRR rate, which may exceed real-world rates, inflating estimates.

- Multiple Solutions: Cash flows with multiple sign changes (positive to negative) can yield multiple IRRs, complicating interpretation.

- Short-Term Bias: IRR favors quick, small returns over larger, longer-term gains (e.g., a 15% IRR small project might yield less than a 10% IRR large one).

Addressing IRR’s Flaws

To avoid misjudgments, pair IRR with these tools:

| Method | Description |

|---|---|

| NPV | Complements IRR by showing total value created, not just rate |

| MIRR | Adjusts reinvestment rate to market conditions, avoids multiple IRR issues |

MIRR (Modified Internal Rate of Return) improves on IRR by assuming cash flows are reinvested at a realistic market rate (e.g., cost of capital), providing a single, practical result.

5. Frequently Asked Questions (FAQ)

Q1: What is IRR?

IRR, or Internal Rate of Return, is the discount rate that makes an investment’s NPV zero—an annualized return metric.

Q2: How is IRR Calculated?

Use Excel’s =IRR() function with a series of cash flows. It iteratively finds the rate where NPV = 0. Complex cases may need financial software.

Q3: What’s a Reasonable IRR?

It depends on risk and cost of capital:

| Risk Level | Typical IRR Range |

|---|---|

| Low Risk | 1%–5% |

| Medium Risk | 5%–10% |

| High Risk | 15%+ |

An IRR above your cost of capital or target rate signals a worthwhile investment.

Q4: Is Higher IRR Always Better?

Not necessarily. High IRR might reflect high risk, short-term cash flows, or low total returns. Check NPV too.

Q5: How Do IRR and NPV Work Together?

IRR measures efficiency; NPV shows total profit. An investment is ideal when IRR exceeds cost of capital and NPV is positive.

6. Conclusion

IRR is a powerful tool for evaluating investment returns, widely used by investors and businesses.

However, its assumptions—like reinvesting at the IRR rate—and potential for multiple solutions mean it shouldn’t stand alone.

Pairing IRR with NPV, cost of capital, and risk analysis ensures more reliable decisions.

Further Reading

- What Is ROI (Return on Investment)?

- What Is Compound Interest?

- What Is the Sharpe Ratio?

- What Is Maximum Drawdown (MDD)?

- Forex Trading Basics

Titan FX Research. We produce educational content for investors, covering a wide range of financial instruments including forex, commodities (crude oil, precious metals, agricultural products), stock indices, U.S. equities, and digital assets.

Primary Sources (by Category)

- Finance theory: Investopedia — Internal Rate of Return (IRR); CFA Institute — Capital Budgeting

- Practice: Corporate financial reports; MoneyForward — IRR calculation

- Tools: Microsoft — Excel IRR function documentation