Options

From stocks and indices to forex and commodities, a growing number of investors want to take part in market moves—and manage risk—without actually holding the underlying asset. Options are one of the key tools that can do both.

This structure lets investors take part in market moves with a relatively small amount of capital, while also gaining flexibility for risk management and strategy. Across global financial markets, options are widely used for hedging, speculation, and income strategies, making them one of the key trading tools for many professional investors. That said, income strategies usually involve selling options: while the seller collects a premium, they may also take on significant assignment risk, so these strategies are not suitable for beginners who do not yet understand the risks.

This article covers the basic definition and mechanics of options, their main building blocks, the two core types, their benefits and risks, and how options compare with contracts for difference (CFDs)—helping you build a solid foundation for understanding this instrument.

- Options trade the right, not the obligation, to buy or sell.

- Premium, strike price, and expiry drive an option's value.

- Calls profit from rises; puts profit from falls.

- Time decay works against the buyer, and leverage cuts both ways.

- Sellers collect a premium but take on far greater risk.

1. What Are Options? Basic Definition and How They Work

Options are derivative contracts that give the buyer the right—but not the obligation—to buy or sell an underlying asset at a preset price within a specific future period or on a specific date.

Unlike buying or selling a stock directly, the essence of an option is trading a right rather than trading an asset.

- The buyer pays a premium to the seller and, in return, gains the choice to exercise or abandon that right in the future.

- The seller receives the premium but must fulfill the corresponding obligation if the buyer exercises the right.

This allows investors to take part in relatively large market moves with a comparatively small amount of capital, and to design different strategies based on their own view of future prices, volatility, and the passage of time.

The core of an option's design lies in the asymmetry between the roles of buyer and seller. When simply buying an option, the buyer's maximum loss is usually limited to the premium paid. Among these, a long call has profit potential that can theoretically expand as the underlying price rises, while a long put profits when the underlying price falls—though its maximum gain is capped by the underlying price falling to zero.

By contrast, the seller can collect a premium but must also take on the obligation to fulfill the contract, and typically has to post margin to guarantee performance. Selling a call without holding the underlying can, in theory, expose the seller to unlimited losses; selling a put can lead to substantial losses if the underlying price falls sharply.

So while options are a flexible risk-management tool that can also be used for speculation and hedging, beginners should first understand their leverage characteristics, time decay, and seller assignment risk before considering real trades.

2. Main Building Blocks: Premium, Strike Price, and Expiration

An option's value is determined by several core components. Understanding these is the foundation for beginners.

Premium

The premium is the fee the buyer pays the seller to obtain the option's right. Think of it as an insurance premium: after paying this fee, the buyer gains the choice to exercise or abandon the contract in the future.

The level of the premium is affected by many factors—including the underlying price, strike price, remaining time, market volatility, interest rates, and dividends—and it is the real-time market price of the option.

Strike Price

The strike price is the execution price agreed on by both parties. For example, if a buyer holds a call with a strike price of 100, they have the right to buy the asset at 100 in the future. For a put, it means the buyer has the right to sell the asset at the strike price.

The gap between the strike price and the current market price affects whether the option has immediate exercise value, and it also affects the level of the premium.

Expiration Date

The expiration date is the last valid day of the option contract. After this date, the contract usually expires automatically and the buyer loses the right to exercise.

Options carry a time limit, and the closer they get to expiration, the more their time value generally erodes—a time cost that buyers should watch closely. That said, the actual window for exercise depends on the contract type: American options can usually be exercised any time before expiration, while European options can usually only be exercised on the expiration date.

In-the-Money, At-the-Money, and Out-of-the-Money

In the real-time trading of options and other derivatives, a contract usually shows one of three intrinsic-value states, depending on the relationship between the strike price and the current market price.

Note that the table below uses a call as the example; for a put, the direction of in-the-money and out-of-the-money is reversed.

| Moneyness | Intrinsic value | Example: a call with a current price of 100 |

|---|---|---|

| In-the-Money (ITM) | Already has immediate exercise value | Strike price of 90; can buy below the current price |

| At-the-Money (ATM) | Strike price is close to the current market price | Strike price of 100; near the current price |

| Out-of-the-Money (OTM) | No immediate exercise value; mainly time value remains | Strike price of 110; above the current price, with no exercise benefit for now |

3. The Two Core Types: Calls and Puts

Options mainly fall into two types: calls and puts. The two move in opposite directions, and investors can choose between them based on their market view and risk-management needs.

Call Option

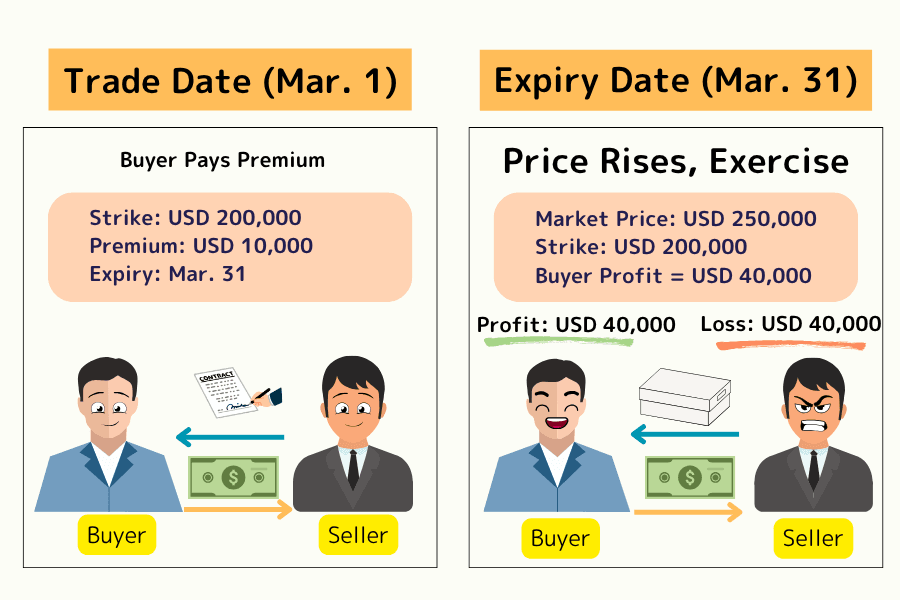

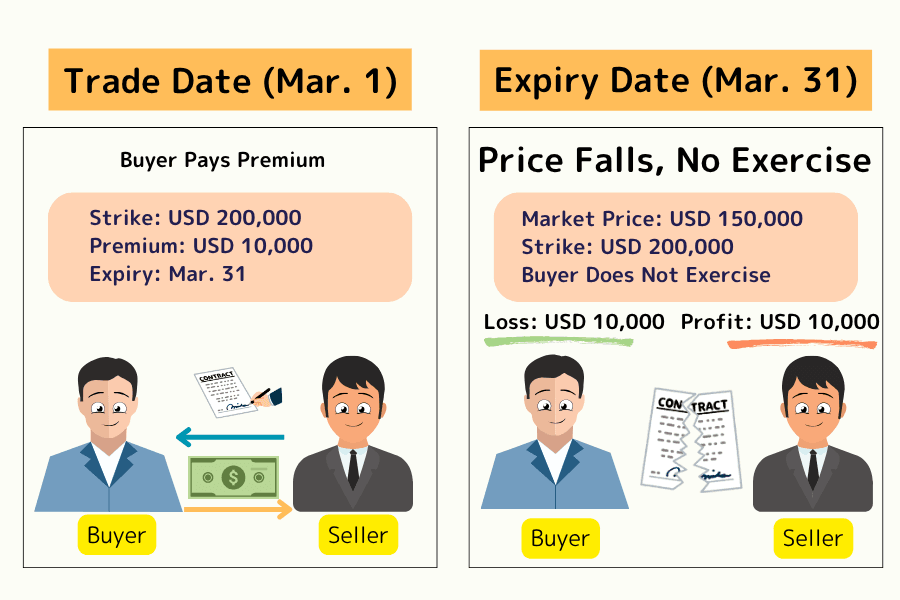

A call gives the buyer the right to buy the underlying asset at a specific price during the agreed period or on the expiration date, with the actual exercise window depending on the contract type.

When an investor expects the underlying price to rise, they typically consider buying a call. If the underlying price is clearly above the strike price, the call's value may rise, and the buyer can realize a gain by closing the position or exercising.

However, a call does not guarantee a profit just because the market goes up. Buyers still need to account for the premium cost, time decay, changes in implied volatility, and time to expiration. If the underlying price does not rise enough to cover the premium cost, the buyer can still lose money.

Put Option

A put gives the buyer the right to sell the underlying asset at a specific price during the agreed period or on the expiration date, with the actual exercise window again depending on the contract type.

When an investor expects the underlying price to fall, they typically consider buying a put. Puts are also often used as a hedging tool for existing holdings—for example, an investor holding a stock or index position can reduce downside risk by buying a put.

However, a put is likewise affected by the premium, time decay, and implied volatility. If the underlying price does not fall as expected, or does not fall enough to cover the premium cost, the buyer can still lose part or all of the premium.

Calls vs. Puts at a Glance

| Item | Call | Put |

|---|---|---|

| Basic direction | Bullish | Bearish |

| Buyer's right | Buy the underlying at the strike price | Sell the underlying at the strike price |

| Common uses | Participate in rallies; build bullish strategies | Hedge downside; build bearish strategies |

| Max loss for a simple buyer | The premium paid | The premium paid |

| Main risks | Premium going to zero; time decay | Premium going to zero; time decay |

4. Benefits and Risks of Options

Options offer strategic flexibility but also carry higher risk. Beginners need to understand their price-movement logic, time value, and leverage characteristics before using them rationally.

Main Benefits

- Higher capital efficiency: The buyer only needs to pay a premium to gain exposure to the underlying asset's price movements, so capital is used more efficiently.

- Relatively clear risk for buyers: When simply buying an option, the maximum loss is usually limited to the premium paid, so investors know their maximum potential loss before entering.

- High strategic flexibility: Options can be structured around market direction, changes in volatility, and risk-management needs, and can suit bullish, bearish, or range-bound conditions.

Main Risks

- Time decay: As expiration approaches, an option's value may gradually decline. Even if your directional view is broadly correct, you can still lose money due to the passage of time or an insufficient price move.

- Large premium swings: A small move in the underlying, a change in implied volatility, or a shortening time to expiration can all cause the premium to move sharply.

- Higher risk for sellers: The party selling an option can collect a premium but must take on the obligation to fulfill the contract. Selling a call without holding the underlying can, in theory, expose the seller to unlimited losses; selling a put can lead to substantial losses if the underlying price falls sharply.

- A higher learning curve: An option's price is affected not only by the underlying price but also by time value, volatility, interest rates, and dividends. Beginners who do not understand the pricing logic tend to underestimate the risks.

Therefore, when getting started with options, beginners should begin with basic concepts, demo trading, or small positions, gradually becoming familiar with premium changes, time decay, and the profit-and-loss structure of different strategies—and avoid using complex strategies or seller strategies before understanding the risks.

5. Beyond Options: Understanding Contracts for Difference (CFDs)

Beyond options, investors may also come across derivatives such as futures, contracts for difference (CFDs), and margin trading. These can all be used to take part in market moves, but their risk structures, capital requirements, and mechanics differ.

What Is a Contract for Difference (CFD)?

A contract for difference (CFD) is a derivative that tracks the price movements of an underlying asset. Investors do not need to actually hold the stock, index, currency, or commodity—instead, they trade based on changes in the underlying price.

CFDs usually do not have the fixed expiration date and premium structure of options, and their profit and loss mainly moves with the underlying price. However, CFDs are leveraged products, so you need to watch for margin requirements, overnight costs, price gaps, and forced liquidation risk—none of which means they are lower-risk or more suitable for beginners.

Key Differences Between Options and CFDs

| Item | Options | CFDs |

|---|---|---|

| Expiration | Usually a fixed expiration date | Usually no fixed expiration date |

| Cost structure | The buyer pays a premium | Margin-based; overnight costs may apply |

| Time value | Time decay exists | No option-style time value, but overnight costs may apply |

| Direction | Express a view via calls, puts, or combined strategies | Go long or short directly |

| Capital threshold | Buyer pays a premium; seller usually needs margin | Margin-based; positions can be built with less capital, but leverage magnifies risk |

| Main risks | Time decay; premium going to zero; seller assignment risk | Leverage magnifying losses; forced liquidation; overnight costs; price gaps |

| Common use cases | Hedging; volatility trading; combined strategies | Short-term trading or risk management by experienced traders |

CFDs can be one of the tools experienced traders study for short-term trading or risk management, but they should not be seen as a simple substitute for options or long-term investing.

For investors who want to take part in global market moves through CFDs, Titan FX offers forex, precious metals, energy, indices, and other CFD products—well suited as an advanced tool for experienced traders who want to observe how different markets move.

Whether options or CFDs, both are fundamentally leveraged financial instruments that can magnify both gains and losses. Before investing, you should fully understand the product's characteristics, margin rules, and risks, and set up sound money management and risk controls.

6. Options FAQ

Q1. What mainly determines an option's premium?

The premium is mainly affected by factors such as the underlying asset's price, the strike price, the time remaining to expiration, implied volatility, interest rates, and dividends.

Generally, the longer the time to expiration and the higher the implied volatility, the higher the premium tends to be. That said, the actual price is still influenced by market supply and demand and the volatility of the underlying asset.

Q2. Do you have to hold an option until expiration?

Not necessarily. Investors can usually close a position early through an offsetting trade before expiration, so you do not have to hold until the expiration date.

However, whether you can close smoothly depends on market liquidity, the bid-ask spread, and the contract rules. Options with poor liquidity may be harder to fill or come with higher trading costs.

Q3. What is the biggest difference between options and futures in terms of risk structure?

The biggest difference lies in the different structure of rights and obligations.

With futures, both the buyer and the seller have an obligation to perform, profit and loss usually changes fairly linearly with the underlying price, and daily settlement and margin maintenance are required. If the market moves sharply, investors may face margin calls or forced liquidation.

With options, the buyer holds the right and the seller takes on the obligation. When simply buying an option, the buyer's maximum loss is usually limited to the premium paid; but selling an option can mean taking on higher assignment risk, especially with a naked call, where losses can in theory be unlimited.

Q4. How should beginners choose a strike price?

The strike price directly affects the premium cost, the probability of success, and how profit and loss change.

In-the-money contracts usually cost more but already carry some intrinsic value; at-the-money contracts are more sensitive to changes in the underlying price; out-of-the-money contracts have lower premiums but need a more pronounced move in the underlying price to have a chance of gaining value.

Beginners can first use demo trading or small positions to observe how in-the-money, at-the-money, and out-of-the-money contracts differ under price swings, time decay, and changes in implied volatility—then gradually understand the risk and suitable scenarios for each strike price.

Q5. What happens after an option expires?

After an option expires, the contract is handled according to its state and market rules.

If the contract is out-of-the-money at expiration, it usually expires worthless, and the premium the buyer paid may go entirely to zero. If the contract is in-the-money at expiration, it may be exercised, cash-settled, or handled automatically according to the rules of the exchange or broker.

So before trading, investors should understand the expiration rules, settlement method, and broker handling of the product they trade, to avoid unexpected changes in their position at expiration.

Q6. Can an option's premium go to zero?

Yes. If a bought option is out-of-the-money at expiration, the buyer usually will not exercise the right, the contract expires worthless, and the premium paid may go entirely to zero.

So although buying an option usually limits the maximum loss to the premium, that does not mean the risk is low. If your directional view is wrong, the move is insufficient, or time value decays quickly, you can still lose the entire premium.

7. Summary

Options are a derivative that combines strategic flexibility with leverage characteristics, and they can be used for hedging, speculation, volatility trading, and strategy allocation across different market conditions.

For beginners, learning options should start with the core concepts—the basic definition, premium, strike price, expiration date, and calls versus puts—before moving on to understand time decay, implied volatility, and seller assignment risk.

Options are not a tool that profits simply from getting the direction right. Even if the underlying price moves as expected, the final result can still be affected by the premium cost, the passage of time, or changes in volatility. So before trading for real, investors should get familiar with the profit-and-loss structure through demo trading or small positions, and avoid using complex strategies before understanding the risks.

As trading experience builds, investors can go on to explore other derivatives such as CFDs and futures. However, these tools all carry leverage risk by nature and can magnify both gains and losses. Whatever tool you use, money management, risk control, and continuous learning are foundations you cannot ignore for long-term participation in the markets.

Further Reading

- What Are Derivatives?

- What Is a CFD (Contract for Difference)?

- What Are Futures?

- What Is Leverage?

- What Is Volatility?

Titan FX Trading Strategy Lab. We produce investor-education content covering forex, commodities (crude oil, precious metals, agricultural goods), stock indices, US equities, and digital assets.

Primary Sources (by category)

- Exchanges & clearing: Cboe (Chicago Board Options Exchange) — options contract specifications and market data; OCC (Options Clearing Corporation) — options exercise and settlement rules

- Regulators & investor education: U.S. Securities and Exchange Commission (SEC) Investor.gov — options basics and risk disclosure

- Academic & theory: Black, F. & Scholes, M. (1973) "The Pricing of Options and Corporate Liabilities", Journal of Political Economy — options pricing theory; Hull, J. C. Options, Futures, and Other Derivatives — the standard derivatives textbook