Gotobi (Five-Ten Days)

If you watch JPY currency pairs closely, you may notice a recurring pattern: predictable bursts of flow on specific days each month, concentrated in particular Tokyo morning hours. This pattern has a name — Gotobi (五十日) — and it traces back to long-standing Japanese corporate settlement conventions. This article walks through what Gotobi means culturally, how it shows up in the FX market, and the short-term trading strategy around the 9:55 JST Nakane (TTM) fixing window.

- What "Gotobi" is: Days ending in 5 and 0 (5th, 10th, 15th, 20th, 25th, 30th). Traditional settlement and payment dates for Japanese corporates, creating an observable intra-month flow pattern.

- Why it matters: Salary transfers, import payments, and trade settlements cluster on these days. JPY demand in early Tokyo hours expands sharply, often producing directional moves in USD/JPY and JPY crosses.

- The Nakane (9:55 JST) effect: Banks must clear client FX orders against the daily TTM fix. This typically drives concentrated USD buying between 8:00 and 8:55 JST, then a fade or reversal once the fix prints.

- Not a silver bullet: Macro events, risk-off sentiment, and technical levels can override the pattern. Treat Gotobi as a "flow context overlay," not a standalone signal — combine with technicals and fundamentals.

- Practical execution: Strict stops, avoid chasing into 8:55, expect amplified moves when Gotobi coincides with month-end or quarter-end, prioritize liquidity nodes in JPY crosses.

1. What Is Gotobi (Five-Ten Days)?

Gotobi (五十日) refers to days of the month ending in 5 or 0 — the 5th, 10th, 15th, 20th, 25th, and 30th. In Japan, these dates are recognized as settlement and commercial peak days, marked by concentrated payment flow and trading activity.

These dates look ordinary on a calendar, but they carry real weight in Japanese business and financial markets. Corporate payments, interbank transfers, and even retail foot traffic show measurable patterns on Gotobi days.

While the concept is rooted in business custom rather than law, the cumulative effect of so many institutions following the same rhythm is what makes it tradeable as a flow pattern.

2. Gotobi and Japanese Business Culture

Gotobi matters because it reflects the long-standing operational rhythm of Japanese corporations and financial institutions. Many firms structure payroll, vendor payments, and accounts settlement around these dates, and the practice has become deeply embedded.

This periodic structure makes Gotobi a concentration point for fund movement. Banks and financial institutions ramp up cash-management and reconciliation work on these days, leading to noticeably elevated funding demand and FX volume.

Logistics activity and consumer footfall also pick up. Taken together, Gotobi has become woven into the operational cadence of Japanese society — and that systemic regularity is exactly what makes it observable in market data.

3. The "Gotobi Effect" in Financial Markets

Because Gotobi is a high-frequency settlement and treasury-operations day for Japanese corporates and banks, it produces a clear "Gotobi effect" in financial markets.

The foreign exchange market is particularly responsive. JPY currency pairs often see higher volume and amplified short-term volatility on Gotobi.

A common scenario: banks and corporates execute large FX settlements on these days, converting foreign currency into yen to pay salaries, invoices, or overseas creditors — which can push yen-strength flow in the morning Tokyo session.

When Gotobi coincides with month-end or quarter-end, the picture intensifies further: capital reflows, portfolio rebalances, and hedging activity can widen the moves.

For short-term traders and FX participants, Gotobi serves as a useful window for observing flow concentration and short-horizon price behavior. Combining technical analysis with fundamental context gives traders a sharper read on potential entry and exit opportunities.

4. How Should Traders Respond?

Gotobi originates as a commercial convention, but for FX and financial-instrument traders it functions as a valuable reference for tracking market flow. Understanding the potential impact of these dates helps maintain composure and adjust strategy when short-term volatility hits.

In practice, watch JPY-related pairs — USD/JPY, EUR/JPY, AUD/JPY — during the Tokyo session (Japan time 9:00–noon). Unusual price moves or volume spikes in this window often trace back to corporate settlements or financial-institution treasury operations.

When Gotobi falls just before or after month-end, quarter-end, or major holidays (Golden Week, year-end), liquidity changes and the volatility envelope can both expand meaningfully.

In those situations, setting prudent stops and profit targets — and avoiding excessive leverage — is the basic discipline for managing risk.

In short, treating Gotobi as a "liquidity node" and combining it with technicals and news flow can sharpen execution and reduce exposure to unexpected moves.

Further reading: Best FX Trading Hours: Tokyo, London, and New York Sessions

5. The Gotobi × Nakane Trade: Reading 8:00–8:55 JST Flow

On Gotobi days, one classic short-term strategy is built around the flow that occurs just before the 9:55 JST Nakane fix (TTM — Telegraphic Transfer Middle Rate), the daily reference rate banks publish for customer FX settlement.

Because Japanese corporates schedule overseas payments and FX conversions on Gotobi, the resulting USD-buying tends to concentrate in the morning session — supporting USD/JPY into the fix.

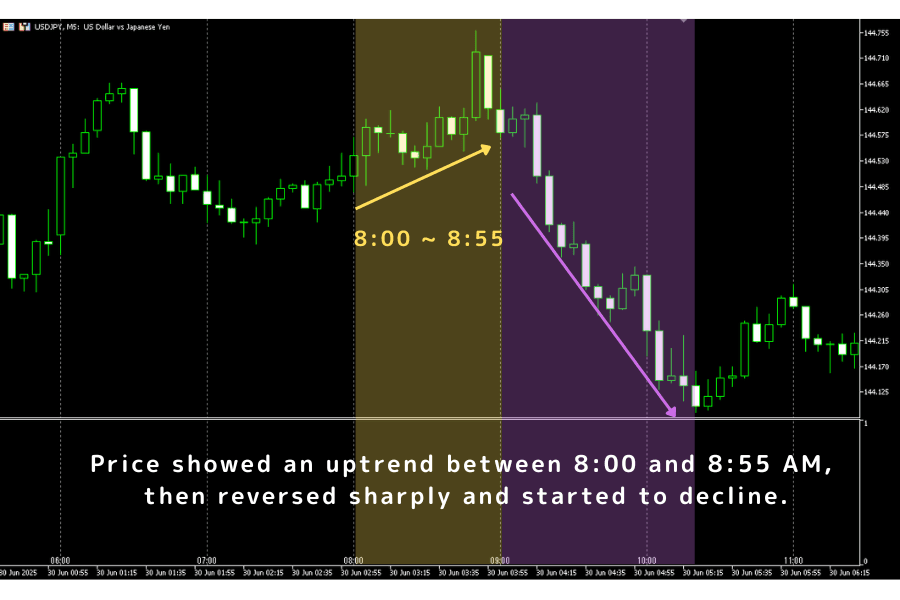

Traders typically focus on USD/JPY between 8:00 and 8:55 JST.

During this window, many Japanese corporates and financial institutions execute cash-management activity, lifting USD demand and often producing a short-term USD/JPY uptrend.

Historical observation of Gotobi sessions suggests that USD/JPY tends to grind higher from 8:00, peak near the 9:55 fix, and then either consolidate or reverse. This price action is a common reference for intraday traders building short-term setups.

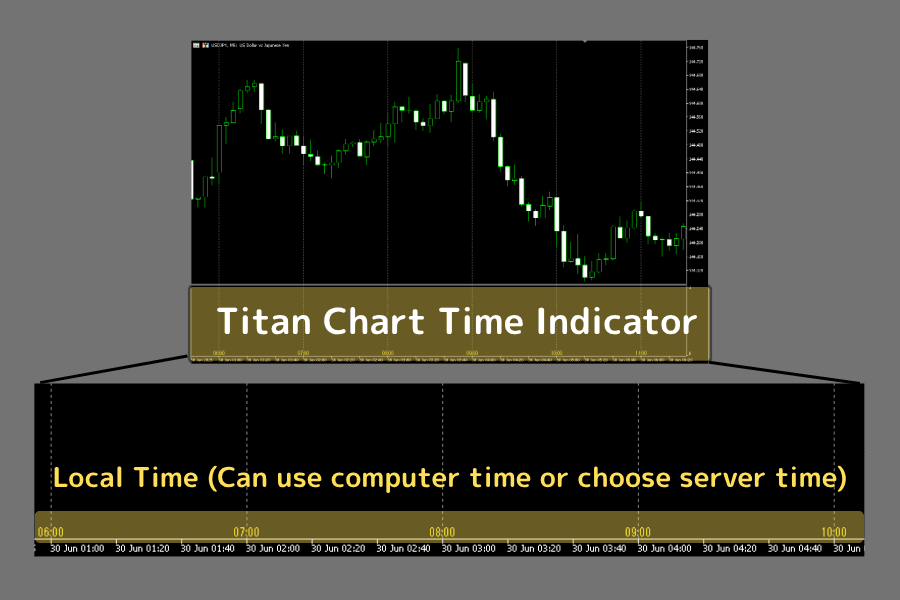

The chart timeline above has been adjusted using Titan FX's Titan Chart Time indicator, which displays local time (Japan time, Hong Kong time, etc.) directly on the chart — no manual conversion from the platform's server time required. This significantly improves analysis speed and accuracy.

To try this tool, you can download it for free:

It's worth emphasizing that not every Gotobi produces obvious USD buying. When the market is constrained by macro news, risk-off sentiment, or technical resistance, price action can run counter to the historical pattern — sometimes fading early, drifting sideways, or producing false breakouts. Caution remains essential.

Practical considerations when using this strategy:

- Confirm that the day's sentiment and technicals support a short-term long bias

- Combine with short moving averages, candlestick patterns, and support/resistance levels

- Set strict stop-losses to manage the risk of fast reversals

- Avoid chasing into 8:55 — price often reverses quickly after the Nakane fix prints

Reading the "Gotobi × Nakane" rhythm gives traders an edge in capturing intraday opportunities, especially in the early Asian session.

That said, this is a day-trading technique. It needs to be combined with market judgment and risk management — and never relied on as a rigid, mechanical pattern.

6. Frequently Asked Questions (FAQ)

Q1. Is Gotobi a recurring "regular event" every single month?

Gotobi is a settlement convention, not a legally mandated market event. Most Japanese corporates and banks follow this rhythm, but not every Gotobi produces a clear JPY move. Empirically, end-of-month days (especially the 30th) and end-of-quarter Gotobis (March, June, September, December) tend to show stronger effects than the 5th, 10th, 15th, 20th, and 25th of an ordinary month. The right framing: a higher-probability observation window, not a guaranteed pattern.

Q2. Can the Gotobi strategy only be applied to USD/JPY? What about other pairs?

USD/JPY is the most direct candidate because Japanese corporate FX settlement is overwhelmingly USD-denominated. That said, EUR/JPY, AUD/JPY, GBP/JPY and other JPY crosses also show same-direction flow — though liquidity and signal strength diminish. Beginners should anchor on USD/JPY; on crosses, watch for wider spreads and higher volatility.

Q3. Why does the market often reverse after the Nakane fix (9:55 JST)?

The Nakane is the reference settlement rate banks use for client FX orders. In the run-up (8:00–8:55), banks buy USD into the fix to cover those orders, lifting USD/JPY. Once the fix prints, the forced buying disappears and profit-taking plus arbitrage unwinds flow into the market — producing the classic "peak at the fix, fade afterwards" pattern (known in the trade as the "Nakane-Goto bottom"). This is the central reason the strategy explicitly avoids chasing into 8:55.

Q4. Asian-session liquidity is relatively thin. Is the Gotobi strategy high-risk?

Asian-session liquidity is genuinely lower than London or New York, which means wider spreads and higher slippage probability. The Gotobi strategy tries to extract short-term moves from "relatively thin liquidity + concentrated buying," so the main risks are: (a) breaking news that disrupts the flow rhythm; (b) sharp reversals immediately after the fix; and (c) extended counter-trend moves when the higher-time-frame trend is against the entry. Position sizing, strict stops, and avoiding entries around major data releases are the baseline disciplines.

Q5. Will the Gotobi effect fade as electronic trading and globalization advance?

The underlying Japanese corporate settlement conventions are still in place (payroll days and month-end cutoffs are baked into HR and accounting systems), so the structural driver of the flow remains. But the spread of FX algorithmic trading and the CLS (Continuous Linked Settlement) real-time settlement system has measurably shrunk the "first-mover edge" of predictable liquidity nodes. Over the long arc, the Gotobi effect is weaker than a decade ago — but on month-end, quarter-end, and year-end specific nodes it still carries meaningful reference value.

7. Conclusion

Gotobi is the everyday settlement day of Japanese corporates and banks, and it tends to surface as concentrated flow and short-term volatility in the FX market. For traders — particularly those active in the early Tokyo session — understanding the rhythm around Gotobi and the lead-up to the Nakane fix helps surface intraday opportunities.

The pattern doesn't print every time. But combined with careful observation, validation, and disciplined risk control, Gotobi remains a useful flow overlay within a broader trading strategy.

Titan FX Live RatesFurther Reading

- Best FX Trading Hours: Tokyo, London, and New York Sessions

- Forex Trading Basics: Margin, Pips, and Order Flow

- Japanese Yen (JPY): Fundamentals and FX Market Characteristics

- Global Major Central Banks (Fed, ECB, BOJ, PBOC, BOE) Overview

- Day Trading: Foundations and Risk Management

- Candlestick Chart Patterns: A Technical Analysis Primer

- Titan Chart Time Indicator: Local Time Display for MT4/MT5

Titan FX Financial Markets Research & Review Team. We cover forex (FX), commodities (crude oil, precious metals, agricultural products), stock indices, U.S. equities, and crypto assets, producing educational content for investors across asset classes.

Primary Sources (by Category)

- Official data: Bank of Japan (BOJ) Financial Markets Department public data, Tokyo Foreign Exchange Market Committee Operating Manual, CLS Group Settlement Data.

- Market data: Bloomberg FX Volume Heatmap, Reuters FX Tokyo Session Report, CFTC Commitments of Traders Report (JPY).

- Academic research: Takatoshi Ito and Yuko Hashimoto, "Microstructure of the Yen FX Market"; Yin-Wong Cheung, "Yen Behavior on Major Settlement Days"; Bank for International Settlements (BIS), "Triennial Central Bank Survey of FX Markets."

- Industry and third-party references: Investopedia (Tokyo Session), OANDA / Refinitiv FX Tokyo Session Guides, Titan FX Research economic calendar, Nikkei FX commentary.