How to Read Financial Statements: Income, Balance & Cash Flow

When you first start investing in US equities, a dense stack of financial reports can be intimidating. Companies frequently post record-high revenue in the news, yet their share price still falls after earnings — the key usually isn't any single number, but the relationships between figures.

Financial statements are not just tools for accountants. They are the most important basis on which investors judge a company's underlying health, growth potential, and risk. With the right reading order and core framework, even beginners can quickly see whether a company is genuinely profitable, whether its cash position is solid, and whether it has the makings of long-term competitiveness.

This guide walks through the three core financial statements from scratch — income statement, balance sheet, and cash flow statement — and lays down a practical, repeatable framework for financial analysis.

1. What Are Financial Statements?

Financial Statements are the formal documents through which a company periodically discloses its financial condition and operating results, showing how funds move at specific points in time and across specific periods. The three core reports in a complete financial-statement set are the income statement, balance sheet, and cash flow statement.

| Core Statement | Primary Role | Viewpoint |

|---|---|---|

| Income Statement | Measures the company's "earning power" | Performance across a continuous period (flow) |

| Balance Sheet | Measures the company's "asset base" | Static snapshot at a specific date (stock) |

| Cash Flow Statement | Measures "where the money actually is" | Flow in and out over a continuous period |

2. The Three Core Statements Explained: Income, Balance, Cash Flow

To build a solid foundation, we walk through each statement using the day-to-day operations of Mr. Tanaka's coffee shop.

Income Statement: A Report Card for Operating Profitability

The income statement focuses on all revenue and expenses a company generates over a period (a quarter or a year) and ends with a "net income" figure that reflects operating efficiency.

Operating Income = Revenue − Cost of Goods Sold − Operating Expenses

| Key Line Item | Definition | Coffee-Shop Example |

|---|---|---|

| Revenue | Total amount collected from selling goods or services — the original source of profit. | Total sales of coffee and pastries. |

| Cost of Goods Sold | Direct expenses incurred to produce the product; reflects raw production efficiency. | Cost of coffee beans, milk, and paper filters. |

| Operating Expenses | Costs to keep the business running day to day; generally not linearly proportional to volume. | Rent, advertising, and staff salaries. |

| Net Income | What remains for shareholders after every cost, fee, interest, and tax is accounted for. | Residual profit after paying every expense. |

Moving from revenue down through costs and expenses to net income reflects a company's ability to convert "sales into actual profit" — the most intuitive path for assessing operating efficiency.

When reading the income statement, pay particular attention to whether revenue is growing consistently, whether gross margin is stable, and whether net income is being converted into real cash.

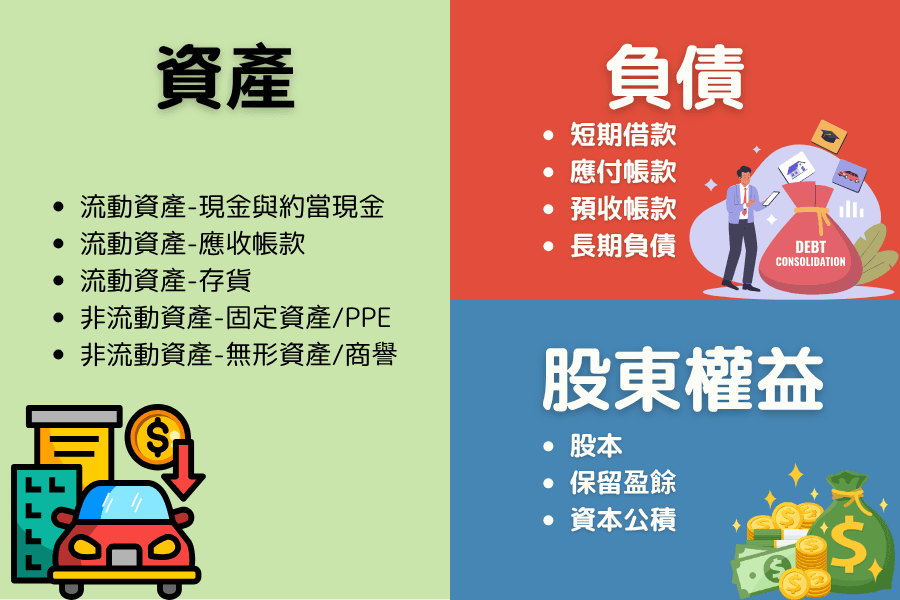

Balance Sheet: A Health Check of Financial Strength

The balance sheet freezes the company's asset mix and debt profile at the closing date, showing its "financial worth" at that specific moment. Put simply, it answers: "What does the company own right now, what does it owe, and how much actually belongs to shareholders?"

Assets = Liabilities + Shareholders' Equity

| Key Line Item | Definition | Coffee-Shop Example |

|---|---|---|

| Assets | Resources owned by the company that are expected to generate future economic benefits. | Imported espresso machines, bar fit-out, cash in the bank. |

| Liabilities | Current economic obligations — future cash or services the company must deliver. | Startup bank loans, unpaid supplier invoices. |

| Shareholders' Equity | Net value after subtracting liabilities from assets; the genuine value attributable to investors. | Equipment value plus cash remaining after debts are cleared. |

The core of this statement lies in watching the debt ratio and current ratio. A healthy balance sheet provides ample liquidity, so the company can keep servicing its debts through downturns or unexpected costs without heading into insolvency.

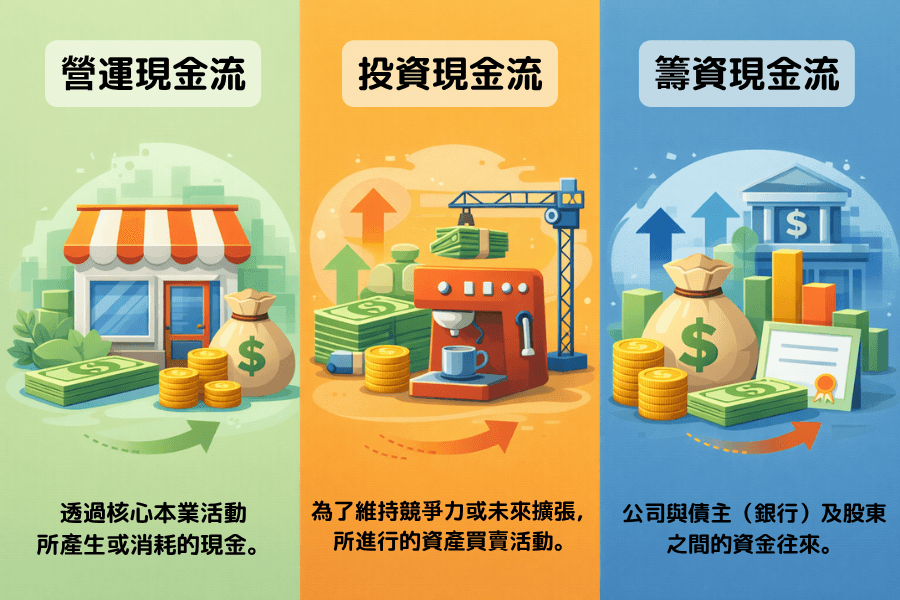

Cash Flow Statement: A Compass for Tracking the Flow of Funds

The cash flow statement tracks how cash actually flowed in and out over a given period, revealing whether the company's funding is stable and whether it can sustain operations.

Net Change in Cash = Operating Cash Flow + Investing Cash Flow + Financing Cash Flow

| Key Line Item | Definition | Coffee-Shop Example |

|---|---|---|

| Operating Cash Flow | Cash generated by core business activities; indicates whether the company can sustain itself. | Net cash in the register at the end of each day after covering small expenses. |

| Investing Cash Flow | Capital deployed for future growth, or proceeds from selling long-term assets. | Mr. Tanaka spending cash to buy a new coffee machine for expansion. |

| Financing Cash Flow | Funds exchanged between the company and its creditors or shareholders. | New bank financing, or dividend payments to partners. |

Cash flow is the lifeblood of a business. Investors should particularly watch whether operating cash flow exceeds net income over the long term. If book profits soar every year but cash never hits the company's pocket, receivables may be ballooning or inventory may be piling up — both latent risks.

How the Three Statements Connect: A Linked Cycle of Data

The three statements do not stand alone — they influence and feed into one another.

Put simply: a number you see in one statement typically also appears in the other two.

Linkage 1: Profit Rolling Forward (Income Statement → Balance Sheet)

The "net income" from the income statement — after subtracting dividends paid to shareholders — rolls into the balance sheet's "retained earnings." This is how a company's stock of wealth (shareholders' equity) grows with good operating performance.

Linkage 2: Cash Reconciliation (Income Statement → Cash Flow Statement)

The cash flow statement starts from net income on the income statement, then adds back non-cash expenses (such as depreciation and amortization) and adjusts for changes in receivables, inventory, and other working-capital items, reconciling the accounting profit to the actual cash moving in and out.

Linkage 3: Asset Depreciation (Balance Sheet → Income Statement)

When a company buys equipment (like a coffee machine), it is first recorded as a "fixed asset" on the balance sheet. That spending then flows through the income statement over the equipment's useful life in the form of "depreciation expense," shaping reported profit year by year.

3. Practical Use: How Investors Interpret and Apply Financial Statements

Facing dense financial data, investors should start with structured analysis instead of staring at any single number in isolation.

Reading Order and a Quick Judgment Framework

In practice, this order gets you from zero to a working picture of a company fast.

First, observe the trend of revenue and net income on the income statement to confirm the company has both growth potential and basic earning power.

Next, check the operating cash flow on the cash flow statement — is it consistently positive and higher than net income? That shows earnings have real cash behind them.

Finally, read the cash reserves and debt structure on the balance sheet to confirm the company has enough financial stability to weather market volatility.

Key Practical Points

- Gross margin and operating margin: These are indicators of product quality. If revenue is rising but margins are slipping, the company may be facing competitive pressure or losing control of costs.

- Free Cash Flow (FCF): Operating cash flow minus capital expenditures. Only when FCF is consistently positive does a company have the headroom for long-term expansion and shareholder returns.

- Asset structure analysis: If inventory and receivables are rising markedly faster than revenue, sales may be slowing or collection risk may be climbing.

4. FAQ: Financial-Statement Details Beginners Miss

Q1: Does a high net income (or EPS) mean the company is flush with cash right now?

Not necessarily. Net income is a book figure that can include uncollected receivables or non-cash asset appreciation. If operating cash flow is thin, the company may end up "profitable on paper, cash-poor in reality."

Q2: Why is the cash flow statement often considered more important than the income statement?

Because the cash flow statement shows real cash, while the income statement can include revenue not yet received or expenses not yet paid. Over the long haul, a company without cash simply cannot continue operating.

Q3: Why do US-equity investors place special emphasis on "Free Cash Flow (FCF)"?

Free Cash Flow measures how much real cash is left after paying salaries, funding equipment maintenance, and covering every other necessity. The formula is:

Free Cash Flow (FCF) = Operating Cash Flow − Capital Expenditures

Operating cash flow is real cash earned from the core business. Capital expenditures are the spending needed to keep the business competitive. Only when FCF is positive does a company have the room to pay dividends, buy back shares, or pursue acquisitions.

Q4: Where can I find these financial statements?

US-listed companies are required to submit regular filings to the US Securities and Exchange Commission (SEC). You can find them through SEC's EDGAR system, or under each company's "Investor Relations" page, typically as 10-K (annual) or 10-Q (quarterly) reports.

Q5: Can the numbers be manipulated? How should investors guard against that?

Manipulation typically surfaces as a long-term divergence between "cash flow" and "net income." If profits keep rising year after year while operating cash flow is persistently negative and receivables are rising abnormally, investors should be extremely cautious. Reading the independent auditor's opinion is also the first line of defense.

5. Summary: Build Your Own Financial Checklist

Financial statements are the foundational language of US-equity investing. The balance sheet, income statement, and cash flow statement each has a distinct function — only by reading them together can you see the full picture.

For beginners, a practical sequence is: first the income statement to understand earnings, then the balance sheet to assess financial strength, and finally the cash flow statement to check cash health. Internalize this basic reading method and you can make more rational, steadier decisions in US equities — and avoid being misled by surface-level numbers that mask the real risks underneath.

Titan FX Trading Strategy Research Institute

The financial markets research team at Titan FX. Produces educational content for investors across a broad range of asset classes, including foreign exchange (FX), commodities (crude oil, precious metals, agricultural products), stock indices, US equities, and cryptocurrencies.

Primary sources: SEC EDGAR, NYSE Listed Companies, IFRS, U.S. GAAP (FASB), Bloomberg, Reuters