Financing

Whether a company builds a factory, a household buys a home, or a trader applies leverage, there is always the same underlying question: how do you secure the funds? That is what financing is about.

This article lays out what financing means, its three layers, and the swap (overnight interest) mechanism that traders meet most directly in FX.

- Definition: Getting funds now in exchange for paying back later

- Three layers: Corporate financing, personal loans, and market leverage

- In FX: Not a loan — a daily settlement of the rate gap (the swap)

- Positive vs negative: Buy the higher-yield currency to earn, lower-yield to pay

- Triple swap: Usually charged on Wednesday to cover the weekend

1. What Is Financing?

Financing is the act of individuals, corporates, or governments borrowing or raising capital to support operations, investment, or consumption.

The core idea is trading time for capital — getting access to funds first, and returning value to the provider later in the form of interest, equity, or other returns.

At heart, financing is about the flow of capital and the transfer of risk. The party that needs capital gets it earlier to fuel growth or investment, while the provider gets paid through interest, equity, or other forms of return.

Financing is one of the mechanisms that keeps the economy moving. Whether it is a company borrowing to expand capacity, a government issuing debt to build infrastructure, or an individual taking out a mortgage or using consumer credit, these are all branches of the same idea.

It is not only about how to obtain funds, but also about the cost of funds, risk management, and the design of the return structure. As financial markets have evolved, financing has diversified from traditional bank loans to modern leverage, securitisation, and FX financing — but the underlying principle remains the same.

2. The Three Layers of Financing

The shape of financing changes with the borrower, the purpose, and the market context, but the core is always the same: how to obtain capital efficiently and put it to work in return-generating activity.

By the nature of the borrower, financing can be grouped into three layers — corporate, personal, and financial markets — each with its own logic and risk profile.

Type 1: Corporate financing

Corporates are among the largest participants in financing. To maintain operations, expand the business, or fund new projects, they raise capital through multiple channels.

- Debt financing: borrowing from banks or issuing bonds. Interest is paid periodically and principal is repaid. Control of the company is preserved, but financial leverage and repayment pressure increase.

- Equity financing: issuing new shares or taking on investors in exchange for capital without repayment. Fits growth-stage companies, but at the cost of equity dilution and potential investor involvement in decisions.

- Internal financing: reinvesting retained earnings into production and R&D — the most stable, lowest-risk source of funding.

Type 2: Personal financing

Personal financing mainly serves living and investment needs — mortgages, auto loans, student loans, consumer credit, and revolving credit card debt.

It lets individuals enjoy the benefits of an asset or education earlier, while taking on the corresponding interest cost and credit risk.

Type 3: Financial-market financing

In financial markets, financing takes on a clear leverage dimension. Traders use financing to scale up positions and improve capital efficiency.

Typical examples include "margin buying" in stock markets and margin systems in futures and FX.

This leveraged form of financing carries both heightened risk and amplified return potential — the next section unpacks how it actually works and what the funding cost looks like.

3. Financing in Investing and Trading

Building on the previous section, financing in financial markets has evolved beyond traditional borrowing into a capital-leverage mechanism.

Under this mechanism, traders can build a larger position without putting up the full capital, amplifying potential return — and accepting greater risk in exchange.

Unlike corporate or personal financing, the trading-side version isn't about cash-flow needs; it's about lifting capital efficiency and increasing positional flexibility. The mechanics differ across markets:

- Equities: investors can borrow from a broker (margin) to fund part of a position alongside their own capital.

- Futures: margin systems allow control of a full contract value with only a portion of the cash.

- FX: financing shows up as "overnight interest / swap" — not a literal loan, but a reflection of the interest-rate differential between two currencies.

So in FX, "financing" tracks the relative interest-rate change between currencies rather than money being borrowed from the market.

It can become a cost of carry (when the differential is negative) or a source of return (when the differential is positive) — a distinctive capital-turnover trait of FX markets.

4. FX Financing Cost and the Swap Mechanism

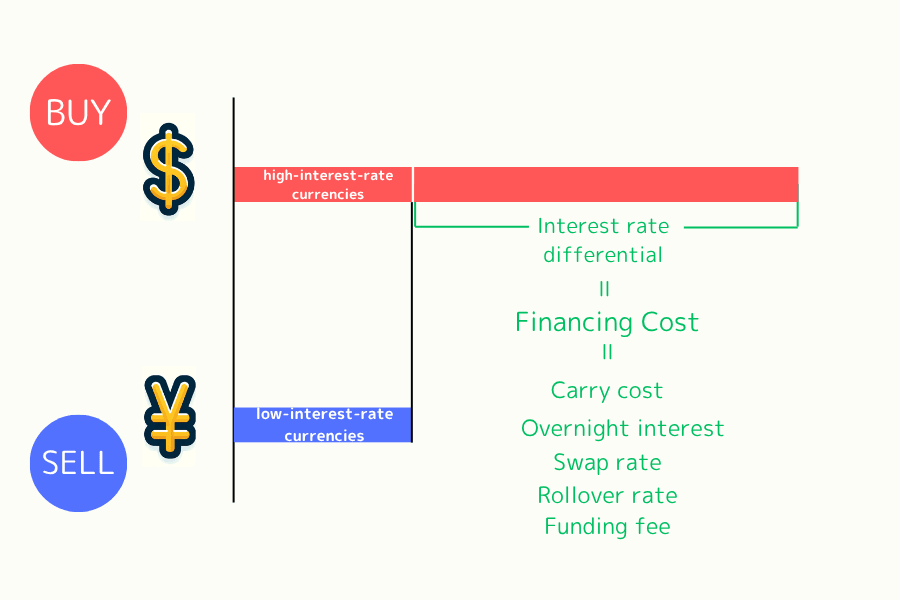

In FX, when a position is held overnight, the broker's system calculates a daily financing cost — also known as swap (or rollover) — based on the interest-rate differential between the two currencies of the pair.

FX trading always happens in currency pairs, so every transaction is simultaneously "buy one currency, sell another." Because each central bank sets a different policy rate, when a position crosses the daily cut-off, the system settles based on the two currencies' rate differential.

This settlement can be a cost or a credit, depending on direction and the rate gap:

- If the bought currency yields more than the sold currency, the trader can receive positive interest;

- If the bought currency yields less than the sold currency, the trader pays financing.

In other words, going long a currency pair in FX is effectively "borrowing the low-yield currency and depositing the high-yield one."

This daily settlement created by the two currencies' interest-rate gap is called the "swap point" or "overnight interest," and it moves with market rates, liquidity, and central-bank policy.

Why financing cost can turn into income

Once the mechanism is clear, it becomes obvious why a "financing cost" can sometimes generate income.

For example:

- Long AUD/JPY when AUD yields more than JPY is equivalent to borrowing yen and holding Australian dollars — a setup that can produce a positive daily swap.

- Short AUD/JPY reverses the operation — paying financing interest each day.

Using rate differentials between countries this way is known as a "carry trade." In low-volatility, stable markets, carry trades can deliver steady interest income — but when FX moves sharply or risk-off takes over, currency depreciation can wipe out the accumulated swap.

So in FX, financing cost is not just a cost of carry; it is a balance between return and risk. Used correctly, it lets traders adapt to different rate environments and improve overall efficiency.

5. Swap History and Practical Use

Swap values are not fixed. They shift with national rate policies, money-market conditions, and broker rules.

For long-term holders or traders who treat swap income as a strategy, tracking the historical data is essential for planning.

Broker differences

Different brokers use different calculation methods and rules, so the actual swap can vary even for the same pair.

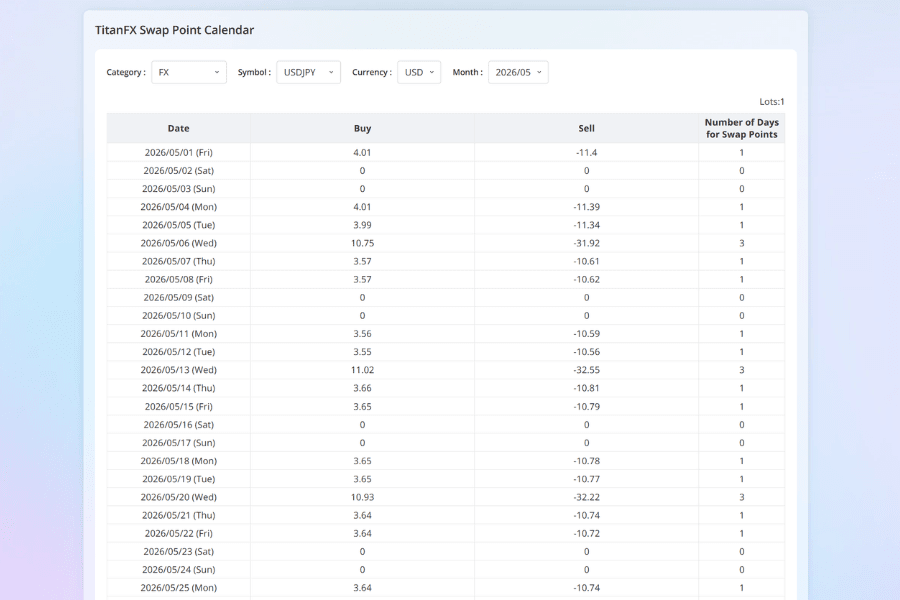

Titan FX historical data

Titan FX offers a detailed swap history, letting traders look up swap values for specific pairs on specific dates.

With the historical data, you can see "when" and "how much" of swap will be earned or paid, which helps with timing entries and exits.

Triple swap day

Most brokers credit three days of swap on Wednesday to cover the weekend. Missing this detail can produce unexpected gaps between projected and actual cost or income.

Example:

In USD/JPY, a single-day position may pick up around USD 7 of swap on a normal day but more than USD 21 on Wednesday (triple). For longer holds, planning around this cycle is part of basic discipline.

6. Frequently Asked Questions (FAQ)

Q1. Does financing cost (swap) apply every day?

Yes, whenever a position crosses the broker's daily cut-off (usually around New York close, GMT 21:00 or 22:00). Intraday entries and exits that close before the cut-off do not trigger swap.

Q2. How is equity margin trading different from FX swap?

Margin buying in equities means borrowing from a broker at a fixed interest rate (per the broker and market rules), and it's a one-way payment. FX swap is a two-way settlement based on the rate differential between two countries; it can be positive or negative depending on the pair and the direction.

Q3. Which pairs have the largest swap differentials?

Combinations of high-yielding, commodity-linked currencies with low-yielding funding currencies typically see larger swap — for example AUD/JPY, NZD/JPY, MXN/JPY, and ZAR/JPY. But a high swap usually comes with greater FX volatility, so the total picture matters.

Q4. Do central-bank rate moves immediately change the swap?

The direction transmits, but with a lag. After a central-bank rate change, interbank overnight rates respond first, and brokers typically adjust their swap basis within a few business days. The longer-term swap trend is driven by major central banks such as the Fed, the BOJ, and the ECB.

Q5. Does swap affect margin and the risk of being stopped out?

Yes. Swap is added to or subtracted from the account balance, which affects usable margin. If swap is persistently negative for a long-held position, it erodes the margin cushion day by day and indirectly raises the chance of forced liquidation. Before planning long-duration positions, it pays to estimate how cumulative swap will affect margin.

7. Conclusion

"Financing" is a broad concept, from corporate fundraising to personal loans to leverage in financial markets — all are extensions of the same idea.

In FX, it morphs into a daily settlement mechanism that is tightly bound to interest rates.

Understanding financing cost (swap) helps you correctly evaluate the return of a position and find new opportunities as global rates move.

For traders who care about steady operation and capital efficiency, getting comfortable with the principles of financing cost is one of the steps toward a more mature trading approach.

Further Reading

- What Is Swap / Financing Cost?

- What Is a Carry Trade?

- What Is FX Leverage?

- What Is a Currency Pair?

- What Is a CFD?

Titan FX Research Hub — investor education across foreign exchange (FX), commodities (oil, precious metals, agriculture), stock indices, U.S. equities, and crypto assets.

Primary Sources (by category)

- Academic and market basics: the three layers of financing, swap / rollover calculation logic, and the carry trade as covered in public references

- Central-bank policy sources: Bank of Japan (BoJ), U.S. Federal Reserve, European Central Bank (ECB)

- Market data and FX practice: BIS FX statistics, commercial-bank overnight (O/N) rate disclosures, and central-bank policy-rate releases