Stock Par Value

Stock par value, also known as face value, refers to the nominal value printed on the stock certificate. The par value per share is usually fixed and set by the company when issuing stock. Although it is not directly related to the market price of the stock, par value is an important element in calculating a company’s capital in accounting.

- Stock Par Value definition and its role in share capital accounting

- Formula: Share Capital = Issued Shares × Par Value, with examples

- Why par value is largely separate from market price and BPS

- Par Value vs No Par Value Stock: jurisdictional differences

- Investment relevance: par value is historical, modern decisions use PER/PBR/ROE

1. What is Stock Par Value?

Simply put, stock par value represents a fixed value per share. When a company issues shares, it divides the initial investment into many shares, and the value represented by each share is the par value. Par value is usually stated per share, and in accounting, capital is calculated by multiplying the par value by the number of shares issued.

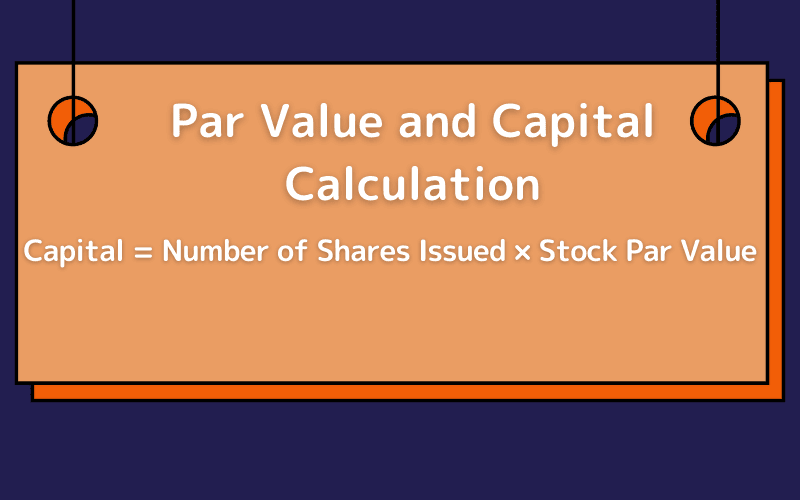

Par Value and Capital Calculation

In accounting, the capital (or equity) is calculated as the par value multiplied by the number of shares issued. The formula is as follows:

Capital = Number of Shares Issued × Stock Par ValueFor example, suppose a company has a capital of 1 million dollars, and the par value per share is set to 1 dollar. This means the company will issue 1 million shares.

2. Changes and Impact of Stock Par Value

1. Changes in Stock Par Value in the United States

Before 1982, most companies in the United States were required to issue shares with a par value, which typically ranged from $1 to $100. However, in 1982, the U.S. Securities and Exchange Commission (SEC) allowed companies to issue no-par-value stock.

This move provided greater flexibility for companies when issuing shares, enabling them to avoid setting an arbitrary value that had no direct impact on market pricing or capital raising. As a result, most modern U.S. corporations issue no-par-value stock, focusing on market-driven share prices rather than the nominal par value.

2. Par Value of Stocks in International Markets

In international stock markets, particularly in the US, stock par values are typically more flexible. For instance, the par value of stocks issued by US companies may be set to 1 dollar, 0.1 dollar, or even 0.01 dollars. This flexibility allows investors to adjust stock prices and issuance terms according to market demand.

3. The Relationship Between Par Value and Stock Price

1. No Direct Relationship Between Par Value and Stock Price

The par value of a stock is primarily a basis for calculating capital and does not directly impact the stock price. The price of a stock is mainly determined by market supply and demand, the company’s fundamentals, and future profit expectations. Therefore, even if a company has a high or low par value, it does not directly dictate the stock price.

For example, if a company’s capital is 1 billion dollars but its fundamentals are poor, with limited growth potential in the industry, the stock price may still remain low. On the other hand, if a company has a smaller capital but strong fundamentals and broad prospects, its stock price could be higher.

2. Par Value Is Not the Same as Stock Book Value

Stock book value refers to a company’s actual value, i.e., the equity available to shareholders. The book value is calculated from the company's financial statements and reflects the value left over after liabilities are deducted, distributed per share.

On the other hand, stock par value is an accounting unit for calculation and is not related to the company’s actual asset value. Therefore, the par value of a stock is not the same as its book value.

4. No Par Value Stocks vs. Par Value Stocks

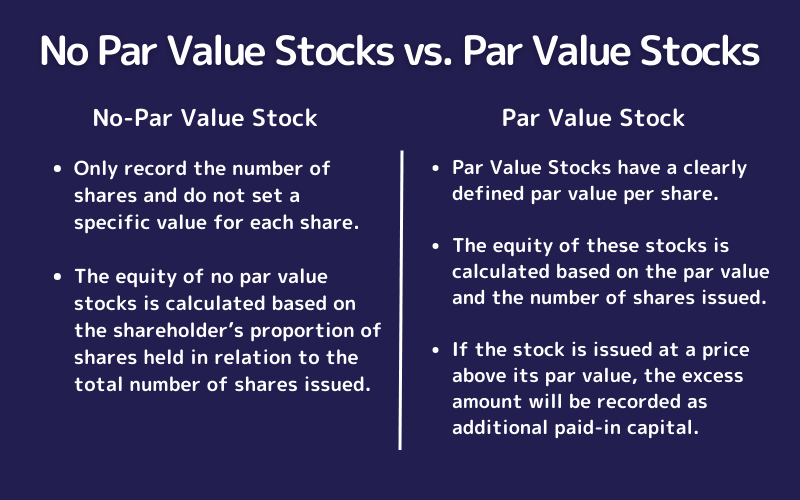

1. No Par Value Stocks

No Par Value Stocks are those that do not specify a specific par value per share. These stocks only record the number of shares and do not set a specific value for each share. The equity of no par value stocks is calculated based on the shareholder’s proportion of shares held in relation to the total number of shares issued.

The key advantage of no par value stocks is their greater flexibility, especially in the issuance process, as companies can adjust terms based on their needs.

2. Par Value Stocks

Par Value Stocks have a clearly defined par value per share. The equity of these stocks is calculated based on the par value and the number of shares issued. If the stock is issued at a price above its par value, the excess amount will be recorded as additional paid-in capital.

For example, if a company issues stock with a par value of 10 dollars per share and an investor purchases the stock for 20 dollars per share, the excess amount of 10 dollars will be recorded as additional paid-in capital.

5. The Impact of Changes in Par Value on Company Operations

Reasons for Changing Stock Par Value

Companies may adjust the par value of their stocks for several reasons:

Stock Splits: To reduce the price of each share and make the stock more attractive to market demand, some companies may perform a stock split, reducing the par value per share. For example, a company might split a 10-dollar par value share into two 5-dollar shares, making each share more affordable and potentially attracting smaller investors.

Stock Consolidation: If a company’s stock par value is too low, it may choose to consolidate its shares, increasing the par value. For example, the company may consolidate shares with a par value of 1 dollar into 5-dollar shares, thus raising the stock price and reducing the number of shares, which could make the company appear more attractive.

6. Frequently Asked Questions (FAQ)

Q1. What's the difference between par value and market price?

Par value is a fixed nominal amount set in the corporate charter; market price is the dynamic trading price reflecting earnings, growth, and macro conditions. For example, Toyota with par value of ~10 yen trades around 3,000 yen — the two metrics are largely independent.

Q2. Which is more common, par-value or no-par-value stock?

Since the 2001 Commercial Code revision, virtually all Japanese listed companies use no-par-value stock. The US has nominal par values (often 1 cent). Par value remains legally meaningful in Taiwan and Hong Kong markets.

Q3. Is par value useful for investment decisions?

Rarely. Modern valuation uses PER, EPS, ROE, PBR, dividend yield, and growth metrics. Par value is a historical accounting construct that can usually be set aside.

Q4. How does par value change during a stock split?

It decreases proportionally to the split ratio. A 1:2 split on 100-yen par value reduces it to 50 yen, with share count doubling. Total shareholder value (shares × par) remains unchanged.

Q5. When should foreign investors care about par value?

Generally not, but specific contexts matter: Taiwan/Hong Kong listings, rights issues (where below-par issuance may be restricted), accounting analysis with capital reserves, and cross-border M&A involving par-value jurisdictions.

7. Conclusion

Stock Par Value is a historical accounting construct that originally served as the basis for share capital calculation and creditor protection. In modern markets, however, par value has become largely symbolic — most jurisdictions (Japan, US, UK) have moved to no-par-value systems, while Taiwan and Hong Kong retain par value in their statutory framework.

For investment decisions, par value provides little practical signal. Modern valuation relies on PER, EPS, ROE, PBR, dividend yield, and growth metrics that directly reflect a company's earnings power and asset base. Investors should:

- Recognize par value as a legacy accounting concept, not a market signal

- Focus on PER/PBR/ROE for valuation assessment

- Distinguish par value from BPS (Book Value per Share) — they are unrelated

- Check par value rules only when relevant: Taiwan/HK listings, rights issues, or cross-border M&A

Treat par value as part of a company's regulatory and accounting structure, but anchor investment decisions on profitability, growth, and capital efficiency metrics.

Further Reading

Titan FX Research Team. We cover a broad set of financial instruments — foreign exchange, commodities, equity indices, US equities, and digital assets — producing practical, research-backed educational content for investors.

Primary Sources

- Par value fundamentals: Investopedia — Par Value, Corporate Finance Institute — Par Value

- No-par-value systems: JPX — Equity issuance rules, SEC — No Par Value Stock

- Cross-market comparison: Taiwan Stock Exchange, Hong Kong Stock Exchange — Listing Rules