Kelly Criterion

In trading, most participants focus on finding precise entry points — yet a more critical question often goes overlooked: how much capital to commit on each trade.

Even a strategy with a 60% win rate can erode an account quickly if individual trades carry too much risk. The traders who survive long-term obsess over position management more than entry timing.

The Kelly Criterion was built precisely for this problem. It uses probabilities and reward/risk structure to compute the theoretically optimal allocation per trade, helping traders strike the balance between growth and ruin.

- Formula: f* = (bp − q) ÷ b — where f* is the optimal fraction, b is the reward/risk ratio, p is the win rate, and q is the loss rate

- Mathematical origin: Published by Bell Labs mathematician John L. Kelly Jr. in the 1956 Bell System Technical Journal. Originally derived from information theory; later applied to gambling and investment.

- Core goal: Maximize long-term compound growth without ruin

- Practical variant: Half Kelly retains ~75% of theoretical growth while halving drawdown — most professional traders use Half or Quarter Kelly

- Prerequisites: 50–100+ real trades to estimate win rate and reward/risk; beginners often overestimate win rate, which leads to over-exposure

1. What is the Kelly Criterion? Core Concept

The Kelly Criterion was first published by Bell Labs mathematician John L. Kelly Jr. in the 1956 Bell System Technical Journal as a result in information theory. It was later applied to gambling and investing, where its core purpose is to compute the optimal fraction of capital to commit per trade — assuming a positive expected value — so that long-term compound growth is maximized.

It is also commonly called the Kelly formula in trader-facing literature.

Trait 1: Maximize Capital Growth

The formula's essence is balancing risk and reward. It does not chase one-shot windfalls — it asks: how can capital climb fastest without going to zero?

Trait 2: Probability-Driven, Not Intuition-Driven

Position size isn't a gut decision — it derives from the win rate and reward/risk ratio that your trading system produces. The more stable those parameters, the more usable Kelly's output becomes.

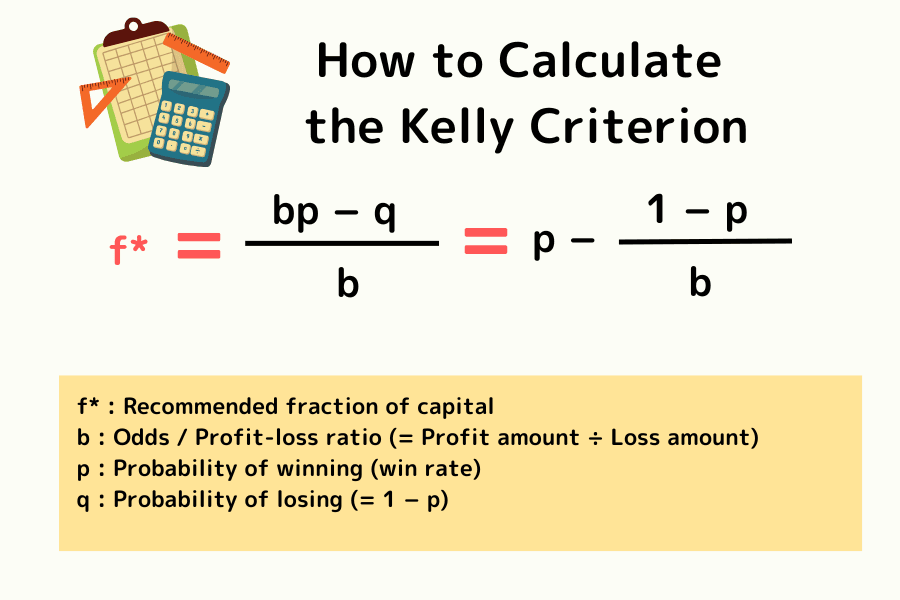

2. How to Calculate the Kelly Criterion

We present both the mathematical original and a trader-friendly simplification.

Original Mathematical Formula

The standard form found in academic and gambling literature:

f* = (bp − q) ÷ b

| Variable | Meaning |

|---|---|

| f* | Recommended fraction of capital |

| b | Net odds on a win (= average winning amount ÷ average losing amount) |

| p | Probability of winning (win rate) |

| q | Probability of losing (= 1 − p) |

Trading-Oriented Simplification

In financial trading, defining b as the reward/risk ratio gives an equivalent but more intuitive form:

- Bet fraction = win rate − loss rate ÷ reward/risk ratio

- That is: f* = p − (1 − p) ÷ b

Worked Example

Strategy: win rate 40% (p=0.4), loss rate 60% (q=0.6), wins pay 3 (b=3), losses cost 1.

- Original formula: (3 × 0.4 − 0.6) ÷ 3 = 0.6 ÷ 3 = 0.2

- Simplified form: 0.4 − (0.6 ÷ 3) = 0.4 − 0.2 = 0.2

- Reading: To maximize long-term growth, the theoretical maximum risk fraction per trade is 20%.

3. Practical Guide: 5-Step Application to Trading

Five steps to translate Kelly's math into actual orders.

Step 1: Pull Historical Trade Data

Gather at least 50–100 real trade records or a meaningful backtest. The more data, the more representative the parameters become. If your style (e.g., stop-loss habits) recently changed, older data loses relevance.

Step 2: Estimate Win Rate

Divide profitable trades by total trades to get p.

A win rate below 40% means your strategy needs an unusually high reward/risk ratio for Kelly to remain useful.

Step 3: Estimate Reward/Risk Ratio

Divide average profit on winners by average loss on losers to get b.

Greater than 1 means "wins exceed losses on average" — the basis for long-term profitability.

Step 4: Plug In to Get the Theoretical Ceiling

Insert your p and b into Kelly to get the suggested allocation.

Note: The percentage Kelly produces is the maximum tolerable principal loss per trade. Kelly ≠ a recommendation to actually bet that much.

Step 5: Reverse-Engineer Lot Size from Stop Distance

This is the most important practical step. If Kelly says 10% on a $10,000 account, this trade can lose at most $1,000.

Operational logic: Set your chart stop, divide $1,000 by the stop distance in pips to get value-per-pip, then back-calculate the lot size.

Example: Long EUR/USD at 1.1000, stop at 1.0900 (100-pip distance).

Per-pip value: $1,000 ÷ 100 pips = $10/pip.

Lot size: a standard FX contract is roughly $10/pip per standard lot, so the answer is 1 standard lot.

Implementation Note: Platform Position Sizing

Once you understand Kelly, the practical work is converting "theoretical ratio" into actual orders.

In practice, traders combine the platform's quote and spread with the stop distance to back into lot size. On Titan FX's MT4 / MT5, you fix the stop first, then compute the lot count from your account balance and acceptable risk.

This flow turns the math model into an executable decision instead of a theoretical wish.

4. Strengths and Limitations

Mathematically perfect, but real markets test it.

Strengths

Strength 1: Auto-rejects Negative-Edge Trades

If your expected value is negative (poor reward/risk or low win rate), Kelly returns zero or negative — telling you not to commit a single dollar.

Strength 2: Discipline by Default

A clean numerical anchor protects you from over-confidence after a winning streak and panic during a losing streak.

Limitations

Limitation 1: Hyper-sensitive to Win-Rate Estimation

Beginners typically overestimate their win rate. A few percentage points of estimation error swings the recommended position size dramatically and creates over-exposure.

Limitation 2: Severe Drawdowns

Kelly chases the terminal growth maximum — and the path to it can include drawdowns of 50%+, which is psychologically destructive for most retail traders.

5. Risk Variants: Balancing Growth and Stability

Full Kelly is rarely tolerable in practice. A 25% Kelly bet means four consecutive losses devastate the account. Professionals deflate it.

Variant 1: Half Kelly and Fractional Kelly

The dominant pro practice: cut Kelly's recommendation to half (or a quarter). If Kelly says 20%, you actually bet 10% or 5%.

Growth slows, but drawdown shrinks by roughly 50%, producing a smoother equity curve.

Variant 2: Kelly Combined with the 2% Rule

Kelly is offensive (maximize growth); fixed-fraction risk control (e.g., the 2% rule) is defensive (preserve capital).

- Combination logic: Treat Kelly's number as the ceiling, but never let any single trade lose more than 2–5% of equity in absolute terms.

Why Beginners Should Avoid Full Kelly

Kelly is acutely sensitive to data quality. Beginners ride survivorship bias and overestimate win rate. Half-Kelly or smaller fractions are essentially insurance against estimation error and against Black Swan events.

Frequently Asked Questions (FAQ)

Q1: Can the Kelly Criterion be directly applied to forex trading?

Theoretically yes, but since win rates and profit/loss ratios are unstable in forex, practitioners use Half-Kelly (50%) or Quarter-Kelly (25%) rather than the full Kelly fraction.

Q2: What if the Kelly Criterion calculation returns a negative value?

A negative Kelly value means the strategy has a negative expected value. You should either skip the trade or revise the strategy entirely.

Q3: How does the Kelly Criterion relate to risk management?

Kelly gives the theoretically optimal bet size, but in practice, traders use a fraction of Kelly (typically 25-50%) to reduce drawdown risk from losing streaks.

6. Conclusion: The Real Value of Kelly

The Kelly Criterion's value is converting uncertainty into a quantifiable risk envelope, giving every trade a clear capital basis.

In practice, choose an allocation that fits your risk tolerance rather than chasing the theoretical maximum. Half-Kelly or a more conservative fraction lets you control drawdown while maintaining steady growth.

If you can manage position size by probability and data over the long run, market volatility stops being just a threat — it gradually becomes the foundation of compounding edge.

Further Reading

- What Is Compound Interest?

- What Is a Lot?

- What Is Spread?

- What Is Leverage?

- The 2% Risk Rule

- What Is a Black Swan Event?

Titan FX Trading Strategy Lab. We produce investor-education content covering forex, commodities (crude oil, precious metals, agricultural goods), stock indices, U.S. equities, and digital assets.

Primary Sources (by category)

- Theoretical foundation: Kelly, J. L. (1956) "A New Interpretation of Information Rate", Bell System Technical Journal, Vol. 35, pp. 917–926 (the original Kelly Criterion paper)

- Mathematical derivation and proofs: Thorp, E. O. (1969) "Optimal Gambling Systems for Favorable Games", Review of the International Statistical Institute; Thorp, E. O. (2006) The Kelly Criterion in Blackjack, Sports Betting, and the Stock Market

- Practical applications: Poundstone, W. (2005) Fortune's Formula: The Untold Story of the Scientific Betting System That Beat the Casinos and Wall Street

- Drawdown and fractional Kelly empirics: MacLean, L. C., Thorp, E. O., & Ziemba, W. T. (2010) The Kelly Capital Growth Investment Criterion: Theory and Practice