Rebalance / Rebalancing

Investing is not a contest of chasing returns; it is a long game of controlling risk and maintaining discipline. Portfolio rebalancing is one of the most overlooked yet most important practices in that long game.

When market moves push your portfolio away from its target allocation, rebalancing is what restores the original structure and brings the risk profile back into the range you actually want. It helps investors counter market sentiment with discipline, and keeps a portfolio compounding on a stable trajectory.

Whether you are a beginner or a long-horizon investor, understanding what rebalancing is and how to do it well lets you find the real balance between risk and return.

- Rebalancing: A disciplined practice of periodically (or conditionally) adjusting a portfolio so that asset weights return to their original target allocation. The intent is discipline, not market prediction.

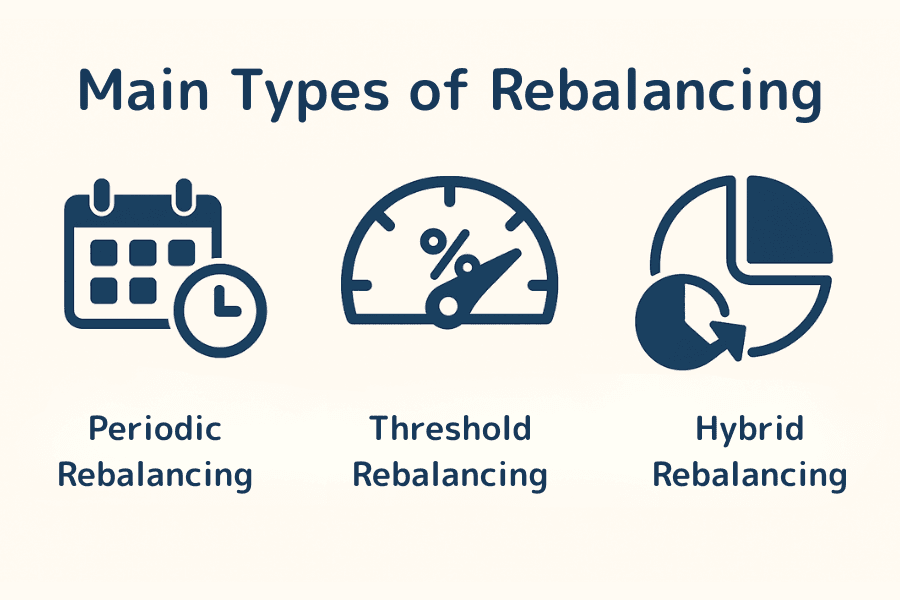

- Three types: Time-based (fixed cadence), Threshold-based (triggered when weights drift beyond ±5–10%), and Hybrid (calendar plus threshold; the standard for most robo-advisors).

- Four reasons it matters: stabilizes risk level, enforces investing discipline, prevents concentration drift, and improves long-horizon risk-adjusted return.

- Three execution paths: manual, automated (via platform / robo-advisor), and cash-flow rebalancing (use new contributions or withdrawals to nudge weights without selling).

- Costs and risks: transaction fees, slippage, and capital-gains tax can erode returns if rebalancing is too frequent. The goal is a dynamic balance between cost control and disciplined execution.

1. What Is Rebalancing?

To understand rebalancing, you first need asset allocation — the foundation of any investment strategy. Asset allocation is the way capital is split across different asset classes (stocks, bonds, cash, commodities) to balance risk and return. The right mix depends on the investor's risk tolerance, goals, and time horizon. A conservative investor may target "40% stocks / 60% bonds," while an aggressive investor may target "70% stocks / 30% bonds."

Portfolio rebalancing means periodically — or under specific conditions — adjusting the portfolio so that the actual weights of each asset class drift back to the original target. For example, if a "60% stocks / 40% bonds" portfolio drifts to "80% stocks / 20% bonds" because of a stock-market rally, rebalancing means selling some stocks and buying some bonds to bring the allocation back to 60:40.

The point of rebalancing is not to predict markets — it is to maintain structural stability through disciplined adjustment. The core objective is to keep the portfolio's risk and return profile consistent with the original plan, no matter what the market does in the short term. In effect, rebalancing converts an "investment plan" into an "execution discipline" so that a strategy can run stably over years.

2. Three Types of Rebalancing

Rebalancing can be categorized by execution timing and trigger condition. The three main types are time-based, threshold-based, and hybrid. Each represents a different trade-off between discipline and responsiveness; choosing the right one depends on the investor's risk tolerance and operating habits.

Type 1: Time-based Rebalancing

Time-based rebalancing emphasizes calendar discipline. The investor sets a fixed interval (quarterly, semi-annually, or annually) and reviews the portfolio at that cadence, restoring the original allocation. The underlying philosophy is "ignore short-term volatility, preserve long-term structure." It is simple, predictable, and low-cost in execution — well-suited to passive investing or retirement plans. The downside is slow reaction to fast-moving markets.

Profile and fit

- ▸ Suited to passive investors using ETFs and index funds

- ▸ Avoids emotional decisions, reinforces discipline

- ▸ Low cost but slow to respond in highly volatile markets

Type 2: Threshold-based Rebalancing

Threshold-based rebalancing is a trigger-driven approach. When an asset class drifts beyond a defined band (for example, ±5% or ±10%) from its target weight, rebalancing is triggered. This makes risk control more responsive to market change. In choppy markets, however, it can produce excessive trading and incremental cost. Most investors use a clearly defined threshold to avoid being triggered too often.

Profile and fit

- ▸ Suited to active investors and those sensitive to market shifts

- ▸ Corrects risk drift in real time, keeps the portfolio stable

- ▸ Watch out for transaction costs and tax friction

Type 3: Hybrid Rebalancing

Hybrid rebalancing combines the best of both. The investor sets a fixed review cadence (quarterly, for instance) but only executes adjustments if weights have drifted past a threshold. This approach pairs discipline with flexibility — it lowers trading frequency while still keeping risk in check. It is the most common rebalancing pattern used by robo-advisors and asset-management platforms.

Profile and fit

- ▸ Suited to long-horizon investors, institutions, and robo-advisor users

- ▸ Balances discipline and flexibility — the dominant style of modern asset management

- ▸ Maintains risk-control efficiency while reducing trading frequency

3. Why Rebalancing Matters

Most market failures come not from bad asset selection but from a lack of long-term discipline and risk control. Rebalancing exists to keep the portfolio on track through volatility, so that short-term price action does not pull a strategy off course.

Reason 1: Keeps Risk Level Stable

Different assets have different volatility characteristics. Without periodic adjustment, weights can drift dramatically and overall portfolio risk can exceed the investor's tolerance. A long stock-market rally, for example, will inflate the portfolio's stock weight and turn a "neutral" allocation aggressive. Rebalancing pulls weights back to the original level so that returns continue to be pursued under the intended risk envelope.

Reason 2: Enforces Investing Discipline

Rebalancing replaces emotion-driven action with a system. Investors tend to feel greedy in rising markets and fearful in falling markets; rebalancing forces "sell-high, buy-low" behavior through a pre-agreed rule. This automated, contrarian mechanism reduces the influence of emotion on decisions and builds discipline over the long run.

Reason 3: Prevents Concentration and Structural Drift

Long market trends gradually unbalance a portfolio. After several years of stock-market gains, equities can grow to dominate, leaving the portfolio dependent on a single market. Rebalancing prevents the "winner-takes-all" expansion, redistributes weights, and keeps the portfolio diversified. For investors aiming at steady long-term returns, this is critical.

Reason 4: Improves Risk-Adjusted Returns

Rebalancing is not about chasing short-term outperformance. By capturing structural price differences across volatile periods, it improves long-horizon risk-adjusted return. In a choppy market, prices oscillate; periodic rebalancing operates as automatic "buy-low, sell-high" within the volatility. In any single year this may not beat the market, but over time it dampens volatility, smooths the return curve, and tends to produce more stable compounding.

4. How to Rebalance in Practice

There is no rigid template for rebalancing. The key is "consistent, repeatable, executable." Different investors choose different methods based on goals, capital size, and operating habits. In practice, three execution paths cover most use cases: manual, automated system, and cash-flow rebalancing.

Method 1: Manual Rebalancing

Manual rebalancing is the most traditional approach: the investor reviews the portfolio personally and adjusts weights. It demands time and planning, but it gives the investor a clear understanding of how the allocation is evolving and how the market is moving.

Steps:- ▸ Step 1: Compute the current market value and actual weight of each asset.

- ▸ Step 2: Compare with the original target weights (e.g., 60% stocks / 40% bonds).

- ▸ Step 3: If drift is large enough, sell the over-weight portion and buy the under-weight portion.

- ▸ Step 4: Evaluate transaction cost and tax impact before executing.

Example: a long-horizon investor sets "60% stocks / 40% bonds." Stock-market gains push the equity weight to 75%. At rebalancing time the investor sells some stocks and buys bonds to restore the target allocation. The method is flexible and gives the investor full control, but it requires time and personal discipline.

Method 2: Automated Rebalancing

Automated rebalancing is executed by an investment platform or robo-advisor based on pre-set rules. The investor sets initial weights and a tolerance band, and the system tracks drift and rebalances automatically when the band is breached.

Example: a robo-advisor user targets "70% stocks / 30% bonds" with a ±5% tolerance. When stocks rise to 75%, the system automatically sells some stocks and buys bonds to restore the target. The benefits are disciplined execution and time savings, especially for passive investors holding long-term ETF portfolios. The trade-offs: less control over execution, and some platforms charge an extra management fee.

Method 3: Cash-flow Rebalancing

Cash-flow rebalancing avoids buying and selling existing holdings. Instead, it uses new contributions or withdrawals to nudge the portfolio toward target weights. This pattern is extremely common in long-horizon dollar-cost-averaging and retirement plans, because it preserves the allocation structure without generating extra trading cost.

In practice: when new money comes in, allocate it to the asset class currently under-weight. When money needs to come out, take it from the over-weight asset class first. For example, an investor making monthly contributions notices their bond weight is below target and routes the next month's contribution mainly into bonds. This method is gentle, efficient, and especially well-suited to long-term saving and accumulation strategies.

Frequency and Timing

There is no universal answer to rebalancing frequency, but consistency matters more than the cadence itself. Research shows that rebalancing too often increases trading cost, while rebalancing too rarely lets risk drift out of control. The two common conventions are:

- Time-based: A fixed interval such as semi-annually or annually — emphasizes discipline and long-term stability.

- Threshold-based: Triggered when weights drift past a defined band (e.g., ±5%) — emphasizes responsive risk control.

Whichever method you pick, what matters is sticking to it. As long as the rule is followed consistently, rebalancing will deliver its core benefits: stable investing and risk control over time.

5. Cost and Risk Considerations

Rebalancing keeps allocation structure stable, but execution is not free. Ignoring cost and execution risk can shrink returns or amplify volatility. Any rebalancing design needs to account for both transaction cost and operational risk.

Cost Side: Trading and Tax

Rebalancing involves buying and selling, which inevitably brings fees and tax consequences.

- ▸ Fees and slippage: In volatile or low-liquidity markets, the bid-ask spread (slippage) widens, and frequent rebalancing accumulates meaningful cost.

- ▸ Tax impact: Selling appreciated assets in a taxable account triggers capital-gains tax. Estimate the tax bill before executing.

To reduce cost, lengthen the cycle, use cash-flow rebalancing, or pick a low-cost platform.

Risk Side: Timing and Market Conditions

Bad timing can turn rebalancing itself into a risk.

- ▸ Selling too early: Selling into a still-running uptrend can cost upside.

- ▸ Over-rebalancing: Constant chasing and counter-trading can erode returns.

- ▸ Liquidity risk: Bonds, foreign ETFs, and small-cap stocks can be thin during certain hours; adjustments are harder and more expensive.

The ideal rebalancing strategy does not aim for perfection — it aims for a dynamic balance between cost control and risk preservation. Disciplined adjustment under reasonable cost is what lets rebalancing actually deliver stable long-term returns.

6. Frequently Asked Questions

Q1: How often should rebalancing be done?

There is no single answer, but in practice "semi-annually" or "annually" is the most common time-based cadence. More active investors use a threshold-based approach, triggered when an asset class drifts ±5% to ±10% from target. Research shows over-frequent rebalancing inflates costs, while infrequent rebalancing lets risk run. A hybrid of calendar plus threshold is the most common approach in modern asset management.

Q2: Does rebalancing increase trading cost?

Yes. Each rebalance involves buying and selling, so it incurs commissions, spreads, and potentially tax. In a taxable account, selling appreciated assets triggers capital-gains tax. Cost-reduction levers include: lengthening the cycle, using cash-flow rebalancing (route new contributions to under-weight assets), and choosing low-cost ETFs and platforms.

Q3: How is rebalancing different from market timing?

Rebalancing is a "rule-based discipline" — execute mechanically against a pre-agreed target weight. Market timing is a "subjective market call" — try to predict highs and lows and trade them. Rebalancing does not require market prediction; it just maintains risk level through automated "sell-high, buy-low." Over the long run, disciplined rebalancing tends to be more predictable and more stable than market timing.

Q4: Are rebalancing strategies different in retirement vs taxable accounts?

Yes. Tax-deferred retirement accounts generally do not trigger immediate taxes when you rebalance — frequency can be higher. Taxable accounts need to consider capital-gains tax, so cash-flow rebalancing (adjusting via new contributions) is preferred to avoid realizing gains. Long-horizon investors often place "tax-sensitive positions" in taxable accounts and "frequent-rebalancing positions" in retirement accounts.

Q5: Can ETFs / robo-advisors rebalance automatically?

Yes. Most robo-advisors (Robo-advisor) execute rebalancing automatically — the user sets initial weights and a tolerance band (for example, ±5%). Some target-date funds (Target-date Funds) also include built-in rebalancing that gradually reduces stock weight as the investor approaches retirement. For investors who do not want to manage allocations manually, this dramatically lowers the operational barrier.

7. Summary: Rebalancing as Discipline

Rebalancing is not a sophisticated mathematical model, and it is not a high-return technique. It is an action framework for maintaining direction through volatility and controlling risk over the long run.

Most investors lose to emotion, not to stock-picking. When markets rise, greed pulls the allocation away from plan; when markets fall, fear pushes investors into bad exits. Rebalancing matters most in exactly those moments — it provides a disciplined rail so you keep moving with the plan even when the market is uncertain.

The key to making rebalancing work is not the frequency of adjustment but consistency of execution. Whether you use a semi-annual time-based schedule or a threshold-triggered approach, sticking to the rule over the long term is what turns market volatility from a threat into a tailwind.

Investing success is not about who predicts most accurately — it is about who stays disciplined the longest. Make rebalancing a core habit of your investment plan, because what really delivers stable returns over time is not luck, it is discipline.

Further Reading

- What Is the Sharpe Ratio?

- What Is Volatility?

- What Is Slippage?

- What Is a Stop-Loss?

- What Is a CFD?

- Forex Trading Basics

- What Is Leverage?

Titan FX Research. Investor-education content covering forex (FX), commodities (oil, precious metals, agricultural products), stock indices, US equities, and crypto assets across global markets.

Primary Sources by Category

- Theoretical origin: Markowitz, H. M. (1952) "Portfolio Selection," Journal of Finance; Modern Portfolio Theory (MPT) foundation

- Empirical research: Vanguard "Best Practices for Portfolio Rebalancing" (2010, 2015 update); Plaxco, L. M. & Arnott, R. D. "Rebalancing a Global Policy Benchmark" (2002)

- Tax strategy: Bogleheads.org "Asset Location" guide; Israelsen, C. L. 7Twelve: A Diversified Investment Portfolio with a Plan

- Robo-advisors: Betterment / Wealthfront official white papers; robo-advisor performance tracking research