Return on Investment (ROI)

On the road to investing, many people start with searches like "what is ROI," "how to calculate return on investment," or "ROI formula" — hoping to quickly judge whether a given investment is worthwhile.

Return on Investment (ROI) is one of the most intuitive evaluation metrics. It tells you, at a glance, how much return each dollar of invested capital ultimately brought back.

Beginners searching "what is ROI" or "ROI formula" often skip over the time factor and risk factor in the process.

This guide walks through the ROI calculation formula, compares ROI vs. ROE vs. ROA, and explains the difference between annualized return and total return — helping you build a proper evaluation framework.

- 1. What Is Return on Investment (ROI)? Core Concept

- 2. ROI Formula: A Simple Calculation for Beginners

- 3. ROI vs. ROA vs. ROE: The Three Return Metrics Compared

- 4. ROI's Strengths and Limits: Where Are the Blind Spots?

- 5. Practical: Using ROI Across Different Investments

- 6. FAQ: ROI and Annualized Return - Reading Pitfalls

- 7. Summary: Building a Proper Return-Evaluation Lens

1. What Is Return on Investment (ROI)? Core Concept

Return on Investment (ROI) is a metric that measures the ratio between investment return and invested cost. Its meaning is simple: for every unit of capital invested, what percentage of return comes back.

ROI is widely used because it carries extraordinary generality. It evaluates stocks, bonds, and mutual funds; it works on real-estate rental yields; it even applies to enterprise advertising-spend effectiveness. With this one number, investors can quickly compare the early-stage earning power of very different investment types.

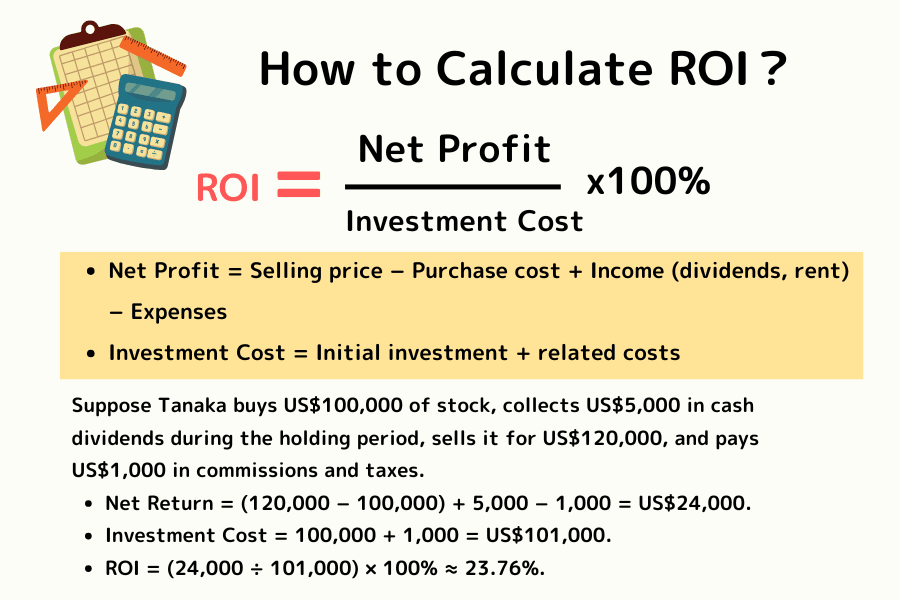

2. ROI Formula: A Simple Calculation for Beginners

Calculating ROI isn't hard — you just need to know how much you put in and how much you ended up with.

Core formula:

ROI = (Net Return ÷ Investment Cost) × 100%

- Net return: Sell price minus buy cost, plus any dividends or rental income earned during holding, minus taxes, commissions, and custody fees.

- Investment cost: The total amount originally invested, including any transaction-related taxes and fees.

Worked Example

Suppose Tanaka buys US$100,000 of stock, collects US$5,000 in cash dividends during the holding period, sells it for US$120,000, and pays US$1,000 in commissions and taxes.

- Net Return = (120,000 − 100,000) + 5,000 − 1,000 = US$24,000.

- Investment Cost = 100,000 + 1,000 = US$101,000.

- ROI = (24,000 ÷ 101,000) × 100% ≈ 23.76%.

3. ROI vs. ROA vs. ROE: The Three Return Metrics Compared

When reading financial statements or evaluating a company, you'll often encounter ROA (Return on Assets) and ROE (Return on Equity). They look similar but answer different questions.

Side-by-Side Comparison

| Metric | ROI (Return on Investment) | ROE (Return on Equity) | ROA (Return on Assets) |

|---|---|---|---|

| Perspective | External investor (individual / institutional) | Shareholder (capital provider) | Internal (management) |

| Formula | (Net Return ÷ Investment Cost) × 100% | (Net Income ÷ Equity) × 100% | (Net Income ÷ Average Assets) × 100% |

| Core logic | Profit percentage on a specific position | Efficiency of using shareholder capital | Operating capability across all resources |

| Best for | Judging a stock, property, or single project | Company earning speed & dividend potential | Resource-utilization efficiency in asset-heavy sectors |

| Leverage impact | Reflects personal investment leverage | Higher debt can inflate ROE | Includes debt in denominator - leverage-agnostic |

| Main strength | Most intuitive and universal | Core metric for shareholder value | Exposes over-reliance on borrowing |

Key Distinction

ROI is a scorecard an investor gives to a specific position; ROA and ROE are diagnostic of company fundamentals.

If a company's ROE is conspicuously higher than its ROA, the business is usually amplifying returns via financial leverage — and debt risk deserves a closer look.

4. ROI's Strengths and Limits: Where Are the Blind Spots?

ROI's biggest strengths are that it is simple and universal — anyone can calculate it, and the same formula applies to stocks, funds, real estate, and businesses alike.

But the limits are real:

- It ignores time: a 15% return over 1 year and a 100% return over 10 years aren't directly comparable.

- It ignores risk: a high ROI investment often carries high risk.

- It doesn't capture opportunity cost.

Beginners should therefore pair ROI with annualized return or risk metrics for a more complete judgment.

5. Practical: Using ROI Across Different Investments

In practice, ROI works best when combined with other supporting tools.

Strategy 1: Build Every Hidden Cost Into the Math

When calculating real-estate ROI, don't just count rental income. Deduct property tax, land tax, maintenance, and management fees. For stocks, factor in trading taxes and the costs of frequent activity.

Strategy 2: Set a Benchmark

Whether a 5% ROI is "good" depends on the market context. If the S&P 500 returned 10% that year, a 5% return actually underperformed the benchmark.

Strategy 3: Pair with Cash-Flow Observation

Some high-ROI items show only paper gains without actual cash inflow. Quality investments should generate stable ROI and consistent cash returns.

6. FAQ: ROI and Annualized Return - Reading Pitfalls

Q1: What's the difference between total return and annualized return?

Total return (ROI) shows the cumulative result over the entire holding period. Annualized return (CAGR) normalizes the gain to a per-year average, which is essential when comparing investments with different holding periods.

The CAGR formula:

CAGR = (Ending Value ÷ Beginning Investment)^(1 ÷ Years) − 1

Example: invest US$100,000 and it becomes US$150,000 after 3 years. ROI = 50%, but CAGR ≈ 14.47%. Only after normalizing the time horizon can you fairly compare compounding efficiency.

Q2: How do I calculate "total return with dividends"?

Add the cash dividends received into the net return. If dividends are reinvested, compounding lifts the long-run ROI meaningfully above the ex-dividend figure.

Q3: What does a negative ROI mean?

The investment is loss-making — the sale price plus any income during the period is still below the initial cost. That's a signal to re-examine the thesis, set a stop-loss, or rebalance.

Q4: Is a higher ROI always better?

Usually a higher ROI is better, but risk and stability must be weighed in. High ROI often comes with high risk.

Q5: Should I include commissions and taxes in ROI?

Yes. Including every relevant cost is the only way to arrive at the true return.

7. Summary: Building a Proper Return-Evaluation Lens

Return on Investment (ROI) is a simple, effective starting metric, but don't lean on any single number. Combine ROI with ROE, ROA, and annualized return, and weigh risk and time.

Beginner ROI Checklist:

- Did the calculation deduct every fee and tax?

- Are you comparing annualized return rather than pure total ROI?

- Did you consider risk and opportunity cost?

- Did you benchmark against the market or a personal target?

Tracking how ROI changes over time — and understanding the story behind each move — is what ultimately compounds into a steadier long-term strategy.

Titan FX Trading Strategy Research Institute

The financial markets research team at Titan FX. Produces educational content for investors across a broad range of asset classes, including foreign exchange (FX), commodities (crude oil, precious metals, agricultural products), stock indices, US equities, and cryptocurrencies.

Primary sources: SEC EDGAR, NYSE Listed Companies, IFRS, U.S. GAAP (FASB), Bloomberg, Reuters