Home

Home- Investment Guide: Strategies for Stocks, Forex, and Metals

- FOMC 2026: Schedule, Rates and Warsh Outlook

FOMC 2026 Guide: Schedule, Rate Decisions and Warsh Confirmation Outlook

The FOMC (Federal Open Market Committee) is the Federal Reserve's policy-setting body that meets eight times a year to decide US interest rates and balance-sheet policy, moving global stock, currency, and bond markets.

Beyond raising or lowering interest rates, the FOMC's March, June, September, and December meetings publish the SEP (Summary of Economic Projections) and dot plot — key references for reading where policy is headed. This article provides a comprehensive overview of the 2026 FOMC meeting schedule, the rate-decision trajectory since Q4 2025, the latest dot plot released in March 2026, and the end of Chair Powell's term and Kevin Warsh's nomination and confirmation outlook, helping investors keep up with global financial markets.

Status as of April 2026: The federal funds target range is 3.50%–3.75%, held steady for two consecutive meetings (Jan 2026 and Mar 2026). Kevin Warsh has been nominated as the next Fed chair. After the DOJ closed its Powell investigation and Senator Thom Tillis withdrew his block, the confirmation path has become much clearer, though formal appointment still requires Senate confirmation.

- What the FOMC does and how it fits inside the Federal Reserve

- The 2026 FOMC meeting schedule and SEP months

- The rate path since September 2025

- How to read the March 2026 SEP and dot plot

- What Kevin Warsh's nomination and confirmation outlook mean for policy communication

- 1: What is the FOMC?

- 2: 2026 FOMC Meeting Schedule

- 3: Policy Trajectory from Q4 2025 to Present

- 4: Latest Dot Plot and Rate Outlook (March 2026 SEP)

- 5: Powell's Term Ending and Warsh's Confirmation Outlook

- 6: Other Major Central Banks' Policy Meeting Schedule (2026)

- 7: 5 Key Things to Watch at FOMC Meetings

- 8: 3 Key Economic Indicators FOMC Watches

- 9: FOMC Information-Gathering Tips

- 10: FOMC FAQ

- 11: Conclusion

1: What is the FOMC?

FOMC stands for Federal Open Market Committee, the core decision-making body within the U.S. Federal Reserve System (FED), responsible for formulating and adjusting U.S. monetary policy.

Its importance lies in the fact that changes in U.S. monetary policy directly affect the U.S. dollar, global stock markets, the foreign exchange market, and commodity prices.

The FOMC typically holds meetings every 6 weeks, totaling about 8 times per year, with additional emergency meetings convened when necessary.

Among these, the March, June, September, and December meetings simultaneously release the Summary of Economic Projections (SEP), covering forecasts for interest rates, GDP, unemployment, and inflation over the next three years, and therefore receive the most attention.

We will introduce the following in detail:

- Topics discussed at FOMC meetings

- FOMC member composition

- FOMC policy stances

- Relationship between FOMC and FED

Topics Discussed at FOMC Meetings

The FOMC's main responsibility is to adjust monetary policy tools, particularly Open Market Operations (OMO), which include three main directions:

Topic 1: FFR (Federal Funds Rate)

The short-term interest rate for interbank reserve lending, which is the FOMC's primary policy tool.

The FOMC sets the FFR target range and influences short-term rates through Treasury bond trading, thereby guiding market funding costs.

Topic 2: QE (Quantitative Easing)

Quantitative Easing refers to the FED's policy under economic downturns or deflation pressure, where it purchases long-term Treasury bonds and Mortgage-Backed Securities (MBS) to increase money supply, lower long-term rates, and stimulate investment and consumption.

Topic 3: QT (Quantitative Tightening)

The opposite of QE, QT involves shrinking the balance sheet (no longer purchasing or actively selling Treasury bonds and assets), withdrawing market liquidity to suppress inflation and prevent economic overheating.

Note: The FOMC decided at its October 2025 meeting to end QT effective December 1, 2025, ceasing balance sheet runoff and concluding the tightening cycle that had been ongoing since 2022.

FOMC Member Composition

The voting members of the FOMC consist of:

- 7 Federal Reserve Board (FRB) Governors: Including 1 Chair and 2 Vice Chairs, all with voting rights (Governor terms are 14 years; Chair and Vice Chair terms are 4 years).

- 12 Regional Federal Reserve Bank Presidents: Among them, the New York Fed President holds permanent voting rights, while 4 other presidents rotate (annually).

- Other non-voting presidents still attend and participate in discussions.

Therefore, each meeting has 12 voting members, and the policy direction is determined by simple majority vote.

FOMC Policy Stance

The attitudes of FOMC members influence market interpretation:

- "Hawks": Lean toward rate hikes and tightening to suppress inflation.

- "Doves": Lean toward rate cuts or maintaining accommodation to stimulate the economy.

This "Hawks vs. Doves" divide is often a core driver of financial market volatility.

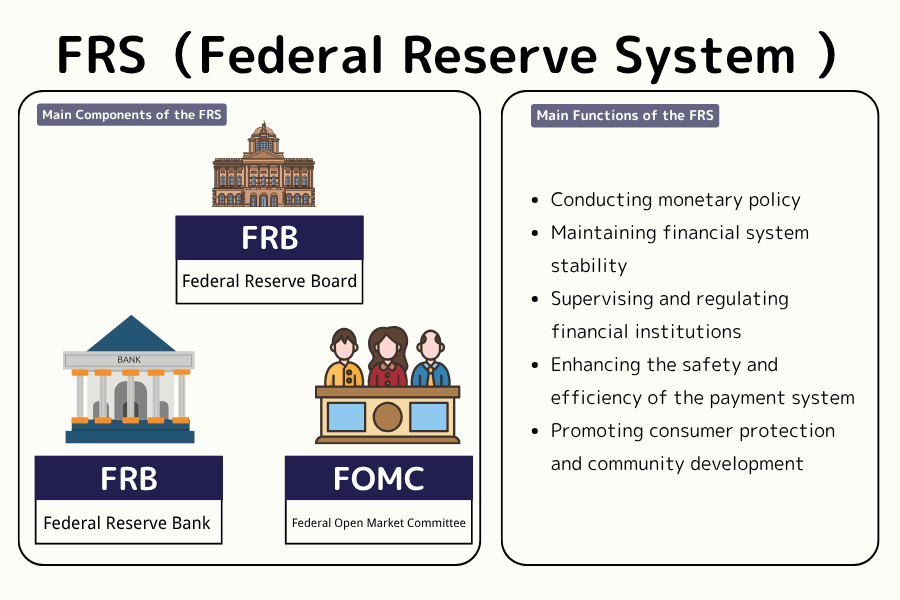

Relationship Between FOMC and FED

In the U.S. financial system, FED, FRB, and FOMC are closely related but have distinct functions, often confused by investors.

- Federal Reserve System (FED): The U.S. central banking system, composed of the Board of Governors, 12 regional Federal Reserve Banks, and member commercial banks.

- Federal Reserve Board (FRB): The highest decision-making body of the FED, responsible for formulating national monetary policy and supervising the 12 regional Reserve Banks.

- Federal Open Market Committee (FOMC): Composed of FRB Governors and select regional Reserve Bank Presidents, specifically responsible for deciding rate policy and open market operations.

In short: FED is the overall system, FRB is the policy-formulation core, and FOMC is the body that specifically decides rates and money supply.

Further reading: Relationship between Fed, FRB, and FOMC

2: 2026 FOMC Meeting Schedule

Meeting Dates and Outcomes (Per Official Press Releases)

Latest Update: At the March 17–18, 2026 meeting, the FOMC held the rate steady at 3.50%–3.75% for the second consecutive meeting, with only Stephen Miran dissenting (preferring a 25bp cut). The accompanying March SEP showed the 2026 median forecast of one more 25bp cut to 3.25%–3.50%, with the longer-run rate revised up to 3.1%. See §4 Latest Dot Plot for details.

The 2026 FOMC meets a total of 8 times, with the March, June, September, and December meetings publishing both the SEP and the dot plot. Bold text in the table indicates SEP-release meetings.

| Meeting Date (ET) | Decision | Target Range (Federal Funds Rate) | SEP Release | Key Notes |

|---|---|---|---|---|

| Jan 27–28, 2026 | Hold | 3.50%–3.75% | No | Ended the 2025 Q4 three-cut cycle. Miran and Waller preferred a 25bp cut. |

| Mar 17–18, 2026 | Hold | 3.50%–3.75% | Yes | Released the March 2026 SEP. The 2026 median forecast was for one more 25bp cut. The longer-run rate was revised up to 3.1%. Only Miran dissented. |

| Apr 28–29, 2026 | Scheduled | — | No | This week. Markets watching for any 2026 cut signals. |

| Jun 16–17, 2026 | Scheduled | — | Yes | Second SEP release. Inflation and employment forecasts to be reviewed. |

| Jul 28–29, 2026 | Scheduled | — | No | Wait-and-see period. |

| Sep 15–16, 2026 | Scheduled | — | Yes | Third SEP release. |

| Oct 27–28, 2026 | Scheduled | — | No | — |

| Dec 8–9, 2026 | Scheduled | — | Yes | Year-end SEP and 2027 outlook to be released. |

Note: SEP = Summary of Economic Projections (including the dot plot), released at the March, June, September, and December meetings.

U.S. FOMC Decision and Press Conference Times (Asia Time)

The U.S. uses Daylight Saving Time (DST), so FOMC announcement times differ between summer and winter.

Times for Asian regions including Tokyo / Beijing / Taipei / Hong Kong / Kuala Lumpur:

| Month | Policy Decision Time | Press Conference Time |

|---|---|---|

| Jan, Dec (Standard Time) | 03:00 (Asia) | 03:30 (Asia) |

| Mar, May, Jun, Jul, Sep, Oct (DST) | 02:00 (Asia) | 02:30 (Asia) |

3: Policy Trajectory from Q4 2025 to Present

From the September 2025 rate cut that started the easing cycle, to April 2026 with two consecutive holds, the FOMC has shifted from "preventive cutting" to "wait-and-see mode" in just six months. Below is the complete chronology:

September 2025: Easing Cycle Begins

On September 17, 2025, the FOMC cut the federal funds rate by 25bp from 4.25%–4.50% to 4.00%–4.25%, citing "slowing economic growth and cooling employment momentum" as a preventive adjustment. The vote was 11–1.

October 2025: Another 25bp Cut, QT Ended

On October 29, 2025, the FOMC cut another 25bp to 3.75%–4.00%, and decided to end Quantitative Tightening (QT) effective December 1. The vote was 10–2, reflecting widening internal divisions—Stephen Miran preferred a single 50bp cut, while Jeffrey Schmid preferred no change.

December 2025: A "Divided" Year-End Cut

On December 10, 2025, the FOMC cut a third time by 25bp to 3.50%–3.75%, but 3 members dissented—the most divided decision since September 2019. The accompanying December SEP showed the 2026 median projection was for only one more 25bp cut to 3.4%, with 7 members projecting no cuts in 2026 at all. Market expectations for 2026 easing pace cooled significantly. The committee also revised the 2026 GDP growth forecast up to 2.3% (+50bp from the September forecast).

January 2026: Brakes Applied, Wait-and-See Begins

On January 28, 2026, the FOMC held at 3.50%–3.75%, formally ending the three-consecutive-cut cycle. The statement emphasized that "economic activity has been expanding at a solid pace," "job gains have been low but the unemployment rate has shown signs of stabilization," and "inflation remains somewhat elevated." Miran and Waller continued to favor another 25bp cut, but markets expected the next adjustment no earlier than June.

March 2026: Hold Again, Latest SEP Released

On March 18, 2026, the FOMC held for the second consecutive meeting at 3.50%–3.75%, with only Miran dissenting, reflecting the prevailing wait-and-see sentiment. The accompanying March SEP showed the longer-run rate revised up from 3.0% to 3.1%, and PCE inflation 2026 year-end forecast revised up to 2.7% (+30bp from the December forecast), reflecting the Fed's recognition that "inflation stickiness" may be higher than previously expected. See §4 Latest Dot Plot below for details.

Summary: After three consecutive 25bp cuts in Q4 2025 (cumulative -75bp), the FOMC has paused for two consecutive meetings since 2026 began. Market focus has shifted to "when and which direction the next adjustment will be," "the policy framework Warsh may pursue if confirmed," and "whether inflation stickiness will force the Fed to hold rates higher for longer."

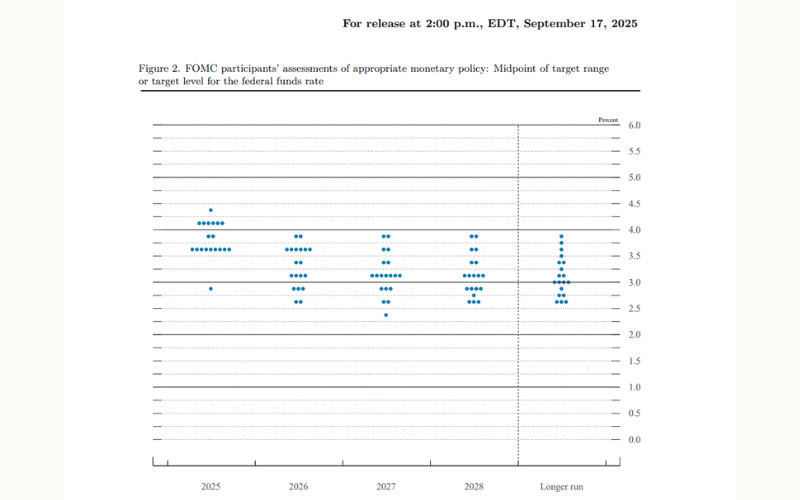

4: Latest Dot Plot and Rate Outlook (March 2026 SEP)

※ Sources: Federal Reserve - SEP March 2026, CME FedWatch

The latest dot plot and SEP released at the March 18, 2026 FOMC meeting:

Rate Path (Median Projection)

| Time Point | Median Projection | Implied Adjustment |

|---|---|---|

| End of 2026 | 3.4% | One 25bp cut from the current 3.50%–3.75% to 3.25%–3.50% |

| End of 2027 | 3.1% | Another 25bp cut to 3.00%–3.25% |

| End of 2028 | ~3.1% | Roughly flat |

| Longer-run | 3.1% | Up 10bps from December 2025's 3.0% |

The upward revision in the longer-run rate suggests the Fed believes the neutral rate has structurally shifted higher in the post-pandemic era.

Distribution of 2026 Rate Cut Expectations Among Members

| Expected Cuts | Members |

|---|---|

| 0 (no cuts) | 7 |

| 1 (25bps) | 7 |

| 2 (50bps) | 2 |

| 3 (75bps) | 2 |

| 4 (100bps) | 1 |

14 of the 19 members project either 0 or 1 cut in 2026, reflecting the FOMC's increasingly cautious stance on the easing pace.

Inflation and Economic Projections (vs. December 2025 SEP)

| Indicator | End of 2026 | End of 2027 | Change from Dec 2025 SEP |

|---|---|---|---|

| PCE Inflation | 2.7% | 2.2% | 2026 +30bps |

| GDP Growth | 2.3% | — | 2026 +50bps (from December) |

The PCE inflation forecast indicates the Fed expects inflation to return to the 2% target only by 2028, a key reason for maintaining higher rates.

The latest dot plot is available on the Federal Reserve official website.

5: Powell's Term Ending and Warsh's Confirmation Outlook

Another major issue in 2026 is the FOMC nomination and transition process. Below is the chronology:

Powell's Term Expires

The current Chair, Jerome Powell, has a 4-year term that expires on May 15, 2026. Over the past six months, his exit process was clouded by a federal investigation.

Warsh Nomination and Confirmation Outlook

| Date | Key Development |

|---|---|

| Nov 2025 | The U.S. Department of Justice (DOJ) opens a criminal investigation into Powell, focused on the truthfulness of his Congressional testimony regarding Federal Reserve headquarters renovation costs |

| Jan 30, 2026 | President Trump nominates former Fed Governor Kevin Warsh as the next Chair |

| Feb–Apr 2026 | Republican Senator Thom Tillis (NC) freezes Warsh's confirmation, demanding the DOJ end the Powell investigation |

| Apr 21, 2026 | Warsh's confirmation hearing; he declares himself "strictly independent" and advocates for a Fed "policy framework regime change" |

| Apr 24, 2026 | U.S. Attorney Jeanine Pirro announces the closure of the criminal investigation into Powell (Powell was never charged) |

| Apr 26, 2026 | Tillis withdraws his opposition; Warsh's confirmation path becomes much clearer |

| May 15, 2026 | Scheduled term end: Powell's chair term ends; Warsh taking office still requires Senate confirmation |

Policy Outlook If Warsh Is Confirmed

In his confirmation hearing, Warsh clearly stated that he would:

- Maintain "strictly independent" stance, refusing to bow to White House demands for rate cuts

- Drive a Fed policy framework "regime change", potentially reducing the number of FOMC meetings per year and reviewing the inflation-targeting mechanism

- Hold a hawkish stance on inflation suppression while acknowledging the policy implications of cooling labor markets

The current market base case is: Warsh maintains the existing 3.50%–3.75% range early in his tenure, with inflation and employment data potentially driving a first cut as early as June. However, if Warsh pushes through framework reforms, FOMC meeting cadence and policy communication could undergo structural change.

6: Other Major Central Banks' Policy Meeting Schedule (2026)

The U.S. FOMC's monetary policy has profound implications for global markets, and central banks worldwide also set their interest rate policies based on their own economic conditions. The 2026 policy meeting announcement times for major central banks:

Bank of Japan (BOJ)

- Announcement Time: Approximately 10:30–12:00 JST after the policy meeting concludes.

- If policy is held unchanged, the announcement is usually earlier; if there is a policy change, the announcement may be delayed.

European Central Bank (ECB)

Europe also uses Daylight Saving Time (DST), so policy decision announcement times vary.

| Month | Policy Decision Time (Asia) | Press Conference Time |

|---|---|---|

| Jan, Mar, Oct, Dec (Standard Time) | 21:15 (Asia) | 21:45 (Asia) |

| Apr, Jun, Jul, Sep (DST) | 20:15 (Asia) | 20:45 (Asia) |

Bank of England (BOE)

The UK also uses Daylight Saving Time (DST), with policy decision announcement times as follows:

| Month | Policy Decision Time (Asia) |

|---|---|

| Feb, Mar, Nov, Dec (Standard Time) | 20:00 (Asia) |

| May, Jun, Aug, Sep (DST) | 19:00 (Asia) |

Reserve Bank of Australia (RBA)

The RBA uses DST and Standard Time, with announcement times as follows:

| Month | Policy Decision Time (Asia) | Press Conference Time |

|---|---|---|

| May, Jul, Aug, Sep (Standard Time) | 12:30 (Asia) | 13:30 (Asia) |

| Feb, Mar, Nov, Dec (DST) | 11:30 (Asia) | 12:30 (Asia) |

Note: Since 2024, the RBA has reduced its meeting frequency from 11 to 8 per year, holding one meeting approximately every 6 weeks.

Bank of Canada (BOC)

Canada also uses Daylight Saving Time (DST), with announcement times as follows:

| Month | Policy Decision Time (Asia) |

|---|---|

| Jan, Mar, Oct, Dec (Standard Time) | 22:00–23:00 (Asia) |

| Apr, Jun, Jul, Sep (DST) | 21:45 (Asia) |

Swiss National Bank (SNB)

The SNB's policy decision announcement times:

| Month | Policy Decision Time (Asia) |

|---|---|

| Mar, Dec (Standard Time) | 16:30 (Asia) |

| Jun, Sep (DST) | 15:30 (Asia) |

When decisions deviate significantly from market expectations, this not only has a major impact on foreign exchange rates, but also affects equity markets, commodity markets, and other global markets.

Checking the deviation between market forecasts and actual results is important. Titan FX provides an Economic Calendar where you can review the importance of economic indicators along with prior forecast and result data.

7: 5 Key Things to Watch at FOMC Meetings

The FOMC publishes various information; the following 5 items deserve particular attention:

- 【Point 1】Statement

- 【Point 2】Chair's Press Conference

- 【Point 3】Summary of Economic Projections (SEP)

- 【Point 4】Meeting Minutes

- 【Point 5】FOMC Member Communications

【Point 1】Statement

The FOMC publishes a Statement after each meeting. The Statement summarizes the assessment of the economy and prices, and the basic policy decisions including changes (or lack thereof) to monetary policy.

The Statement may hint at upcoming policy adjustments and is therefore closely watched by investors. Markets react sensitively to language changes from prior statements.

We recommend referring to the original English text for the most accurate information; if you are not comfortable with English, automatic translation services and breaking-news websites can be helpful.

【Point 2】Chair's Press Conference

30 minutes after the Statement is released, the Fed Chair holds a press conference. The Chair explains the meeting decisions, assesses the economy and prices, and then takes Q&A from the media. Press conference content can trigger major market reactions and warrants special attention.

Before 2018, press conferences were held every other meeting; since 2019, every FOMC meeting includes a press conference. Policy changes tend to occur at meetings with a press conference.

【Point 3】Summary of Economic Projections (SEP)

The FOMC releases the SEP each quarter (March, June, September, December). The projections cover the policy rate, real GDP, unemployment, PCE inflation, and core PCE inflation over the next three years. Among them, the policy rate projections (the "dot plot") receive the most attention.

The latest SEP was released on March 18, 2026. For detailed numbers and distribution, see §4 Latest Dot Plot and Rate Outlook.

If the projections differ from those three months earlier, exchange rates react sensitively. The dot plot can be confirmed on the Federal Reserve's official website.

【Point 4】Meeting Minutes

Meeting Minutes are released approximately 3 weeks after each FOMC meeting. The Minutes reveal discussions not mentioned in the Statement or press conference, potentially triggering market sensitivity.

Since markets have already obtained the main information from the Statement and press conference, the Minutes typically do not contain new material, but occasionally they become a focal point for monetary policy and can cause market volatility upon release.

【Point 5】FOMC Member Communications

FOMC members include the Chair, Vice Chairs, Governors, and regional Federal Reserve Bank Presidents, who frequently make remarks at speeches, press conferences, or symposia. Among regional Reserve Bank President remarks, those from Presidents with voting rights have greater influence.

As the year-end approaches, markets watch for the upcoming year's voting Presidents. Voting rights rotate annually (the New York Fed President holds permanent voting rights). The list of 2026 voting regional Federal Reserve Bank Presidents is available on the Federal Reserve official website for the latest announcements.

8: 3 Key Economic Indicators FOMC Watches

When deciding policy rates, the FOMC primarily references the following 3 economic indicators:

- CPI (Consumer Price Index)

- PCE Deflator

- U.S. Nonfarm Payrolls

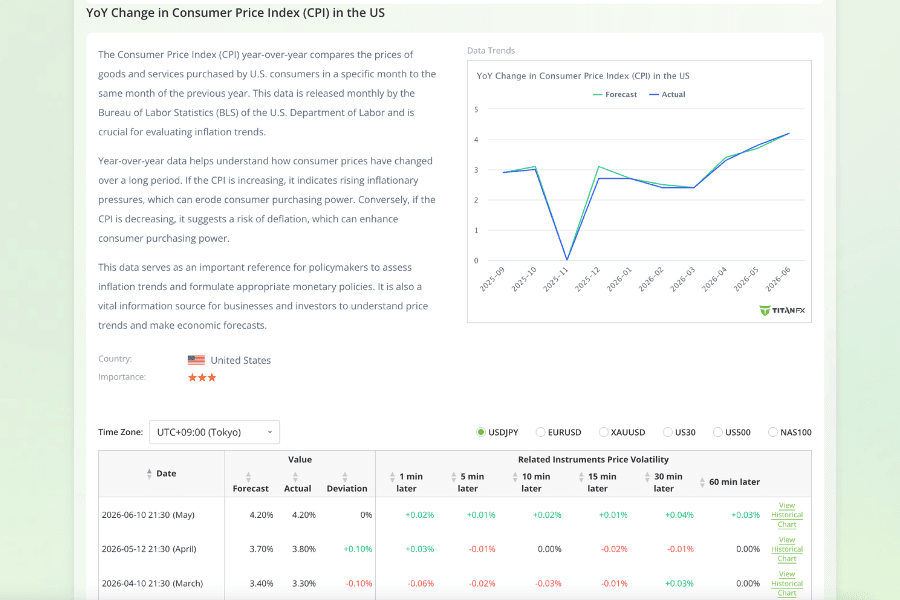

CPI (Consumer Price Index)

CPI is an economic indicator measuring price changes. If inflation persistently exceeds the target, the FOMC may adopt tightening policy (rate hikes) to suppress price increases; if below target, accommodative policy (rate cuts) is used to promote prices. Therefore, price trends are the basis for monetary policy formulation, and CPI requires close attention.

What is the Consumer Price Index (CPI)?

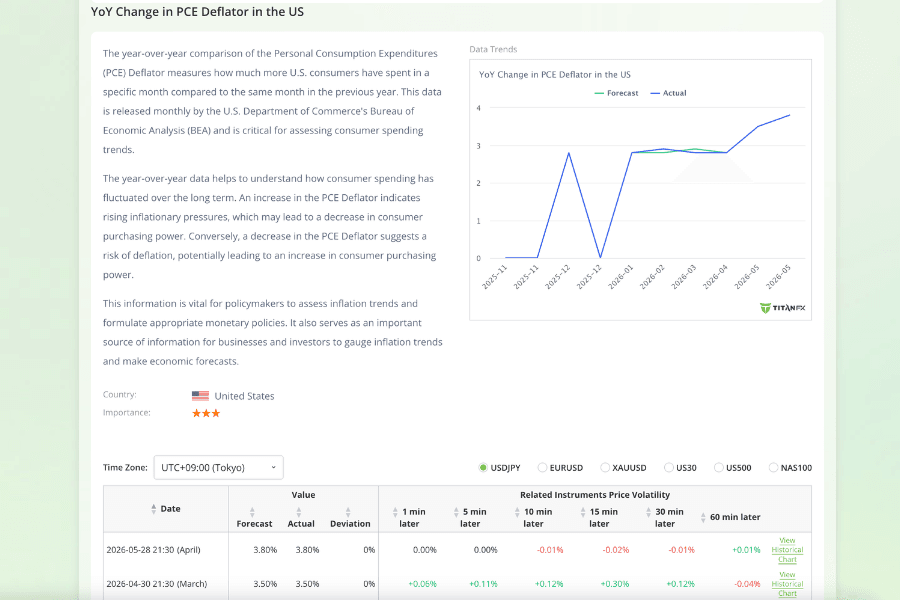

PCE Deflator

The PCE Deflator is calculated based on U.S. personal consumption and is an economic indicator capturing personal consumption price trends. Like the CPI, it can be used to track inflation or deflation. Compared to CPI, the PCE Deflator better adapts to changes in consumer preferences and behavior, and the FOMC places greater weight on this indicator when formulating monetary policy.

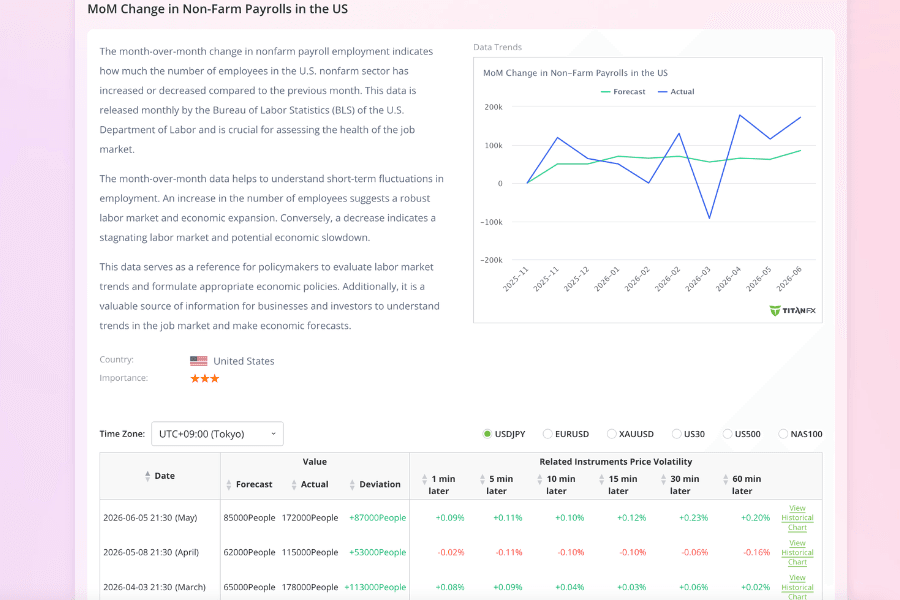

U.S. Nonfarm Payrolls

U.S. employment data surveys the labor market and is a key indicator for understanding U.S. economic trends, including nonfarm payrolls, unemployment, average hourly earnings, and labor force participation rate.

In strong economic conditions, the FOMC may adopt tightening policy (rate hikes) to suppress overheating, with rising USD rates attracting USD buying and raising the exchange rate. In weak conditions, the FOMC may adopt accommodative policy (rate cuts), with falling USD rates increasing selling pressure and lowering the exchange rate.

Therefore, understanding U.S. employment data is crucial for predicting monetary policy.

9: FOMC Information-Gathering Tips

To accurately track FOMC policy direction, investors need to combine official information and market tools to build a comprehensive information-gathering process. Here are several practical methods:

Method 1: Track Official Sources

- Federal Reserve (FED) Website: After each meeting, the Statement, Meeting Minutes, and SEP are released.

- Chair's Press Conference: Listen directly to Powell's (or other Chair's) remarks for first-hand information ahead of market interpretation. If Warsh assumes the chairmanship, his communication style and policy messaging may shift, warranting close attention.

Method 2: Use Market Tools

- CME FedWatch Tool: Through federal funds futures prices, observe market expectations for future rate hike/cut probabilities—an essential reference tool for investors.

- Dot Plot: Understand FOMC members' median projections for future rate levels to judge long-term policy direction.

Method 3: Combine with Economic Calendar and Data Releases

- Economic Calendar: Track important U.S. and global economic data (CPI, nonfarm payrolls, PCE deflator, etc.), which often drive FOMC policy judgments.

- News Alerts and Professional Analysis: Reuters, Bloomberg, Wall Street Journal, and similar media provide rapid post-meeting interpretation, helping investors understand market consensus.

Through these three layers of information gathering, FOMC trends can be tracked more effectively, avoiding the misjudgment that comes from over-reliance on a single source.

10: FOMC FAQ

Q1: Why are FOMC decisions watched globally?

Because the U.S. dollar is the world's primary reserve currency, FOMC rate adjustments affect global funding costs, cross-border investment flows, and commodity prices.

Q2: What is the FOMC dot plot?

The dot plot is a chart showing each member's individual projection for future rates. It is often used to judge the median policy rate, but it is not a final commitment—rather, it represents "members' rate outlook." The latest version was released in March 2026.

Q3: How many cuts will the Fed make in 2026?

According to the latest dot plot released in March 2026, the median projection is for one more 25bp cut. However, 7 of the 19 members project no cuts in 2026, reflecting significant divergence. The current market base case is "first cut possibly in June," but this depends on inflation and employment data.

Q4: Who is Kevin Warsh and when does he take office?

Warsh is a former Fed Governor (2006–2011) nominated by President Trump as the new Chair on January 30, 2026. After the DOJ closed its investigation into Powell on April 24, 2026, and Senator Tillis withdrew his opposition on April 26, 2026, Warsh's confirmation path is now much clearer after the DOJ ended its Powell investigation and Sen. Tillis withdrew his block. The appointment is widely expected but still requires Senate confirmation before he can take office around May 15, 2026. See §5 Powell's Term Ending and Warsh's Confirmation Outlook for details.

Q5: What's the difference between the FOMC policy statement and the Chair's press conference?

- Policy Statement: Written form, briefly describing economic assessment and policy decisions.

- Chair's Press Conference: Verbal explanation and media Q&A, often releasing additional information; market reactions tend to be more dramatic.

Q6: How do FOMC rate decisions affect the stock market?

Rate cuts lower corporate financing costs and are typically positive for equities; rate hikes raise funding costs and may pressure equities. Actual impact still depends on market interpretation of the economic outlook.

Q7: How do FOMC rate changes affect the foreign exchange market?

Rate hikes typically push up the U.S. dollar (because of higher returns on USD assets); rate cuts may weaken the USD, prompting capital to flow to other markets.

Q8: How should investors position before and after FOMC meetings?

We recommend reducing leverage, controlling positions, and avoiding the volatile period during policy announcements. For the medium and long term, adjust asset allocation based on rate direction—for example, in tightening cycles, emphasize USD and short-term bonds; in easing cycles, prefer equities and commodities.

Q9: Should retail investors pay attention to the FOMC?

Yes. Even if you don't trade FX or U.S. equities, FOMC rate decisions indirectly affect mortgage rates, real estate markets, and global fund performance, making them relevant to all investors.

11: Conclusion

The FOMC is a critical bellwether for global financial markets, and the 2026 policy path is filled with uncertainty:

- Policy front: The easing cycle that began in September 2025 was paused in January 2026. The March SEP shows the market expects only one more cut in 2026, with PCE projections revised up due to inflation stickiness.

- Personnel front: Powell's term ends on May 15. Warsh's tenure may drive Fed framework reform (including reduced meeting count and a review of the inflation-targeting mechanism).

- Timing outlook: The April 28–29, 2026 meeting is expected to hold; the next adjustment window is no earlier than June.

For investors, mastering the details of each FOMC decision, dot plot changes, and the Chair's tonal shifts is core to assessing global asset risks and opportunities. We recommend pairing this with the Titan FX Economic Calendar and Spread Comparison tools to position effectively at critical moments.

Further Reading

- What Is the Fed / FRB?

- What Is Monetary Policy?

- What Is Inflation?

- What Is Non-Farm Payrolls?

- What Is GDP?

Titan FX's financial market research team creates investor education content across foreign exchange, commodities, stock indices, U.S. equities, crypto assets, and other major financial markets.

Primary Sources (by Category)

- U.S. monetary policy and official materials: Federal Reserve FOMC Calendars, March 2026 SEP, March 2026 FOMC Minutes

- Nomination and confirmation process: White House nomination release, Senate Banking Committee hearing

- Market tools and economic indicators: CME FedWatch Tool, Titan FX Economic Calendar