Carry Trade

In FX, many long-term traders are drawn to a strategy half-jokingly called "earning rent in your sleep" — the carry trade. The appeal is that it moves the core of the return from hard-to-predict price moves to something more concrete: the policy-rate gap between central banks. The textbook example is borrowing near-zero-rate yen to buy higher-yielding U.S. dollars or Australian dollars, then collecting a steady daily interest-differential payout.

That elegant-looking edge is, in practice, a psychological game against time and volatility. Daily swap interest does flow in, but the moment global markets wobble, a sharp FX reversal can wipe out the gains in days. This guide walks through the mechanics of carry trades from scratch and shows how to chase interest income while avoiding the blow-up trap.

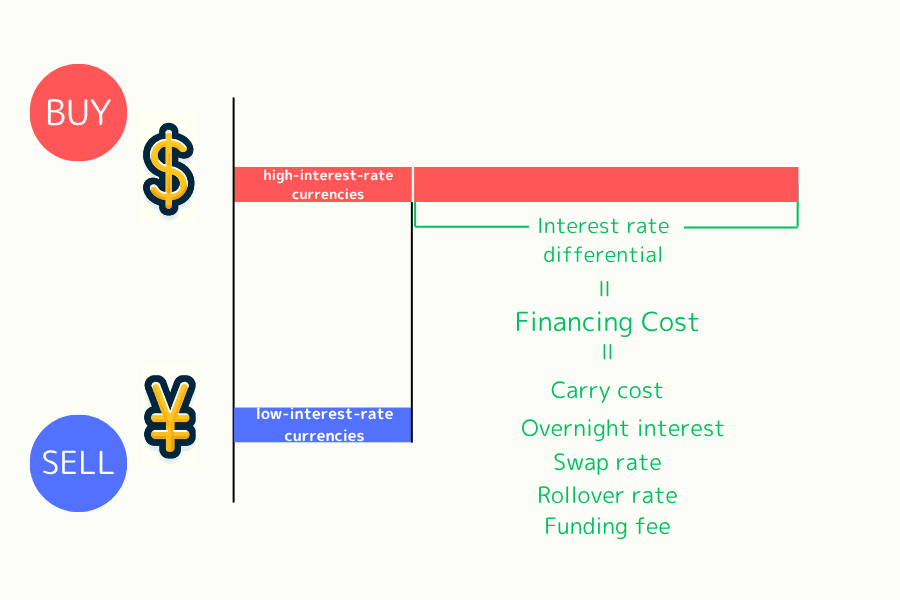

- Definition: A carry trade sells the lower-yielding currency (funding currency) and buys the higher-yielding currency (target currency) to earn the rate differential

- Two return drivers: daily swap interest (steady but slow) and FX-rate change (variable, can go either way)

- Marquee example: the yen carry trade — BOJ's long ultra-low-rate policy makes JPY the cheapest funding currency in the world

- Three blow-up triggers: FX reversal, high leverage forcing loss-cut, and central-bank policy convergence shrinking the rate gap

- Risk-management principles: cap leverage, watch Fed/BOJ policy, prefer high-liquidity major pairs

- 1. What Is a Carry Trade? Mechanics and Examples

- 2. Two Return Sources: Rate Differential and FX Change

- 3. Why the Yen Carry Trade Is the Most Famous

- 4. Critical Risks: Three Blow-Up Triggers

- 5. Practical Tips: Risk Management for Beginners

- 6. Frequently Asked Questions (FAQ)

- 7. Conclusion: Long-Term Strategy or Dangerous Game?

1. What Is a Carry Trade? Mechanics and Examples

A carry trade, sometimes called an interest-differential arbitrage, is an advanced FX strategy that aims to profit from differences in policy rates between currencies. The logic is straightforward: borrow the lower-yielding currency (the funding currency) and hold the higher-yielding currency (the target currency), capturing the gap.

In FX markets, this shows up as "sell the low-yielder, buy the high-yielder." As long as the exchange rate doesn't move sharply against the trader, holding the position lets interest income accumulate steadily over time.

How a rate gap becomes cash flow

Think of a carry trade as a cross-border interest swap.

If you can borrow at a very low rate (say 0.1%) and put the funds into an asset yielding much more (say 5.5%), the 5.4% gap becomes your net return — as long as the exchange rate stays stable.

In practice, you don't actually walk into a bank to arrange the loan. When you open a position with an FX broker, the system computes a daily swap (overnight interest) from the two currencies' rate gap and credits it to your account. That is what gives carry trades the "rent while you hold" feel.

A concrete example: USD/JPY carry trade

Take the most famous yen carry as the example. Suppose Japanese yen (JPY) policy rate is 0.1% and U.S. dollar (USD) is at 5.5%. Buying the USD/JPY currency pair is effectively "borrowing yen, depositing dollars."

- ▸How you earn: holding the position overnight, the platform credits the annualised ~5.4% rate gap into your account in daily slices.

- ▸Strategic role: in high-spread environments, this works as a "time-buying-yield" tool for medium- to long-term investors. As long as the dollar doesn't sell off sharply against the yen, you can earn both swap and potential FX appreciation.

2. Two Return Sources: Rate Differential and FX Change

Carry trades appeal to long-term traders because they can earn from both a cash-flow source and a price-move source at the same time.

Source 1: Swap — the steady "rent"

The swap is the core and the most stable return of a carry trade.

Interest in FX is not paid monthly — it accrues daily. If your position sits across a broker's settlement cut-off, the swap is credited (or debited) automatically.

As long as central-bank rates don't shift dramatically, this stream builds with holding time. Many traders treat it like "rent income from FX," a continuous cash flow that offsets part of the holding cost in medium- and long-term positions.

Source 2: FX appreciation — the upside layer

On top of swap, if the higher-yielding currency (say USD) appreciates against the lower-yielding one (say JPY), you also earn an FX gain when closing the position.

For instance, during a Fed hiking cycle, a stronger dollar can give traders the "interest plus appreciation" double benefit.

That upside, however, is uncertain. In a carry trade, the interest income is contractual but the FX risk is always floating. No matter how wide the rate gap is, if the higher-yielding currency's depreciation exceeds the swap collected, the trade ends in the red.

3. Why the Yen Carry Trade Is the Most Famous

Across all FX arbitrage strategies, the yen carry trade is the shorthand for the whole category. From global capital flows to hedge-fund positioning to crisis post-mortems, the yen plays a central role. That is not random — it reflects Japan's specific economic structure interacting with global risk sentiment.

The setup: the world's cheapest funding currency

The yen became the funding currency of choice because the Bank of Japan, fighting prolonged deflation, has maintained zero- or negative-rate policy for decades.

While major economies (the U.S., Europe, Australia) have hiked policy rates to fight inflation, JPY funding cost has remained the lowest in the world. That huge differential pulled global investors into borrowing yen at scale and rotating into higher-yielding USD or AUD assets — a massive cross-market arbitrage flow.

Market linkage: risk sentiment and yen buy-back waves

The yen carry trade isn't just a profit engine — it is a barometer of global risk appetite.

In risk-on phases, capital flows out of Japan seeking higher returns, weighing on JPY. When geopolitical risk or a financial crisis hits, risk-off forces arbitrageurs to "sell the high-yield asset and buy yen back" to unwind their debt — the so-called "carry-trade unwinding." That's why the yen often spikes sharply in turbulent markets.

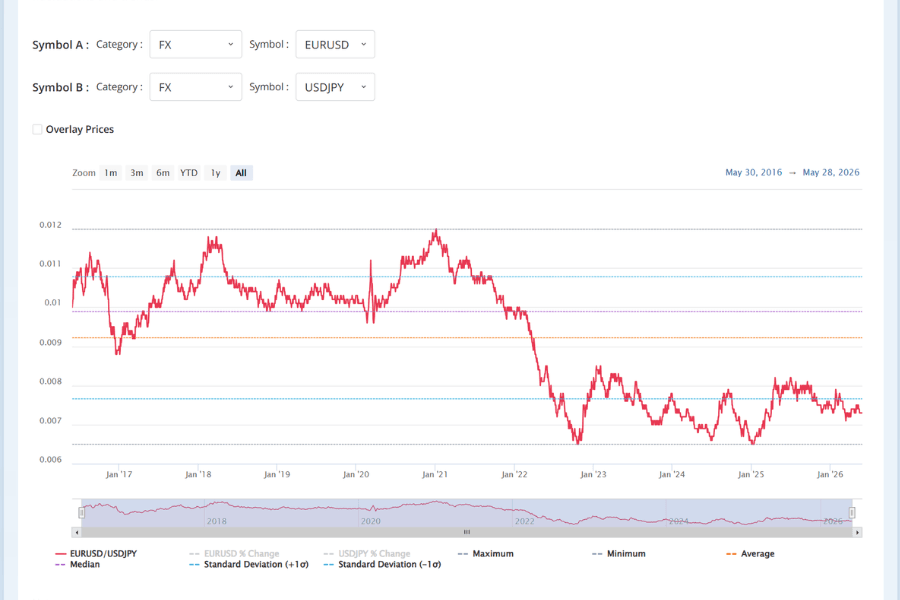

Practical tool: the Titan FX Arbitrage Checker

Finding a precise entry inside the noise of yen moves takes more than the rate gap. The Titan FX Arbitrage Checker offers a useful angle: it computes the ratio between two symbols (e.g. EURUSD and USDJPY) and visualises it as a chart, letting carry traders intuitively see relative strength and correlation between currencies.

Statistics such as the mean, median, and standard deviation help you judge whether the current ratio has drifted too far from its usual range.

When the ratio touches a standard-deviation boundary, the market is often overly optimistic or overly fearful — a useful signal for considering a reversal or scaling-up of the carry position. Data-driven entries reduce the chance of being caught on the wrong side once unwinding begins.

Arbitrage Checker4. Critical Risks: Three Blow-Up Triggers

A carry trade can look like a steady rent stream when markets are calm, but it is fundamentally a "short-volatility" trade. When the environment flips and volatility spikes, the damage tends to be brutal.

Risk 1: A sharp FX reversal eats the profit

FX moves are the most direct enemy of carry. The trader earns a rate gap, but the income drips in over a year.

Suppose the U.S.-Japan rate gap is 5%. If USD falls more than 5% against JPY in one week, even a full year of swap can't cover the FX loss. "Earned the interest, lost the FX" is the number-one risk that beginners miss.

Risk 2: High leverage triggers loss-cuts

Because swap is small in absolute terms, many investors use high leverage to amplify the return.

But leverage cuts both ways. At 20x, a 5% adverse move wipes out the account equity and triggers the broker's loss-cut (margin close-out).

The more dangerous scenario is when an extreme event sets off a carry-trade unwinding: capital floods back into the funding currency (yen), JPY rallies sharply in a short window, and high-leverage carry traders are loss-cut almost simultaneously with no time to react.

Risk 3: Central-bank policy convergence

A carry trade lives on the "moat" of the rate gap.

When the low-rate country (say Japan) starts hiking, or the high-rate country (say the U.S.) starts cutting, the gap narrows.

Once it narrows below what is needed to compensate for the FX risk of holding the higher-yielding currency, the logic that supported the trade breaks down. Arbitrage capital exits quickly, and those large flows often produce a sharp drop in the higher-yielding currency, triggering chain selling.

5. Practical Tips: Risk Management for Beginners

To survive in markets long-term, carry trading needs strict self-protection. The core of this strategy is "stay alive," not "earn fast," so risk management must outrank the search for the biggest rate gap.

Tip 1: Cap leverage and keep a margin buffer

A carry trade is, by nature, a slow strategy that trades time for space. Beginners are drawn in by the steady swap and tend to underestimate the principal-side pressure from FX moves.

Too much leverage prevents you from absorbing normal pullbacks and can loss-cut you on a short-term swing before swap has had time to accumulate. Set a reasonable leverage cap and make sure the account has enough margin to absorb sudden risk-off shocks.

Further reading: How to calculate FX margin.

Tip 2: Track central-bank policy and the spread trend

Carry returns rest on the rate gap between the two countries. Closely watch the rate decisions and macro releases from key bodies such as the Fed and the Bank of Japan (BoJ).

Shifts in the rate path — cooling hike expectations or the start of a cutting cycle — go straight into carry-trade structure. When policy convergence becomes visible, the moat is shrinking, so consider scaling down to lock in gains before the unwind starts.

Titan FX's economic-indicator data and economic calendar let you track central-bank announcements and key data in real time so you can prepare before the rate environment shifts.

Tip 3: Prefer high-liquidity major pairs

Not every wide-spread pair fits a beginner. Some emerging-market currencies offer very high yields but trade with sharp swings and serious political risk — the "earned 10% interest, lost 50% on FX" outcome.

For beginners, combinations among USD, JPY, and EUR are safer. Spreads are smaller, but FX behaviour is more predictable and easier to monitor with quantitative tools.

6. Frequently Asked Questions (FAQ)

Q1. Do I need a large account to run carry trades?

No. Micro-lot capability at FX brokers lets small accounts participate. What matters is whether your account can absorb FX swings, not the absolute starting size.

Q2. Why is the swap I receive smaller than the official rate?

Brokers deduct spread or fees from the swap, and overnight market rates move continuously, so the actual swap credited differs from the headline rate.

Q3. If two countries have the same rate, can I still carry trade?

If the rates are roughly equal, swap shrinks to about zero or even turns negative after fees. The pair has lost its carry-trade meaning — switch to a trend trade or look for another pair with a viable rate gap.

Q4. Are there famous historical "carry-trade unwinding" events?

Carry-trade unwinds usually flare up alongside global risk events. Two prominent cases: ①during the 2008 financial crisis, global investors mass-sold high-yielders such as the Australian dollar and the New Zealand dollar to buy back yen, and AUD/JPY fell tens of percent in a short window; ②in August 2024, a BoJ hike combined with rising Fed-cut expectations sent JPY up nearly 10% in days, triggering large loss-cuts in high-leverage carry positions worldwide. These episodes show that the speed of an unwind dwarfs the pace of swap accumulation — risk management must come before yield maximisation.

Q5. Beyond USD/JPY, which pairs work for carry trades?

Beyond USD/JPY, AUD/JPY, NZD/JPY, MXN/JPY, and ZAR/JPY — "commodity / high-yield currency versus JPY" — are traditional carry candidates. The rate gap is usually clear, but liquidity and political risk differ: AUD and NZD are relatively stable, while the Mexican peso (MXN) and South African rand (ZAR) move sharply and need stronger risk control. EUR/CHF-style carries thrived during low-EUR-rate eras but became less attractive after the ECB's hiking cycle compressed the gap.

7. Conclusion: Long-Term Strategy or Dangerous Game?

To sum up, a carry trade is not "lazy investing" — it is a specialised strategy that combines macroeconomic reading with a high level of risk discipline.

In stable risk environments with clear rate gaps, carry trades can deliver relatively stable cash flow and serve as a supporting engine in asset allocation. But when the world flips into risk-off mode, FX reversals tend to move far faster than swap accumulation, and over-leveraged traders are usually the first to be liquidated.

Before entering, use tools such as the Titan FX Arbitrage Checker and economic-indicator calendars for data-driven assessment, and keep leverage tightly capped. Only traders who keep a healthy respect for the market can turn carry trades into a long-term, durable source of yield.

Further Reading

- What Is Swap / Financing Cost?

- Bank of Japan (BoJ) Policy Schedule

- What Is the Federal Reserve (Fed)?

- How to Calculate FX Margin

- What Is a CFD?

Titan FX Research Hub — investor education across foreign exchange (FX), commodities (oil, precious metals, agriculture), stock indices, U.S. equities, and crypto assets.

Primary Sources (by category)

- Academic and FX-market basics: general public knowledge on the decomposition of carry-trade returns (interest differential + FX change) and the historical record of yen carry trades

- Central-bank policy sources: Bank of Japan (BoJ), U.S. Federal Reserve, Reserve Bank of Australia (RBA)

- Market liquidity and risk management: BIS FX statistics, public research on carry-trade unwinding, and overnight (O/N) bank funding-rate disclosures