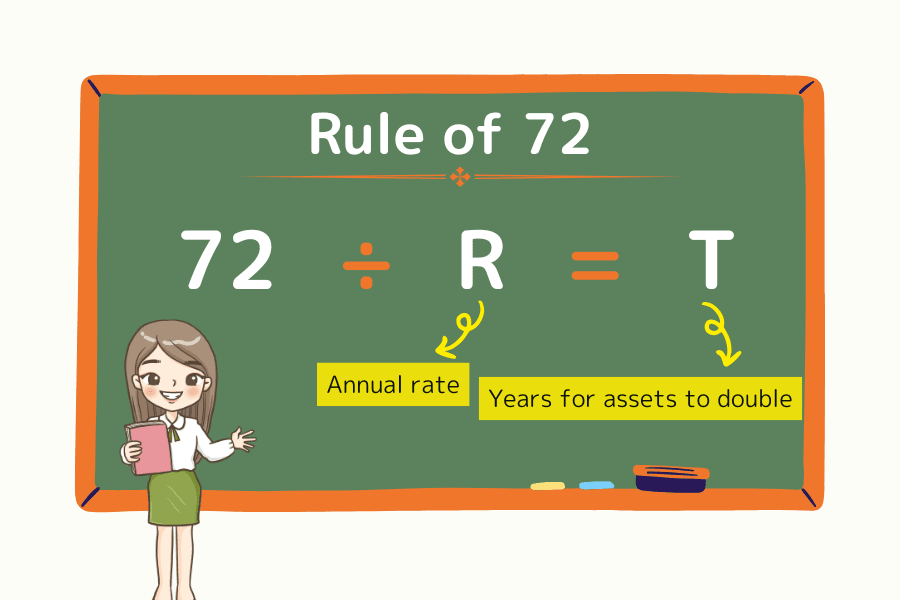

What Is the Rule of 72?

The "Rule of 72" is a quick mental-math shortcut: divide 72 by the annual interest rate (%) to estimate roughly how many years it takes for an investment to double under compound interest.

The real appeal of the Rule of 72 is that it needs no calculator and no finance background — it gives you an instant feel for the power of compounding. Swap the interest rate for an inflation rate, and the same trick estimates how long until your purchasing power is cut in half.

This article walks through the rule's mathematical derivation, its modern-market applications, the broader family of derivative rules (Rule 70 / 69.3 / 114 / 144 / 190 / 126), and the practical caveats every investor should know.

- The formula: 72 ÷ Annual rate (%) ≈ years to double / 72 ÷ Inflation rate (%) ≈ years for purchasing power to halve

- The math: Derived from ln(2) ≈ 0.6931. The number 72 was chosen because it has many divisors (1, 2, 3, 4, 6, 8, 9, 12), making mental arithmetic painless

- Best accuracy zone: 6%–10% annualized rates. For continuous compounding, switch to the Rule of 69.3

- The rule family: Rule 70 (simple inflation) / 114 (3×) / 144 (4×) / 190 (8×) / 126 (systematic / DCA investing) / 240 (monthly rates)

- Beyond investing: Also models inflation, credit-card debt doubling, and retirement-account growth — and is not to be confused with IRS Rule 72(t)

1. What Is the Rule of 72?

The Rule of 72 is a compound-interest shortcut. Divide 72 by the annualized return (%) or inflation rate (%) to estimate the number of years required for an asset to double — or for purchasing power to halve. The formulas are:

72 ÷ Annual Return (%) = Years for assets to double

72 ÷ Inflation Rate (%) = Years for purchasing power to halve

For example, an investment compounding at 8% annually doubles in roughly 72 ÷ 8 = 9 years.

If inflation runs at 3%, then 72 ÷ 3 = 24 years until purchasing power halves.

The rule's accuracy depends on rate stability. It is best suited to early-stage planning and quick comparisons rather than precise modeling.

The Math: Why 72?

The Rule of 72 is derived as an approximation to the compound formula A = P × (1 + r)^t. When the asset doubles, A = 2P, so:

- 2 = (1 + r)^t

- Take the natural log: ln(2) = t × ln(1 + r)

- Solve for t: t = ln(2) / ln(1 + r)

- Apply the small-r approximation ln(1 + r) ≈ r: t ≈ ln(2) / r ≈ 0.6931 / r

- Convert r to a percentage (R% = r × 100): t ≈ 69.31 / R

The mathematically exact value is therefore the Rule of 69.3. Why does 72 dominate in practice? Two reasons:

- Divisibility: 72 is divisible by 1, 2, 3, 4, 6, 8, 9, and 12 — most of the rates investors actually use. Mental arithmetic is trivial.

- Sweet-spot accuracy: The error is smallest in the 6%–10% range, which happens to span the long-run averages of equities and balanced portfolios.

That combination — "accurate enough" plus "easy to compute" — is why 72 became the standard in financial education and investor communication.

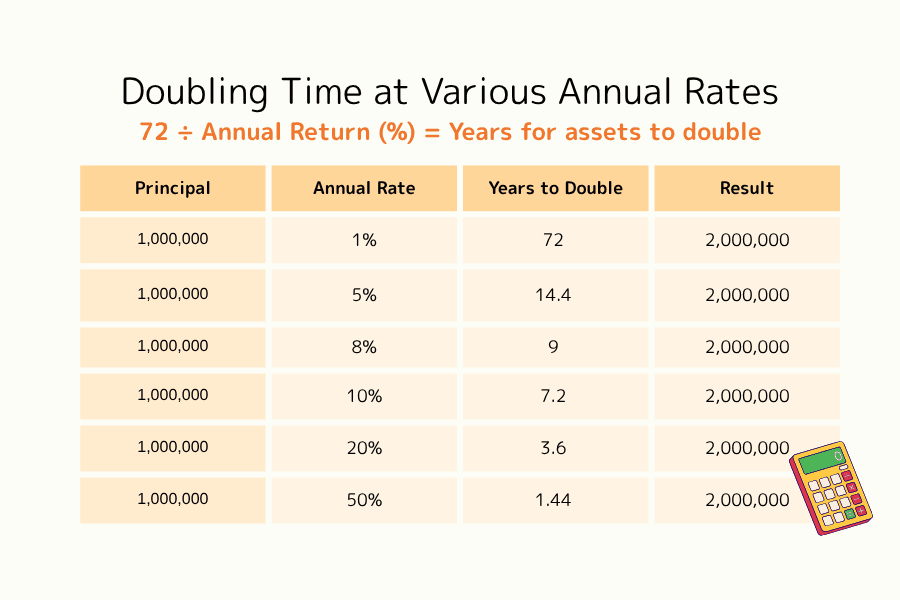

Doubling Time at Various Annual Rates

| Principal | Annual Rate (%) | Years to Double | Result |

|---|---|---|---|

| 1,000,000 | 1 | 72 | 2,000,000 |

| 1,000,000 | 2 | 36 | 2,000,000 |

| 1,000,000 | 3 | 24 | 2,000,000 |

| 1,000,000 | 4 | 18 | 2,000,000 |

| 1,000,000 | 5 | 14.4 | 2,000,000 |

| 1,000,000 | 6 | 12 | 2,000,000 |

| 1,000,000 | 8 | 9 | 2,000,000 |

| 1,000,000 | 10 | 7.2 | 2,000,000 |

| 1,000,000 | 12 | 6 | 2,000,000 |

| 1,000,000 | 15 | 4.8 | 2,000,000 |

| 1,000,000 | 20 | 3.6 | 2,000,000 |

| 1,000,000 | 30 | 2.4 | 2,000,000 |

| 1,000,000 | 50 | 1.44 | 2,000,000 |

| 1,000,000 | 100 | 0.72 | 2,000,000 |

Two Takeaways

- Small differences in return produce large differences in doubling time. The gap between 5% and 8% is more than five years.

- Compounding rewards time. Starting earlier — even at a moderate rate — beats starting later at a high rate.

2. Applications and Economic Interpretation

Application 1: Estimating Doubling Time

For an asset compounding at the historical equity average of 7%: 72 ÷ 7 ≈ 10.3 years

Lift the rate to 12% and the doubling time collapses to: 72 ÷ 12 = 6 years

Even small lifts in return materially accelerate wealth growth.

Application 2: Reverse-Engineering the Required Return

To take 1,000,000 to 2,000,000 in 5 years, the required annual return is: 72 ÷ 5 = 14.4%

Returns of that magnitude typically appear in growth equities, emerging-market assets, index instruments such as the S&P 500 and NASDAQ 100, or leveraged products such as forex margin trading and CFDs — but always paired with materially higher risk. Match the strategy to your risk tolerance.

Application 3: Inflation and the Erosion of Purchasing Power

The Rule of 72 also models how inflation erodes purchasing power. At 3% annual inflation: 72 ÷ 3 = 24 years

Today's 100 will buy roughly 50 worth of goods in 24 years.

At 6% inflation, halving accelerates to: 72 ÷ 6 = 12 years

Pure cash holdings lose real value over long horizons; this is why diversified, inflation-aware portfolio construction matters.

3. The Rule in the Modern Financial Environment

Long-run statistics put equity-market real returns in the 7%–10% range and fixed-income real returns at roughly 2%–4%. Today's environment — characterized by central-bank policy normalization following extended low-rate regimes and persistent inflation — keeps the real yield on traditional savings products near zero or negative.

Through the Rule of 72:

- At a 1% rate, doubling takes 72 years.

- At 2%, it still takes 36 years.

These speeds cannot keep pace with cumulative inflation. Saving alone rarely produces real wealth growth in this environment, which is why diversified portfolios across equities, fixed income, commodities, and alternatives have become the default playbook.

Higher Returns Come With Higher Risk

Aiming for 15%–20% returns (growth equities, technology, real estate, CFDs) compresses doubling time dramatically:

- 15% return: 72 ÷ 15 ≈ 4.8 years

- 20% return: 72 ÷ 20 ≈ 3.6 years

But these returns ride on volatility and the business cycle. Calibrating with hedging strategies and proper position sizing turns aggressive returns into an asset rather than a trap.

Inflation Erosion in the Recent Cycle

Recent inflation cycles offer real-world Rule of 72 case studies:

- Annual inflation 3% (long-term average) → purchasing power halves in 24 years

- Annual inflation 6% (moderate inflation) → halves in 12 years

- Annual inflation 8% (severe inflation episodes) → halves in 9 years

A household spending 100,000 per year that takes no defensive action would need 200,000 to maintain the same lifestyle nine years into an 8% inflation regime.

The Reverse Application: Debt at High Interest Rates

The Rule of 72 also captures debt accumulation, especially at consumer credit rates:

| Debt Type | Annual Rate (APR) | Doubling Time |

|---|---|---|

| Credit-card revolving balance | 18% | ~ 4 years |

| Cash advance / payday loan | 24% | ~ 3 years |

| Mortgage | 5% | ~ 14.4 years |

| Consumer loan | 12% | ~ 6 years |

Implication: Earning 8% on investments while carrying 18% revolving credit-card debt means the debt grows faster than the assets. Pay down high-interest debt before scaling up investments — that order of operations is the only one consistent with the math of compounding.

4. Limitations and Practical Caveats

The Rule of 72 is a powerful planning shortcut, but it has real boundaries. Use it knowing the following:

1. Rates Are Not Constant

The rule assumes a fixed annual return or inflation rate. Reality serves up volatility, policy shifts, and full business cycles. Averages over-simplify and can either flatter or punish actual outcomes.

2. Higher Return Equals Higher Risk

Higher rates compress doubling time, but the assets that deliver them — high-volatility equities, leveraged products — bring matching downside. Calibrate to your risk tolerance and financial goals; do not treat headline return as a sufficient criterion.

3. Costs and Taxes Matter

The Rule of 72 takes a gross return as input. Taxes, transaction costs, and management fees compress real growth and stretch doubling time. Plan against your net return (return minus all costs) for a more realistic picture.

4. Accuracy Falls Off at the Extremes and Under Continuous Compounding

When annual rates exceed 20% or fall below 2%, the rule's error grows visibly. For continuous compounding (used in some financial-engineering models), substitute the Rule of 69.3 (ln(2) × 100 = 69.3) for tighter precision.

5. Do Not Confuse "Rule 72" With IRS Rule 72(t)

A common point of confusion in U.S. retirement-planning content: IRS Rule 72(t) — which governs early withdrawals from retirement accounts — has nothing to do with the Rule of 72. They share a number; that's the entire connection.

5. The Family of Derivative Rules

The Rule of 72 is one member of a family rooted in the constant ln(2) ≈ 0.6931. Below is a unified view of the most useful relatives:

| Rule | Use Case | Formula | Best For |

|---|---|---|---|

| Rule 69.3 | Doubling under continuous compounding | 69.3 ÷ R | Financial engineering, derivatives pricing |

| Rule 70 | Simple-interest or inflation halving | 70 ÷ Inflation rate | Central-bank inflation estimation |

| Rule 72 | General compound doubling | 72 ÷ R | Equities, bonds, balanced portfolios |

| Rule 114 | Time to 3× | 114 ÷ R | Long-horizon retirement targets |

| Rule 144 | Time to 4× | 144 ÷ R | Multi-generational wealth planning |

| Rule 190 | Time to 8× | 190 ÷ R | Visualizing very long-run compounding |

| Rule 126 | Systematic-investment doubling | 126 ÷ R | Salary-deduction, retirement-account contributions |

| Rule 240 | Doubling at monthly rates | 240 ÷ Monthly rate | Monthly-compounding products |

Choosing the Right Rule

- Lump-sum investing: Rule 72

- Systematic / dollar-cost-averaging investing: Rule 126 (derived in research by Professor Norio Hibiki of Keio University; captures the dynamics of periodic contributions where later capital has less compounding time)

- Continuous compounding / financial engineering: Rule 69.3

- Inflation estimation: Rule 70 (simplicity) or Rule 72 (precision)

- 3× / 4× / 8× targets: Rule 114 / 144 / 190

6. Frequently Asked Questions

Q1:Beyond the Rule of 72, what other estimation rules are useful?

Beyond the Rule of 72, several adjacent shortcuts help model asset growth and inflation:

- Rule of 70: Similar to the Rule of 72, mainly used for purchasing-power-halving estimates. Simpler but slightly less accurate

- Rule of 69.3: A more precise variant derived from ln(2) ≈ 0.693, used in financial engineering

- Rule of 114 / 144 / 190: Time to grow assets by 3× / 4× / 8× (114 ÷ R, 144 ÷ R, 190 ÷ R)

- Rule of 126: Doubling estimate for dollar-cost-averaging (systematic) investing, derived in research by Professor Norio Hibiki of Keio University

- Rule of 240: For monthly compounding — 240 ÷ monthly rate ≈ months to double

These rules are not as exact as full compound-interest calculations but offer real value for early-stage planning and education.

Q2:Can I use the Rule of 72 every day?

The Rule of 72 is built around annualized returns and asset doubling, so it is designed for long-term investment planning — questions like "how much do I need to compound at to double my portfolio in N years?"

For short-term trading (intraday, weekly), returns vary too quickly for the rule to be a meaningful prediction tool.

It is, however, useful for setting annual targets — for example, doubling capital in 3 years implies an annual return of roughly 24%.

In short: the Rule of 72 is not an instrument for short-term trading, but it is excellent for long-term goal setting.

Q3:Why 72, and not 69 or 70?

Theoretically, the exact value is ln(2) × 100 ≈ 69.31. In practice, 72 wins for two reasons:

- Divisibility: 72 is divisible by 1, 2, 3, 4, 6, 8, 9, and 12, making mental and verbal arithmetic trivial

- Sweet-spot accuracy: In the 6%–10% range, the approximation error is smallest — and that band happens to cover the long-run average return of most diversified equity-bond portfolios

The Rule of 72 strikes the optimal balance between precision and computability, which is why it became the standard in financial education.

Q4:What is the difference between the Rule of 72 and the Rule of 70?

Both share the same structure (divide a constant by the rate to get doubling/halving time), but their use cases differ:

- Rule of 72: General compound investing (equities, bonds, ETFs), best accuracy at 6%–10%

- Rule of 70: Inflation estimation, population-growth modeling, purchasing-power halving — mathematically tighter approximation but less practical for investing applications than 72

In practice, investing literature uses 72 while economics — especially central-bank inflation estimation — uses 70. The error gap is small; choose based on convention.

Q5:Which rule should I use for continuous compounding?

When compounding frequency approaches infinity (continuous compounding), use the Rule of 69.3 (ln(2) × 100 = 69.3).

Example: 8% under continuous compounding:

- Rule of 72: 72 ÷ 8 = 9 years

- Rule of 69.3: 69.3 ÷ 8 ≈ 8.66 years

A difference of about 0.34 years (4 months). For applications requiring high precision — financial engineering, derivatives pricing, actuarial work — Rule 69.3 has materially smaller error. For day-to-day investing decisions, the Rule of 72 is precise enough.

Q6:Does the Rule of 72 apply to dollar-cost-averaging (DCA) investing?

The compound dynamics of systematic, periodic investing differ from a lump sum, so we recommend switching to Rule of 126:

126 ÷ Annual return (%) ≈ years to double the principal under systematic investing

Example: monthly DCA into an index ETF averaging 6% annually:

- Lump-sum: 72 ÷ 6 = 12 years to double

- DCA: 126 ÷ 6 = 21 years to double

The gap arises because capital contributed late has less time to compound. Rule 126 — derived in research by Professor Norio Hibiki of Keio University — better captures the dynamics of payroll deductions, retirement-account contributions, and other systematic-investment use cases.

Q7:How should I account for taxes and fees?

The Rule of 72 works on a gross return. The actual doubling time should be calculated on a net return — gross minus all taxes, transaction costs, and management fees.

Example:

- Nominal annual return: 8%

- Total costs (tax + fees + management): 1.5%

- Net return: 6.5%

- Actual doubling time: 72 ÷ 6.5 ≈ 11.1 years (not 9)

Always plan against net return. Low-cost index ETFs are popular among long-term investors precisely because their total expense ratio (TER) is small, keeping the gap between nominal and net return narrow and aligning real outcomes more closely with the Rule-of-72 theoretical value.

7. Conclusion: The Wisdom of Compounding and Time

The Rule of 72 is simple, but it captures something fundamental: time and rate of return are the dominant levers in wealth formation. With the rule and its derivative family — Rule 70, 69.3, 114, 144, 190, 126 — you can frame the questions that matter: how long to double, what return to target, and how to defend purchasing power against inflation.

Wealth is rarely built overnight; it is the product of starting early and compounding consistently. Choose the right vehicles, set clear goals, and continuously rebalance the trade-off between return and risk. That discipline is what allows compounding to do its work.

For deeper application, explore the specific instruments and education topics linked above, or consult a qualified financial professional to translate the math into a plan suited to your circumstances.

Further Reading

- What is Forex Margin Trading?

- What is Leverage?

- What is a CFD?

- What is Inflation?

- What is a Stock Market Index?

- What is the FOMC?

Titan FX's financial market research and analysis team produces investor education content across a wide range of financial instruments, including foreign exchange (FX), commodities (crude oil, precious metals, and agricultural products), stock indices, U.S. equities, and crypto assets.

Primary Sources (by Category)

- Mathematical foundations of compound interest and the Rule of 72: Pacioli, L. (1494) Summa de arithmetica, geometria, proportioni et proportionalità; the natural-log constant ln(2) ≈ 0.6931

- Academic origins of derivative rules: Eckart-Young correction (mathematical derivation of Rule 69.3 / 70); Professor Norio Hibiki, Keio University (Rule 126, research on systematic-investment compounding)

- Inflation and purchasing-power data: U.S. Bureau of Labor Statistics (CPI historical data); Federal Reserve Economic Data (FRED)