Lehman Brothers Crisis

With over $600 billion in liabilities, it remains the largest bankruptcy filing in U.S. history. What makes Lehman's downfall a watershed is how quickly extreme leverage, liquidity mismatches, and the "too big to fail" assumption toppled a storied Wall Street bank in a matter of days — making it the defining inflection point of the 2008 Global Financial Crisis and a textbook example of a Black Swan Event.

This article explains what the Lehman Brothers Crisis was, the bank's rise and fall, the five causes of its collapse, its global impact, the post-crisis regulatory reforms, and what the Global Financial Crisis means for individual traders.

- Date: 15 September 2008. Lehman files Chapter 11 with $600B+ liabilities — the largest U.S. bankruptcy on record.

- Root causes: heavy subprime exposure, leverage ratios above 30:1, severe underestimation of liquidity risk, misreading of government willingness to bail out, and total loss of market confidence.

- Global impact: Dow dropped 500+ points in one day; interbank credit froze; the world entered the 2008–09 Great Recession.

- U.S. response: TARP (~$700B), Federal Reserve emergency near-zero rates, quantitative easing, and the Dodd-Frank Act (2010).

- Key lesson: "Too Big to Fail" was no longer absolute — regulation, leverage discipline, and orderly resolution became central pillars of the post-crisis financial system.

1. What was the Lehman Brothers Crisis?

The Lehman Brothers Crisis is the 15 September 2008 bankruptcy filing of Lehman Brothers Holdings, the fourth-largest U.S. investment bank at the time. Total liabilities exceeded $600 billion — the largest Chapter 11 filing in U.S. history.

The "2008 Global Financial Crisis" (GFC) commonly refers to the system-wide crisis that Lehman's collapse set off around the world; the Lehman Brothers Crisis was its single most emblematic trigger. This article focuses on that trigger — the Lehman failure itself — while the broader causes and spread of the crisis are covered in our Financial Crisis explainer.

2. The Rise and Fall of Lehman Brothers

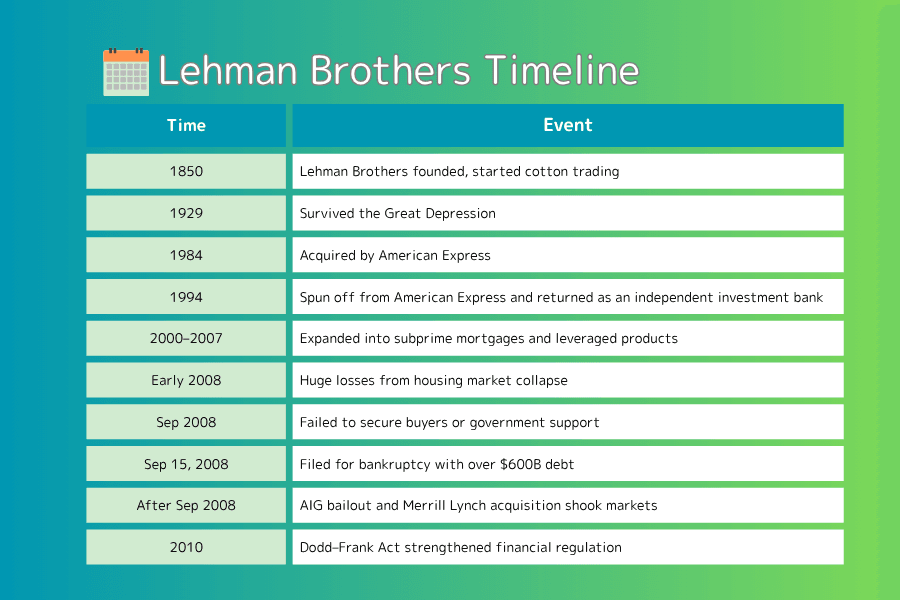

Lehman Brothers was founded in 1850 by German immigrant Henry Lehman as a small cotton-trading shop in Montgomery, Alabama. After his brothers joined, the family expanded from commodity trading into financial services — particularly financing for Southern cotton farmers.

After the Civil War, Lehman moved to New York and grew into a major Wall Street investment bank, underwriting railroads, utilities, and other large industrial offerings. By the 20th century, Lehman was one of the most prominent names in American finance.

Lehman survived earlier shocks: it weathered the 1929 Great Depression, was acquired by American Express in 1984 (temporarily losing its independence), then spun back out and went public in 1994.

In the 2000s, Lehman expanded aggressively into real estate and structured finance. By 2007 it was the fourth-largest investment bank globally — behind Goldman Sachs, Morgan Stanley, and Merrill Lynch — and held an outsized share of mortgage-backed securitization.

Lehman's history was once described as a "nine-lives cat" because of its repeated comebacks. The subprime collapse ended that streak.

3. Five Causes of the Crisis

Cause 1: Heavy Subprime Mortgage Exposure

In the 2000s, U.S. home prices soared and subprime lending standards collapsed. Lehman aggressively originated mortgages, bought subprime loan portfolios from other lenders, and packaged them into MBS (Mortgage-Backed Securities) and CDO (Collateralized Debt Obligations) sold worldwide.

These products appeared diversified, but they were highly dependent on continued home-price appreciation. Once prices fell, the entire stack collapsed in value.

Cause 2: Extreme Leverage

Lehman's leverage ratio peaked above 30:1, meaning a 3–4% loss could push the firm into technical insolvency. Its short-term funding relied heavily on repo markets, which evaporate at the first sign of distress. Confidence loss = funding loss.

Cause 3: Severe Underestimation of Liquidity Risk

Lehman held large positions in illiquid assets. When markets stopped bidding for those assets during the panic, the firm had no time to liquidate, and its short-term funding ran dry within days.

Cause 4: Misreading Government Willingness to Bail Out

Lehman expected a Bear Stearns-style or AIG-style government rescue. The U.S. Treasury and Federal Reserve ultimately declined, and Lehman was allowed to fail. Subsequent academic analysis concluded that Lehman over-relied on the implicit assumption that "the government won't let us fail" — and seriously misread the political and financial calculus.

Cause 5: Total Collapse of Market Confidence

Successive credit-rating downgrades in 2008 panicked investors. Customers withdrew funds, counterparties cut off trading, and Lehman's funding chain snapped within days. By the time the bankruptcy filing was made, no rescue could be arranged.

4. Global Impact

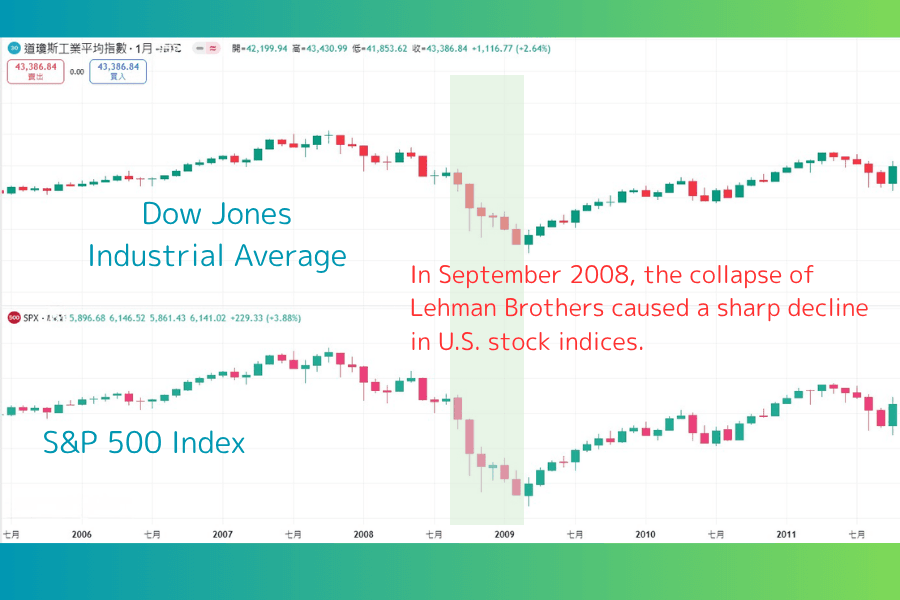

Impact 1: Worldwide Market Crash

The Dow dropped over 500 points in a single day after the filing, and global indices followed. Trust between banks, insurers, and investment institutions collapsed; capital markets effectively seized up.

Impact 2: Credit Market Freeze

Interbank lending stopped. Solvent corporations couldn't roll short-term funding. Healthy companies were dragged into cash-flow crises, and the freeze spread far beyond the financial sector.

Impact 3: Mass Asset Destruction

Equities, real estate, and commodities all crashed simultaneously, destroying personal and institutional wealth. Pension funds, insurers, and household balance sheets took severe hits, and consumer sentiment collapsed.

Impact 4: Global Recession

The shock waves reached Europe, Japan, China, and emerging markets quickly. Growth slowed and unemployment soared, producing the 2008–2009 Great Recession.

Impact 5: Wall Street Reshuffling

Merrill Lynch was rapidly absorbed by Bank of America, AIG received an emergency government rescue, and Goldman Sachs and Morgan Stanley converted to bank holding companies. Wall Street's structure changed permanently.

5. Post-Crisis Reforms

Reform 1: TARP

The U.S. Treasury launched the Troubled Asset Relief Program (TARP) with roughly $700 billion to purchase troubled assets and inject capital into banks, preventing a system-wide collapse.

Reform 2: Federal Reserve Emergency Policy

The Federal Reserve cut rates to near zero — historically low — and launched Quantitative Easing (QE), buying Treasuries and mortgage-backed securities at scale to keep liquidity flowing.

Reform 3: Dodd-Frank Act (2010)

The U.S. enacted the Dodd-Frank Wall Street Reform and Consumer Protection Act in 2010, the most comprehensive financial-regulatory reform since the Great Depression. Key provisions:

- Caps on financial-institution leverage

- Stronger bank capital requirements

- Establishment of the Financial Stability Oversight Council (FSOC)

- Clearer government authority to wind down failing financial firms

Reform 4: Rethinking "Too Big to Fail"

Lehman demonstrated that systemically important firms can collapse. Markets began pricing in tail-risk for large institutions, and governments built Orderly Liquidation Authority to avoid sudden chaotic failures.

Reform 5: Bank Risk-Management Overhaul

Global banks shifted toward stronger liquidity, credit, and capital management. Reliance on complex derivatives was reduced. Leverage ratios came down across the industry, and balance sheets became more conservative.

6. Frequently Asked Questions About the Lehman Crisis

Q1: When and why did the Lehman Brothers Crisis happen?

On 15 September 2008, Lehman Brothers Holdings — the fourth-largest U.S. investment bank — filed for Chapter 11 bankruptcy. The proximate causes were heavy subprime mortgage exposure, leverage above 30:1, severe underestimation of liquidity risk, a misread of government willingness to bail out, and a complete loss of market confidence.

Q2: Why was Lehman not bailed out like Bear Stearns or AIG?

Bear Stearns and AIG received government rescues, but the U.S. Treasury and Federal Reserve declined to do the same for Lehman. Reasons included moral-hazard concerns, insufficient collateral, and political pressure. Lehman itself had over-relied on the implicit assumption that the government would not let it fail.

Q3: What was TARP?

The Troubled Asset Relief Program — a roughly $700 billion U.S. government program after Lehman's collapse to purchase toxic assets and inject capital into banks. It is one of the largest peacetime government interventions in financial markets in history.

Q4: What did the Dodd-Frank Act change?

The 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act is the most comprehensive financial-regulatory reform since the Great Depression. Key provisions: caps on financial-institution leverage, stronger bank capital requirements, establishment of the Financial Stability Oversight Council (FSOC), and clearer government authority to wind down failing financial firms.

Q5: How did Lehman affect Asian markets?

Japan's Nikkei 225 fell from a 12 September 2008 close of 12,214 to briefly under 7,000 by 28 October 2008 — about a 43% decline in roughly six weeks. The yen also strengthened sharply on risk-off flows, hurting Japanese exporters' earnings outlook. China and other Asian markets saw parallel sharp declines and growth slowdowns.

Q6: Is the Lehman Brothers Crisis the same as the Global Financial Crisis?

Not exactly. The "Global Financial Crisis (GFC)" refers to the entire system-wide crisis that spread across the world in 2008, while the "Lehman Brothers Crisis" was the trigger that defined it. Lehman's 15 September 2008 bankruptcy escalated the subprime crisis into a full global crisis within days. For the broader causes and spread, see our Subprime Mortgage Crisis explainer; this article focuses on the trigger itself.

7. Conclusion and Takeaways

Lehman Brothers' failure was not just one bank's bankruptcy — it was a system-wide alarm bell. The crisis exposed structural weaknesses: extreme leverage, opaque structured products, lax credit underwriting, and over-reliance on implicit government backstops.

What the crisis taught us:- Financial institutions can't pursue short-term profit while ignoring tail risk.

- Investors must not blindly trust rating agencies or market optimism.

- Regulators must balance market freedom with financial-stability mechanisms — including effective oversight and credible resolution authority.

For individual traders and investors, the operational lesson is preparedness. Use stop losses on every trade, size positions conservatively (the 2% rule is a sensible default), and understand volatility regimes. The next Black Swan Event will not announce itself — survival depends on what you do before it arrives.

Further Reading

The financial markets research team at Titan FX. We produce educational content across a broad range of instruments, including forex (FX), commodities (crude oil, precious metals, agricultural products), equity indices, U.S. stocks, and crypto assets.

Primary Sources (by category)

- Official records: U.S. Securities and Exchange Commission (SEC) — Lehman Brothers Examiner's Report (2010); Chapter 11 filing documents (15 September 2008).

- Government response: U.S. Treasury — TARP (Troubled Asset Relief Program) official documentation; Federal Reserve — Bear Stearns / AIG rescue rationale.

- Regulatory reform: H.R. 4173 — Dodd-Frank Wall Street Reform and Consumer Protection Act (2010); FSOC charter.

- Macro data: Federal Reserve Bank of St. Louis (FRED) — Dow Jones Industrial Average, S&P 500, and Nikkei 225 historical series for September–October 2008.

- Academic analysis: Brunnermeier, M. K. (2009) "Deciphering the Liquidity and Credit Crunch 2007-2008", Journal of Economic Perspectives.