Order Execution

Order execution is the whole process by which a trading platform takes the buy or sell order you send, matches it in the market, and confirms the price and size at which it fills. From the moment you press "buy" or "sell" to the moment a position actually exists, your order passes through several stages: submission, routing, matching, and confirmation.

In forex and contracts for difference (CFDs), the speed and quality of order execution feed straight into the price you actually get, and from there into your trading costs and strategy results. When markets move fast or liquidity is thin, your fill can land away from the price you expected—an easily overlooked but genuinely important part of trading.

This article explains what order execution is, the common order types and execution methods, how platforms handle your orders, and the factors that shape fill quality—so the mechanics behind a "fill" are clear.

- Order execution is how a platform matches your buy or sell order and confirms the fill.

- Market, limit, and stop orders differ; limit and stop orders trigger on price reaching a set level.

- Instant execution may requote you; market execution fills at the available price instead.

- Most forex and CFD brokers today use market execution rather than instant execution.

- Liquidity, volatility, network latency, and VPS use all shape your execution quality.

- 1. What Is Order Execution? The Definition and the Process

- 2. What Are the Common Order Types?

- 3. Execution Methods: Instant Execution vs Market Execution

- 4. How Platforms Handle Orders: Dealing Desk and No Dealing Desk

- 5. What Shapes Order Execution Quality?

- 6. What Happens When Execution Quality Is Poor?

- 7. Order Execution FAQ

- 8. Conclusion

1. What Is Order Execution? The Definition and the Process

Definition: What Order Execution Means

Order execution is the process in which a trading platform receives your buy or sell order, sends it to the market, matches it, and confirms the price and size of the fill. When an order is matched successfully, we say it is "filled"; if the conditions are never met, the order either stays pending or is eventually cancelled.

Put simply, placing an order only sends your intent—execution is the step that actually completes the trade. The gap between the two is usually tiny, but it decides the price at which you end up holding a position.

From Order to Fill: The Basic Process

An order typically passes through the stages below between submission and fill. Knowing this flow helps explain why a fill price can differ slightly from the quote you saw on screen.

| Stage | Description |

|---|---|

| Submission | You choose the instrument, direction, size, and order type, then send the order |

| Routing | The platform passes the order to its price source or liquidity providers |

| Matching | The system pairs the order against the prices and sizes available at that moment |

| Confirmation | The platform returns the result, confirming fill price and size |

| Booking | The position is created and shows up in your account's holdings and margin |

In a market like forex, where quotes change from moment to moment, these stages usually complete within milliseconds. Execution speed and consistency are therefore among the key measures of a trading platform.

2. What Are the Common Order Types?

Different order types carry different fill conditions and execution logic. Knowing how they differ lets you pick the right one for the market and your strategy.

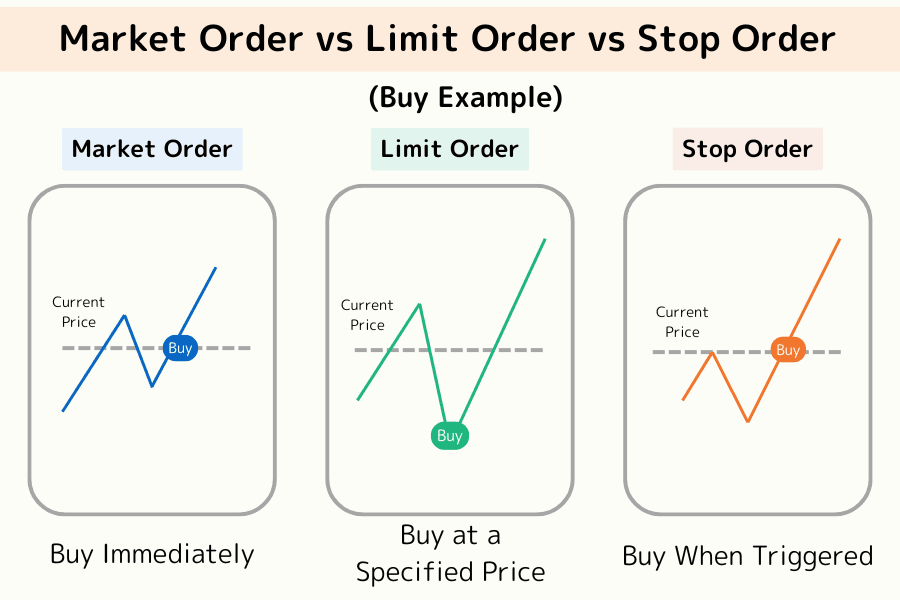

Market Order

A market order fills immediately at the best price available in the market at that moment. It is fast and fills almost every time, which suits situations where you want to get in or out right away.

Note, though, that a market order fills at the price available when it is sent—not the price you saw before pressing the button. In fast-moving markets the actual fill can land slightly away from what you expected, which is known as slippage.

Limit Order

A limit order fills only at a specified price or better. A buy limit sits below the current price and a sell limit above it, and it triggers only when the market reaches your level.

The advantage is control over your fill price, so you avoid buying high or selling low. The drawback is that if price never reaches your level, the order may not fill at all. In some markets, if there isn't enough size available when price does reach it, you can also get a partial fill.

Stop Order

A stop order is sent as a market order once price touches your trigger level. It isn't only for limiting losses—it's also widely used for breakout entries, entering automatically once price clears a range and taking a position in the direction of the move.

Bear in mind that a stop order fills at market once triggered. In fast-moving conditions the actual fill can land away from the trigger price, so filling exactly at your trigger is not guaranteed.

| Order type | Trigger condition | Fill characteristics |

|---|---|---|

| Market order | Sent immediately | Fills at the best available price; fast, but slippage is possible |

| Limit order | Price reaches your level or better | Controls the fill price, but the fill isn't guaranteed |

| Stop order | Price touches the trigger | Fills at market once triggered; used for stops or breakout entries |

3. Execution Methods: Instant Execution vs Market Execution

Beyond the order type, the execution method your platform uses also shapes the result. Forex and CFD platforms commonly use one of two: instant execution or market execution.

Instant Execution

With instant execution you send the order at the price the platform is displaying, and the system tries to fill at that price. If the price has already moved by the time the order arrives, the platform may send a "requote," asking whether you accept the new price.

The upside is a clear, known fill price. The downside is that in fast markets a requote delays your entry, and you can miss the moment you were aiming for.

Market Execution

With market execution your order fills at the price actually available in the market when it is sent, and no requote appears. It's faster because nothing waits on your confirmation—but the fill can slip as price moves.

Today most brokers offering forex and CFDs use market execution, and it is the more common approach in professional trading environments.

| Execution method | Requotes | Main characteristics |

|---|---|---|

| Instant execution | Possible | Clear fill price, but can be delayed when price moves |

| Market execution | None | Faster fills, but slippage is possible |

4. How Platforms Handle Orders: Dealing Desk and No Dealing Desk

Once your order is sent, how the platform actually handles it affects both transparency and where your price comes from. Brokers fall broadly into dealing desk and no dealing desk models, and the differences between DD, NDD, STP, and ECN are often a key consideration when choosing a platform.

Dealing Desk (DD)

Under the dealing desk (DD) model, the broker quotes prices and provides the other side of your order internally, and may take on some orders itself. Quotes tend to be relatively stable, but because the broker is also the price maker, requotes are more likely.

No Dealing Desk (NDD)

Under the no dealing desk (NDD) model, the broker doesn't act as your counterparty on the quote; it routes orders straight to external liquidity providers. NDD execution splits further into STP and ECN:

- ① STP (Straight Through Processing): orders are passed directly to one or more liquidity providers to fill.

- ② ECN (Electronic Communication Network): quotes from multiple liquidity providers are pooled in one electronic network, and the system matches orders automatically on best price and available size—so fills tend to sit closer to the market and are more transparent.

Titan FX, for example, uses NDD with ECN execution, sending orders straight into market matching. That reduces manual intervention and helps keep execution quality steady in normal conditions.

5. What Shapes Order Execution Quality?

The same order can fill very differently depending on market and technical conditions. Below are the main factors that shape execution quality.

Factor 1: Market Liquidity and Depth

Liquidity is how active buyers and sellers are, and how much size can be filled at a given price. When liquidity is ample, orders fill quickly near the expected price. When it's thin—late at night, or around holidays—the gap between your fill and your expectation can widen.

Factor 2: Volatility and Major Events

When key economic data lands, a central bank sets rates, or something unexpected happens, price can move violently in moments. Fills drift further from expectations and slippage becomes more likely. Markets may also trigger halts such as a circuit breaker, which temporarily affects execution.

Factor 3: Network, Server, and VPS

There is transmission time between sending an order and the server receiving it. An unstable connection, or sitting far from the server, stretches that time and lets your fill drift from the quote at the moment you sent it. Traders running automated programs (EAs) often use a VPS (virtual private server) to cut network latency and keep execution more consistent.

6. What Happens When Execution Quality Is Poor?

Order execution looks like a small step in a trade, but when quality is poor the effects cascade through cost, strategy, and mindset. Understanding them helps you weigh both your orders and your platform more carefully.

Effect 1: Higher Trading Costs

Small differences in fill price add up into real money. For high-frequency approaches such as scalping, every instance of slippage or delay chips away at profit and pushes your true costs above what you assumed.

Effect 2: Strategies Stop Behaving as Designed

Many strategies depend on entering and exiting at precise prices. Once fills drift from your levels, your entries and exits shift with them, and the effect the strategy was built around is diluted.

Effect 3: Weaker Automated (EA) Performance

With an EA, execution speed and slippage land directly in your results. When live fill quality departs too far from the assumptions in your backtest, real performance usually falls short.

Effect 4: The Toll on Trading Psychology

Repeated poor fills erode confidence in the platform and the strategy, which can push you into chasing entries or closing early—a cycle that feeds on itself.

Using Tools to Stay Ahead of the Timing

To see the events that can shift execution quality before they land, use the Titan FX economic calendar to track rate decisions, Nonfarm Payrolls, CPI, and other major releases—then avoid placing orders when liquidity is thin or moves are outsized. Keep an eye on your own exposure and position risk as well.

If you want to see how a particular instrument fills across sessions, look at the live quotes and price action of a major pair such as EUR/USD to judge whether liquidity and volatility suit your entry.

7. Order Execution FAQ

Q1. Does placing an order always mean it will fill?

Not necessarily. Market orders usually fill right away, but a limit order fills only if price reaches your level and enough size is available. If the conditions aren't met, the order stays pending or is eventually cancelled.

Q2. Why is my fill price different from the price I saw when ordering?

Because quotes change from moment to moment. A market order fills at the price available when it is sent, not the on-screen quote from before you clicked. That difference is slippage, and it's more likely when the market is moving quickly.

Q3. Is slippage the platform's fault?

Not necessarily. Slippage comes mainly from volatility and shifting liquidity—it is normal in markets and can go in your favour as well as against you. That said, a platform's execution speed and liquidity sources do affect how often it happens and how wide it gets.

Q4. What is a requote?

A requote is what happens under instant execution when price has already moved as your order arrives: the platform comes back with a new price and asks whether you accept it. Market execution doesn't requote—it simply fills at the price available at that moment.

Q5. Which is better, instant execution or market execution?

Each involves a trade-off. Instant execution gives a clear fill price but can requote you; market execution fills faster but can slip. Most forex and CFD platforms use market execution today, though the right choice still depends on your trading style and your platform's terms.

Q6. How can I reduce the odds of a poor fill?

Several things help: use limit orders to control your fill price, avoid entering and exiting at market when liquidity is very thin or the market is moving violently, keep your network stable, and choose a platform that is transparent about execution quality.

Q7. Is ECN always better than a dealing desk?

Not necessarily. ECN emphasises transparent quotes and market matching, while a dealing desk can offer relatively stable quotes—each suits different situations. What really matters is overall execution quality, where the liquidity comes from, and whether the platform's execution is consistently reliable.

8. Conclusion

Order execution is the step that connects placing an order with actually getting filled, and it spans order types, execution methods, and how your platform handles the order. Understanding the differences between market, limit, and stop orders—and the trade-offs between instant and market execution—lets you read your fills far more accurately.

For traders, execution quality shows up directly in costs, in strategy results, and even in mindset. So beyond knowing how execution works, keep an eye on liquidity, volatility, and your platform's execution quality, and use tools such as limit orders and an economic calendar to make better-rounded decisions in any market.

Further Reading

- What Is Slippage?

- What Is a Market Order?

- What Is a Limit Order?

- DD, NDD, STP, and ECN Explained

- What Is Daylight Saving Time?

Titan FX Trading Strategy Lab. We produce investor-education content covering forex, commodities (crude oil, precious metals, agricultural goods), stock indices, US equities, and digital assets.

Primary Sources (by category)

- Regulation & best execution: U.S. Financial Industry Regulatory Authority (FINRA) Rule 5310 — best execution obligations; EU MiFID II — best execution requirements

- Investor education: U.S. Securities and Exchange Commission (SEC) Investor.gov — order types and order handling basics

- Platform & technical documentation: MetaQuotes MT4/MT5 official documentation — order types and execution modes (Instant/Market Execution)