Compound Interest

Compound interest is a method where earnings are reinvested into the principal so that interest itself earns interest — its power comes from time, growing your money exponentially over the long run.

From forex and fund investing to retirement planning, compound interest is one of the most powerful forces for building long-term wealth.

In this guide, we'll break down exactly how compound interest works, how it compares to simple interest, and proven strategies to make it work for you.

- Formula: FV = P × (1 + r)^n

- Mechanism: interest earns interest, compounding over time

- vs simple interest: about $104,340 more over 30 years

- Time matters: weak early, exponential after 20+ years

- 6 strategies: reinvest, Rule of 72, low fees, tax-advantaged accounts

1. Understanding Compound Interest?

Compound interest refers to the method where investment earnings are reinvested along with the principal, creating a snowball effect of growth over time.

The key characteristic is that each reinvestment calculates new interest based on both the original principal and accumulated interest from previous periods. This creates accelerating returns as reinvestment continues.

This "interest earning more interest" mechanism, known as the compound interest effect, is the driving force behind long-term wealth accumulation.

Albert Einstein famously called compound interest the "eighth wonder of the world", highlighting its transformative power for building wealth.

How to Calculate Compound Interest

Compound Interest Formula: Principal × (1 + Annual Interest Rate) ^ Years

Example: For a $100,000 principal at 4% annual interest over 10 years:

$100,000 × (1 + 0.04)^10 = $148,024

How Compounding Frequency Affects Returns

The formula above assumes interest is compounded once a year (annual compounding). In practice, interest may be added to the principal quarterly, monthly, or even daily — and the more frequently it compounds, the stronger the effect. Adding the compounding frequency, the formula becomes:

FV = P × (1 + r / m) ^ (n × m)

- m: number of compounding periods per year (annual = 1, quarterly = 4, monthly = 12, daily = 365)

For a principal of $100,000 at 4% over 10 years, the final values under different compounding frequencies are:

| Compounding Frequency | Periods per Year (m) | Value After 10 Years |

|---|---|---|

| Annual | 1 | $148,024 |

| Quarterly | 4 | $148,886 |

| Monthly | 12 | $149,083 |

| Daily | 365 | $149,179 |

| Continuous | approaching infinity | $149,182 |

More frequent compounding produces a higher value, but the gains taper off and converge toward the theoretical ceiling of continuous compounding (FV = P × e^(r×n), where e ≈ 2.718). So when comparing savings or investment products, look beyond the nominal rate and check how often it compounds.

2. Understanding Simple Interest

Simple interest is a calculation method where earnings are not reinvested.

Since the principal remains constant, each period generates fixed interest payments, resulting in linear growth.

How to Calculate Simple Interest

Simple Interest Formula: Principal × (1 + Annual Interest Rate × Years)

Example: Same $100,000 principal at 4% over 10 years:

$100,000 × (1 + 0.04 × 10) = $140,000

3. Compound vs. Simple Interest: Key Differences

Albert Einstein famously remarked: "Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn't, pays it."

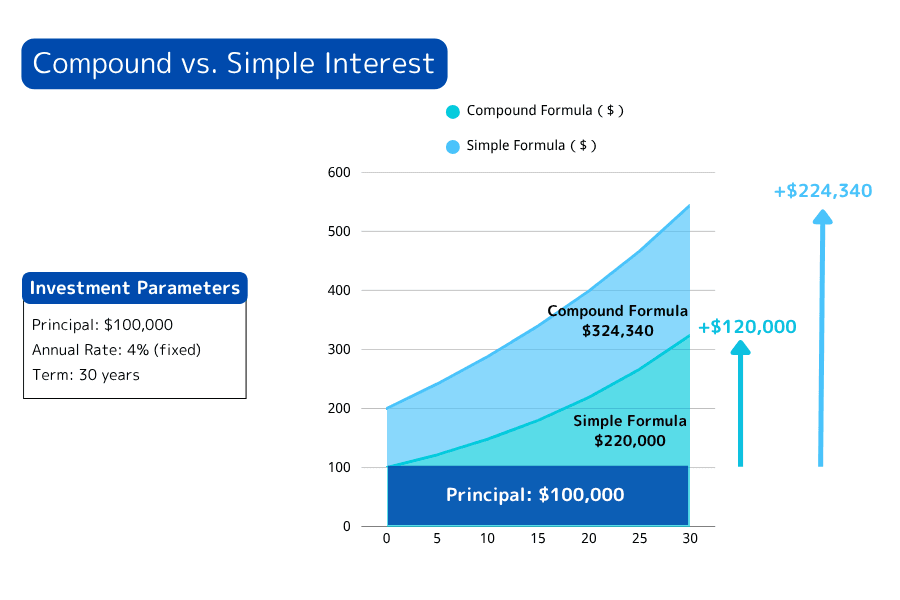

This comparison shows how time and reinvestment create a staggering $104,340 difference from the same $100,000 principal over 30 years at 4% annual interest.

Investment Parameters

- Principal: $100,000

- Annual Rate: 4% (fixed)

- Term: 30 years

- Compound Formula:

Principal × (1 + Rate)^Years - Simple Formula:

Principal × (1 + Rate × Years)

Wealth Growth Comparison

| Year | Compound Value | Simple Value | Advantage |

|---|---|---|---|

| 0 | $100,000 | $100,000 | $0 |

| 5 | $121,665 | $120,000 | +$1,665 |

| 10 | $148,024 | $140,000 | +$8,024 |

| 15 | $180,094 | $160,000 | +$20,094 |

| 20 | $219,112 | $180,000 | +$39,112 |

| 25 | $266,584 | $200,000 | +$66,584 |

| 30 | $324,340 | $220,000 | +$104,340 |

4. 6 Powerful Compound Interest Strategies

Strategy 1: Long-Term Investing with Reinvestment

Maintain investments over extended periods and consistently reinvest dividends, interest, and capital gains. This creates a continuous growth cycle where earnings generate more earnings - the essence of compounding.

Strategy 2: Apply the Rule of 72

Divide 72 by your annual return rate to estimate doubling time. Example: At 6% returns, investments double in about 12 years. This quick calculation helps set realistic expectations for wealth accumulation.

Strategy 3: Prioritize Return Rates

Focus on investments with stable, competitive returns. Even a 1-2% higher annual return creates dramatic differences over decades due to exponential growth.

Strategy 4: Dollar-Cost Averaging

Invest fixed amounts regularly regardless of market conditions. This disciplined approach:

- Smooths out purchase prices

- Reduces timing risk

- Builds positions gradually

Strategy 5: Minimize Costs

Choose low-fee instruments (ETFs, index funds) and avoid excessive trading. Every 1% saved in fees can add tens of thousands to long-term returns.

Strategy 6: Leverage Tax-Advantaged Accounts

Many countries and regions offer tax-advantaged accounts for investment earnings, with tax-free or tax-deferred growth (the specific schemes, conditions, and eligibility vary by your location and broker). Where available, using them effectively boosts your compounding rate.

Pro Tip:

Combine multiple strategies for maximum effect - e.g., regular contributions to low-cost index funds in a tax-advantaged account.

5. Compound Interest FAQs

Q1. Are there any drawbacks to compound interest?

While compound interest can grow assets like a snowball over time, there are potential downsides:

- ▸ Negative returns compound losses more severely than simple interest

- ▸ Sustained losses accumulate more dramatically over long periods

- ▸ During market downturns, this "reverse compounding" accelerates capital erosion

Q2. How long does it take to see compound interest effects?

The power of compounding correlates directly with investment horizon:

- ▸ Short-term (1-5 years): Minimal noticeable impact

- ▸ Medium-term (10-15 years): Begins accelerated growth phase

- ▸ Long-term (20+ years): Exhibits exponential growth characteristics

Following power-law mathematics, its growth curve displays exponential properties, ultimately surpassing linear simple interest by widening margins. See §3.

Q3. Does compound interest apply to all investments?

Not necessarily. Compounding applies to most instruments that generate continuous returns — reinvested stock dividends, fund distributions, forex swap interest, and bond coupons.

However, assets without stable cash flow (some high-risk derivatives or short-term speculation) cannot fully harness the effect. See §4.

Q4. What should I watch for when compounding in forex trading?

In leveraged forex (margin) trading, compounding can accelerate growth but also amplifies risk:

- Swap interest: rate differentials between currency pairs affect the compounding effect

- Leverage risk: leverage magnifies gains, but losses also compound when the direction is wrong

- Risk management: a steady long-term strategy harnesses compounding better than chasing short-term returns

See §4.

Q5. Does compound interest only work in your favor?

No. Compound interest is a double-edged sword: it accelerates the growth of your investments, but it also makes debt snowball just as fast.

▸ Credit card revolving interest: unpaid balances typically compound daily at annualized rates often above 15%, so debt balloons quickly

▸ Loans and installments: mortgages, car loans and similar products also compound — the longer the term and the higher the rate, the heavier the cumulative interest

▸ Takeaway: put compounding to work on the asset side (long-term investing, reinvesting returns) while avoiding high-interest debt, so compounding works for you rather than against you

6. Summary:

Compound interest is a method of growing wealth by reinvesting earnings into the principal, allowing interest to accumulate on both the initial amount and the interest itself. Unlike simple interest, which only applies to the principal, compound interest creates exponential growth by continuously reinvesting earnings.

The real power of compounding comes from its dependence on time—the longer the investment horizon, the more significant the growth. To fully leverage compounding, it’s essential to maintain a long-term investment strategy, choose high-quality assets, apply the Rule of 72 to estimate how long it takes to double your investment, and take advantage of tax-advantaged accounts to maximize growth.

Further Reading

- What is the Rule of 72?

- What is Kelly Criterion?

- What is Volatility?

- What is Forex Leverage?

- Forex Trading Basics

Titan FX Trading Strategy Lab. We produce investor-education content covering forex, commodities (crude oil, precious metals, agricultural goods), stock indices, U.S. equities, and digital assets.

Primary Sources (by category)

- Mathematical foundation: ln(2) ≈ 0.6931 — natural-log basis for compound doubling (Rule of 72 derivation)

- Historical origin: Pacioli, L. (1494) Summa de arithmetica, geometria, proportioni et proportionalità — earliest documentation of compound interest and the Rule of 72

- Empirical compounding & long-run returns: Federal Reserve Bank of St. Louis (FRED) — US S&P 500 historical returns; MSCI World Index 30-year returns

- Einstein attribution: The "8th wonder" quote attributed to Einstein has multiple secondary-source citations (Quote Investigator etc.) but no direct primary source has been verified — treated as anecdote