TIBOR

TIBOR (Tokyo Interbank Offered Rate) is a vital benchmark reflecting interest rates in Japan’s interbank market, widely used in pricing financial products and corporate loans.

This article explores TIBOR’s definition, functions, calculation, and publication methods, while comparing it to other rate benchmarks, offering a comprehensive guide to this key financial tool.

- TIBOR (Tokyo Interbank Offered Rate) definition and role in Japan's financial market

- JPY TIBOR vs Euroyen TIBOR; five tenors (1W to 12M)

- Calculation process: reference panel, trimmed mean, daily 11 AM publication

- TIBOR's impact on Japanese mortgage rates, corporate loans, and swaps

- LIBOR retirement and TIBOR's continued role alongside TONA transition

1. What Is TIBOR?

TIBOR, published daily by the Japanese Bankers Association (JBA), is a reference rate that reflects borrowing costs in Tokyo’s interbank market.

It serves as a key indicator for Japan’s short-term financial markets and is closely tied to the Bank of Japan’s (BOJ) policy rates, such as the unsecured overnight call rate.

Since November 1995, the JBA has calculated and released Yen TIBOR. In March 1998, Euroyen TIBOR was introduced to enhance transparency and growth in Japan’s short-term financial markets.

2. Types and Functions of TIBOR

TIBOR comes in two forms and plays a critical role in financial markets, influencing corporate loans, financial product pricing, and market liquidity. Here’s a breakdown of its types and purposes.

2.1. Types of TIBOR

Yen TIBOR

Yen TIBOR reflects actual rates in Japan’s domestic unsecured call market, measuring the cost of short-term interbank lending.

It uses an ACT/365 basis (actual days/365) for interest calculations, assuming a 365-day year. Due to its strong link to the BOJ’s policy rate, it’s considered a core indicator of domestic funding costs, impacting corporate loans and market operations.

Euroyen TIBOR

Euroyen TIBOR represents rates in Japan’s offshore market, where banks outside Japan lend in yen.

It’s calculated on an ACT/360 basis (actual days/360), differing from Yen TIBOR. The offshore market operates beyond direct Japanese regulatory oversight, so its rates may diverge from domestic trends.

Note: Euroyen TIBOR is unrelated to the euro (EUR); “Euro” refers to offshore yen transactions. This benchmark ceased publication on December 30, 2024.

2.2. Functions of TIBOR

Benchmark for Corporate Loan Rates

TIBOR serves as a base rate for corporate loans, often calculated as TIBOR + a fixed spread. For example, if TIBOR is 1% and the bank’s spread is 0.5%, the loan rate becomes 1.5%.

When the BOJ adjusts monetary policy, TIBOR fluctuates accordingly, affecting borrowing costs. A policy rate hike raises TIBOR, increasing loan expenses and potentially influencing corporate investment decisions.

Pricing Financial Products

TIBOR is a key reference rate in financial markets, applied to products like:

- TIBOR Swaps: Agreements to swap fixed rates for TIBOR-based floating rates, used to hedge interest rate risks and reduce uncertainty from market fluctuations.

- Bonds and Notes: Short-term bonds, commercial paper (CP), and other fixed-income securities often use TIBOR as a pricing benchmark.

Indicator of Market Liquidity

TIBOR’s movements mirror supply and demand in the interbank market. Abundant liquidity lowers borrowing demand, reducing TIBOR; tight conditions push it higher, signaling rising funding costs.

This makes TIBOR a gauge of financial market liquidity and risk sentiment, especially during economic turbulence or crises, when sharp rises may indicate reduced lending willingness among banks.

3. How TIBOR Is Calculated and Published

3.1. Calculation Method

TIBOR is computed by the JBA TIBOR Administration (JBATA) through this process:

① Rate Submissions

Fifteen selected reference banks submit their daily lending rates by 11:00 AM JST (10:00 PM EST the previous day).

② Outlier Removal

The highest and lowest two rates are discarded.

③ Averaging

The remaining rates are averaged to determine that day’s TIBOR.

TIBOR covers multiple tenors: 1 week, 1 month, 3 months, 6 months, and 12 months.

3.2. Publication Method

Timing: Released by authorized providers before 1:00 PM JST daily (12:00 AM EST).

Channels: Available via Bloomberg, Reuters, and updated on the JBATA website (typically after 3:30 AM EST).

Fallback: In case of system failures or market disruptions, the prior day’s rate is used per the “TIBOR Contingency Plan.”

Source: JBA TIBOR Administration website (www.jbatibor.or.jp).

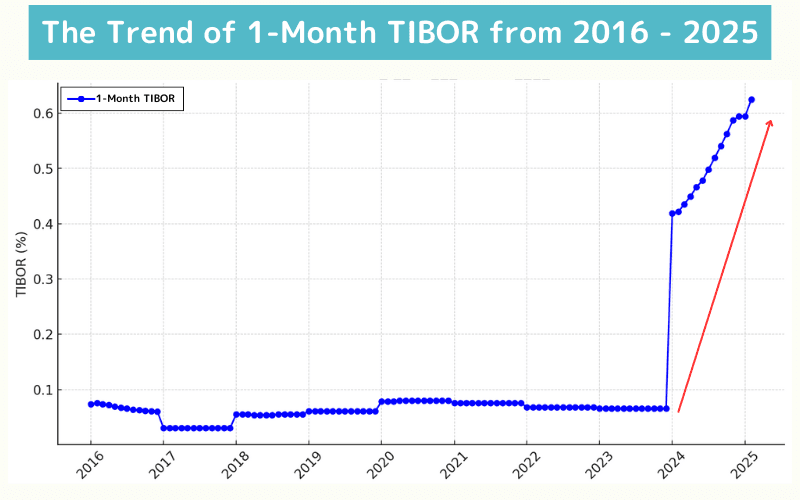

4. Trends in TIBOR

Yen TIBOR varies by tenor—1 week, 1 month, 3 months, 6 months, and 12 months—with the 1-month TIBOR being a widely watched benchmark.

From 2016 to early 2024, 1-month TIBOR remained below 0.1%, reflecting Japan’s prolonged low-rate environment. Since 2024, it has risen noticeably, driven by shifts in funding costs and monetary policy adjustments.

Data Source: JBA TIBOR Administration website

The BOJ’s policy rate (unsecured overnight call rate) shows a similar pattern. Both TIBOR and the policy rate were stable until early 2024, then rose together, highlighting their close correlation. This suggests TIBOR is influenced by both market dynamics and BOJ policy shifts.

Post-2024, TIBOR’s uptrend may signal a repricing of interest rate expectations, with implications for corporate borrowing and market funding costs worth monitoring.

5. TIBOR FAQs

Q1: Where Can I Check TIBOR Rates?

Latest and historical data are available on the JBA TIBOR Administration website (www.jbatibor.or.jp).

Q2: How Does TIBOR Differ from LIBOR?

| Benchmark | Scope | Status/End Date | Administrator |

|---|---|---|---|

| LIBOR | London market, multi-currency (USD, EUR, JPY, etc.) | Mostly ceased Dec 31, 2021 | UK FCA |

| TIBOR | Tokyo market, yen-focused (Euroyen TIBOR ended Dec 2024) | Ongoing (Yen TIBOR) | JBA (JBATA) |

| Key Differences | Geography (global vs. Japan), currency (multi vs. yen) | End dates differ (LIBOR phased out, TIBOR partially persists) | Oversight (UK vs. Japan) |

Q3: Can TIBOR Go Negative?

Yes. From 2018, 1-week TIBOR occasionally dipped below zero, reflecting excess liquidity and low rates. This has lessened since the 2024 policy rate hike.

Q4: Why Was Euroyen TIBOR Discontinued?

Declining offshore market activity and global benchmark reforms led the JBA to terminate Euroyen TIBOR on December 31, 2024, shifting to more representative alternatives.

Q5: Why should retail investors track TIBOR?

For multiple practical reasons:

- Mortgage borrowers on floating rates monitor TIBOR for refinancing timing

- Bond, REIT, and dividend-stock investors care about rate sensitivity

- Forex traders watch JPY rate differentials versus other major currencies

- Market participants infer BOJ policy stance from TIBOR dynamics around policy meetings

Tracking TIBOR's movement relative to consensus expectations often surfaces investment opportunities ahead of broader market recognition.

6. Summary

TIBOR (Tokyo Interbank Offered Rate) is a critical measure of funding costs in Japan’s interbank market, split into Yen TIBOR and the now-discontinued Euroyen TIBOR.

It underpins corporate loan rates and financial product pricing, closely tracking the BOJ’s policy rate.

Calculated and published daily by the JBA TIBOR Administration, TIBOR offers reference rates across tenors from 1 week to 12 months.

With Japan’s monetary policy shifting in 2024, TIBOR’s upward trend signals changing market dynamics—track it via the official website or financial platforms to stay informed.

Further Reading

- Policy Interest Rate

- Open Market Operations (OMO)

- Quantitative Easing (QE)

- CPI (Consumer Price Index)

Titan FX Research Team. We cover a broad set of financial instruments — foreign exchange, commodities, equity indices, US equities, and digital assets — producing practical, research-backed educational content for investors.

Primary Sources

- TIBOR operations: Japanese Bankers Association TIBOR, QUICK Benchmarks

- BOJ monetary policy: Bank of Japan — Monetary Policy, BOJ Time-Series Data

- LIBOR transition: FCA LIBOR Transition, ARRC SOFR