Why Invest in the US Dollar: DXY, Fed Policy and Allocation Strategy

In the global financial system, the US dollar is far more than just the legal tender of the United States — it sits at the centre of international capital markets. The dollar's exchange-rate movements shape global trade, investment flows, and safe-haven demand, while feeding back into the monetary policies and economic stability of nearly every major economy.

In recent years, the Fed's interest-rate cycle, persistent inflation pressure, and elevated geopolitical risk have made the US dollar a top focus for both investors and policymakers.

This guide walks through the dollar's global role from a historical and current-market perspective, breaks down the structural drivers of its exchange-rate movements, and analyses the spillover effects on international markets. It also outlines how investors can adapt asset allocation strategies to dollar cycles in order to maintain stable performance across an uncertain macro environment.

- The dollar's status rests on three pillars. Reserve currency, trade settlement and commodity pricing.

- DXY tracks dollar strength vs. six major peers. Euro carries the heaviest weight at 57.6%.

- Four drivers move the dollar. Economic data, Fed policy, safe-haven flows and capital flows.

- Dollar cycles affect everyone. Emerging markets, commodities and US trade competitiveness all react.

- Allocate dynamically with DCA. Tilt toward USD in hike cycles, away during cuts.

- 1. The Dollar's Historical Background and Global Role

- 2. Why Invest in the US Dollar

- 3. Recent Dollar Trends

- 4. What Moves the Dollar Exchange Rate

- 5. How Dollar Trends Affect Global Markets

- 6. The Dollar Outlook Ahead

- 7. How Investors Can Adapt to Dollar Cycles

- 8. Frequently Asked Questions

- 9. Conclusion

1. The Dollar's Historical Background and Global Role

The US dollar (USD) is the cornerstone of the global financial system, a position built on decades of economic scale, institutional credibility, and policy coherence. The post-WWII Bretton Woods system pegged the dollar to gold and established it as the world's reserve and settlement currency. Even after the collapse of the gold standard in 1971, the dollar retained its leadership through the sheer size of the US economy and the depth of its financial markets.

Pillar 1: The bedrock of global reserves

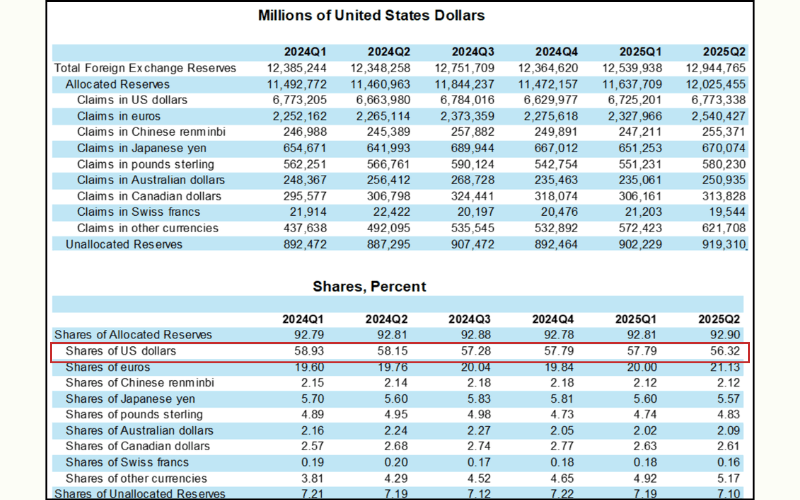

The dollar dominates the foreign exchange reserves of central banks worldwide. According to IMF Q2 2025 data, the dollar accounts for 56.32% of global reserves — well ahead of the euro and the Japanese yen. This share reflects both trust and structural influence over global finance.

Pillar 2: The default currency of trade and finance

Global trade settlement and major commodity transactions — including crude oil and gold — are overwhelmingly priced in US dollars. The depth and liquidity of dollar-denominated capital markets make it the default currency of international finance.

Pillar 3: Persistent long-term influence on exchange rates

Long-term moves in the dollar exchange rate reflect not just the state of the US economy but also global investor sentiment. Historically the dollar firms during Fed tightening cycles and softens when global liquidity loosens. This cyclicality forms the core rhythm of dollar trading.

2. Why Invest in the US Dollar

The case for investing in the dollar rests on its safe-haven characteristics, deep liquidity, and structural stability inside the global financial system. For investors, it is both a primary FX trading asset and a foundational component of asset allocation.

Reason 1: Safe-haven properties

The dollar is widely treated as a global safe haven. When markets get volatile or geopolitical risks escalate, capital tends to rotate into dollar assets, pushing the exchange rate higher. This makes the dollar a value-preservation tool during turbulent periods.

Further reading: What is a safe-haven currency? A guide to the main safe-haven currencies

Reason 2: Interest rates and the dollar are tightly linked

The single largest driver of the dollar is the US interest-rate level. When the Fed raises rates, dollar-denominated asset yields climb and attract global capital. When the Fed cuts, that yield advantage shrinks and capital often rotates into other high-yield currencies or risk assets.

The best-known gauge of the dollar's relative strength is the US Dollar Index (DXY) — a trade-weighted index of the dollar against six major currencies, based at 100 in 1973.

Reason 3: Diversification and currency-hedging effects

From an allocation perspective, the dollar provides global diversification that is hard to replicate with a single-currency portfolio. For investors based in other currencies, dollar-denominated assets can also act as a portfolio-level hedge during local-currency depreciation.

3. Recent Dollar Trends

Since 2020, the dollar has traced clear cycles around three large themes: pandemic shock, inflation surge, and geopolitical risk.

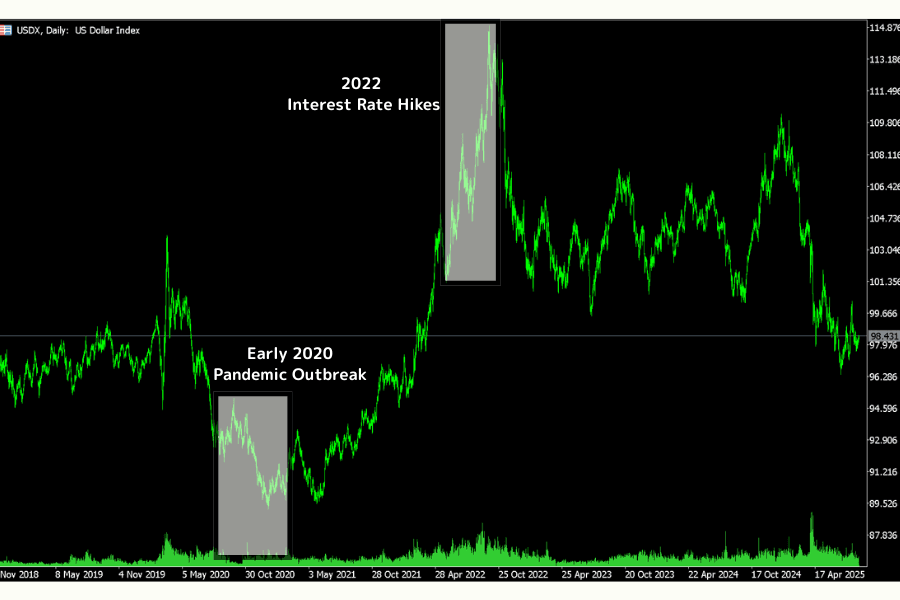

During the early pandemic in 2020, the DXY spiked to around 102 on a global dollar liquidity squeeze, then fell back to roughly 89 as the Fed launched aggressive easing.

From 2022 onward, the Fed entered an aggressive hiking cycle, pushing the DXY as high as 115. The widening US-Japan rate differential also drove USD/JPY past the historic 150 level.

Since May 2025, however, softer inflation, weaker pockets of economic data, and rising expectations for rate cuts have pulled the DXY off its highs and into a more volatile, downward-biased range. Investors are reassessing rate differentials between the US and other major economies, and dollar inflows have started to moderate.

Overall, the dollar has shifted from a high-level consolidation phase into a correction phase. The near-term direction will depend on the pace of Fed cuts and global safe-haven demand, with the dollar likely seeking a new equilibrium range in the short term.

4. What Moves the Dollar Exchange Rate

Dollar movements are never driven by a single variable. They are the product of multiple economic and financial forces interacting at once. The major drivers fall into four buckets: fundamentals, policy, capital flows, and market psychology.

Driver 1: Economic data and inflation

US GDP growth, inflation, and labour-market data form the core inputs traders use to read the dollar.

Strong data implies dollar-denominated assets are attractive and lifts demand for the dollar. Weak data — or signs of slowing growth — tends to weigh on the exchange rate.

Two indicators stand out: nonfarm payrolls (NFP) and the Consumer Price Index (CPI), both of which routinely trigger short-term dollar volatility.

Driver 2: Federal Reserve policy

The Federal Reserve (the Fed) directly influences the dollar through its interest-rate decisions.

Rate hikes lift dollar yields and pull in global capital, supporting dollar appreciation. Rate cuts compress those yields and tend to push capital toward higher-yielding currencies or risk assets.

Markets also pay close attention to the FOMC minutes and chair commentary, since the policy bias they reveal often previews the next leg of the dollar's move.

Driver 3: Global safe-haven demand

As the dominant reserve currency, the dollar carries clear safe-haven properties.

When geopolitical tensions, financial-market stress or liquidity squeezes intensify, investors tilt toward dollar assets for capital preservation. The 2008 financial crisis, the early stages of the 2020 pandemic, and the 2022 outbreak of the Russia-Ukraine war all produced strong safe-haven dollar rallies.

Driver 4: International capital flows and trade structure

US trade deficits and foreign holdings of US Treasuries also have a deep effect on the dollar.

Foreign buying of US bonds or equity inflows raise dollar demand and lift the exchange rate. Capital outflows or a widening trade deficit do the opposite.

Coordination — or divergence — in monetary policy between major economies and shifts in trade balances also influence the dollar indirectly.

5. How Dollar Trends Affect Global Markets

Dollar movements ripple through global markets, most visibly in emerging markets, commodities, and cross-border trade. As the world's principal reserve currency, the dollar's strength influences not just exchange rates and capital flows, but also trade costs and investor sentiment.

Effect 1: Capital flows in emerging markets

A stronger dollar pulls global capital toward US markets in search of higher yields, leaving emerging markets to face capital outflows and currency depreciation. In 2022, when the DXY peaked, currencies such as the Indonesian rupiah, the Korean won, and the Thai baht all came under pressure.

When the dollar weakens, the flow reverses: capital rotates back into emerging-market risk assets, lifting equity and bond markets and easing local liquidity conditions.

Effect 2: Commodity prices and inflation

The dollar and international commodity prices show a clear inverse relationship. When the dollar firms, dollar-priced commodities — gold, crude oil, copper — typically slip as they become more expensive for foreign buyers. When the dollar softens, those prices rebound and feed global inflation pressure.

During the 2022 dollar rally, Brent crude fell from roughly USD 120 per barrel to near USD 90. During the 2024 dollar correction, commodity prices broadly rebounded and inflation expectations reaccelerated.

Effect 3: Global trade and US competitiveness

A stronger dollar raises the price of US exports, weakens export competitiveness, and pressures domestic manufacturers — while simultaneously lowering import costs and helping to contain domestic price growth.

A weaker dollar tends to improve US export performance and boost multinational earnings, but it can also lift import costs and contribute to upward CPI pressure.

In aggregate, dollar moves are double-edged. For emerging markets and commodities, dollar strength often signals tighter liquidity and reduced risk appetite. For the US domestic economy, the strength of the dollar represents a constant trade-off between competitiveness and inflation control.

6. The Dollar Outlook Ahead

The future trajectory of the dollar will depend on Fed monetary policy, the global business cycle, capital-flow direction, and geopolitical conditions — operating together rather than in isolation.

If US inflation continues to cool and the labour market shows signs of weakening, the market's rate-cut expectations will deepen and apply downside pressure on the dollar. Conversely, if inflation stays sticky or growth remains resilient, the Fed may delay cuts or take a more hawkish tone — and the dollar could retain its strength or even resume its uptrend.

The global environment plays an equally important role. Rising geopolitical risk or financial-market stress can trigger safe-haven dollar buying. When global liquidity is generous and risk appetite recovers, capital tends to flow toward emerging markets and high-yield assets, and the dollar weakens. From 2025 onward, the gradual recovery of emerging markets and improving capital-market depth could see the dollar enter a more moderate correction phase.

The "de-dollarization" theme has gained attention, but its actual impact remains limited. The dollar still accounts for around 60% of global FX reserves and retains a dominant position in trade settlement, asset pricing, and cross-border payments. Until a credible alternative emerges with comparable liquidity and trust — or the US faces a structural institutional crisis — the dollar's core status is unlikely to be displaced in the short term.

Digital currencies and financial technology may also become a future structural support for the dollar. If the Fed advances a digital dollar (CBDC), the dollar's position in global payment infrastructure could be further reinforced.

In summary, the dollar may see a more volatile, mildly weaker stance in the short term, but its long-term strengths — US economic scale, market depth, and institutional credibility — remain intact. Even as global finance grows more multipolar, the dollar is likely to retain its core international role for the foreseeable future.

7. How Investors Can Adapt to Dollar Cycles

Investors facing dollar volatility and cyclical shifts should anchor on two principles: flexible allocation and disciplined execution. Strategic adjustments make it possible to capture upside while controlling risk.

Strategy 1: Pro-cycle allocation and risk diversification

When the dollar is in a strong phase, raising exposure to dollar assets — US Treasuries, dollar money-market funds, dollar-denominated bonds — captures the upside of dollar appreciation. At the same time, reducing emerging-market exposure helps limit losses from capital outflows or local-currency depreciation.

When the dollar enters a weak cycle, gradually rotating into non-dollar assets, gold, or silver and other inflation-hedge instruments diversifies away from currency drag.

Strategy 2: Track interest-rate cycles and policy signals

Fed policy is the core variable for the dollar. In a hiking environment, biasing toward short-duration bonds or cash makes sense. In a cutting cycle, the dollar's appeal weakens, and investors can add equities or high-yield credit to capture risk premiums.

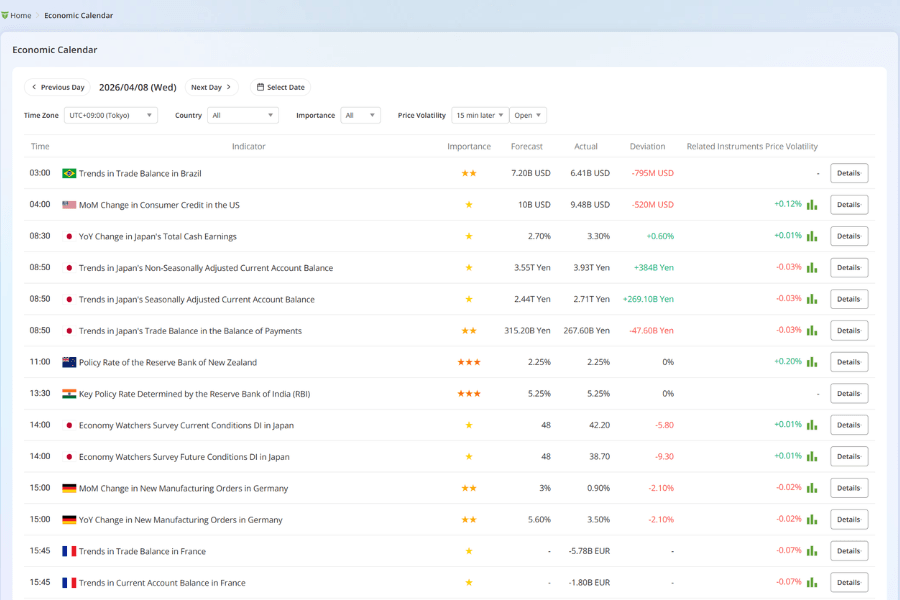

Equally important is monitoring the FOMC minutes and key economic data such as CPI and NFP, which often signal the next turning point in the dollar cycle.

Titan FX supports a global economic indicator lookup and provides a free economic calendar tool that displays release times and forecasts for major data — including GDP, CPI, and NFP — so traders can prepare for expected volatility.

Strategy 3: Risk management and disciplined execution

For FX or derivatives trading, always set take-profit and stop-loss levels so that a single trade cannot exceed your loss tolerance.

Medium- and long-term investors can use dollar-cost averaging (DCA) to build dollar positions gradually, smoothing entry cost and dampening short-term volatility.

Discipline matters above all else: avoid reacting to short-term price moves, and assess dollar trends through the lens of the underlying fundamentals over multi-quarter horizons.

Strategy 4: A global-view approach to asset allocation

Dollar moves are tightly linked to global market sentiment. Investors should track the dollar's relative performance against other major currencies (euro, yen, renminbi), combine the picture with global interest-rate differentials and business cycles, and only then design the allocation overlay.

Combining global diversification with dynamic rebalancing helps maintain portfolio stability and flexibility through dollar cycles.

Further reading: How to trade the US dollar

8. Frequently Asked Questions

Below are the most common questions investors raise once they begin tracking the dollar with a structured framework.

Q1. How does the US dollar maintain its position as the global reserve currency?

The dollar's reserve status rests on three pillars: the scale and depth of US capital markets, the predominance of dollar-denominated pricing in global trade and commodities, and the role of US Treasuries as the world's deepest safe-haven asset. According to IMF Q2 2025 data, the dollar still accounts for around 56.32% of global FX reserves — slowly declining, but with no credible near-term replacement.

Q2. How do I read the US Dollar Index (DXY)?

The DXY is a trade-weighted index of the dollar against the euro, yen, sterling, Canadian dollar, Swiss franc and Swedish krona, set at 100 in 1973. The euro carries the heaviest weight at roughly 57.6%, which is why DXY tends to track euro moves most closely. A rising DXY signals broad dollar strength against major peers; a falling DXY signals weakness. The DXY also moves inversely to dollar-priced commodities like gold and crude oil.

Q3. How does Fed policy shape the dollar exchange rate?

Rate hikes raise dollar yields and attract global capital, supporting dollar strength. Rate cuts do the opposite. But actual moves are also driven by market expectations — if a hike is already priced in, the actual decision can trigger a "buy the rumour, sell the fact" reaction. A robust read of the dollar usually combines FOMC minutes, CPI, and NFP rather than relying on the policy rate alone.

Q4. Is "de-dollarization" actually happening?

Although BRICS and other blocs have pushed de-dollarization themes, the actual impact remains limited. Dollar network effects in trade settlement, asset pricing and cross-border payments are extremely strong, and no alternative currency currently offers comparable liquidity and trust. Until a credible challenger emerges — whether the renminbi, CBDCs, or a structural US crisis — the dollar's core role is unlikely to be displaced in the short term.

Q5. How should an individual investor allocate dollar exposure?

The recommended approach is dynamic allocation paired with disciplined execution. In hiking cycles, tilt toward dollar assets (short-duration Treasuries, dollar money-market funds). In cutting cycles, reduce dollar exposure and rotate into emerging markets, precious metals, or non-dollar high-yield credit. Keep any single dollar asset below 30-40% of total portfolio, and use DCA to smooth entry cost so that one mis-timed call does not damage the portfolio significantly.

Titan FX Economic Calendar9. Conclusion

The dollar has long served as a central pillar of the global financial system. Its exchange rate not only reflects the state of the US economy and policy stance, but also drives global capital flows, trade balances, and market sentiment. Through every interest-rate cycle, inflation shock or geopolitical event, the dollar trace ultimately maps to the pulse of the global economy.

For investors, understanding the mechanics and long-term trajectory of the dollar is fundamental to building a global allocation. The dollar is not just a single-market signal — it is a real-time barometer of global risk appetite and capital flows. Only by combining fundamental analysis, policy reading, and market psychology can investors find a steady operating direction inside dollar cycles.

Even as the financial system grows more multipolar and de-dollarization narratives surface periodically, the dollar's scale, liquidity, and institutional credibility keep its leadership intact for the foreseeable future. Investors who can read dollar cycles and apply hedging and diversification strategies in step with them stand to capture greater autonomy in a shifting global environment — and to build a more durable long-term portfolio.

Further Reading

- US Dollar (USD) trading guide

- US Dollar Index (DXY) live rate

- What is a safe-haven currency? A guide to the main safe-haven currencies

- Titan FX Economic Calendar

- Forex fundamental analysis basics

Titan FX Research and Review Team — covering forex (FX), commodities (oil, precious metals, agricultural products), stock indices, US equities, and crypto assets, producing educational content for retail and institutional investors.

Primary Sources by Category

- Official data and regulators: IMF COFER (Currency Composition of Official Foreign Exchange Reserves, quarterly), the US Federal Reserve (FOMC Minutes / Beige Book), the Bank for International Settlements (BIS) Triennial Central Bank Survey on FX Turnover.

- Market data and liquidity: ICE U.S. Dollar Index (DXY) official methodology, Federal Reserve Economic Data (FRED) DTWEXBGS Broad Dollar Index, Bloomberg Markets (USD coverage).

- Academic research: Barry Eichengreen, "Exorbitant Privilege: The Rise and Fall of the Dollar"; Maurice Obstfeld & Kenneth Rogoff, "Foundations of International Macroeconomics" (chapters on the current account and exchange rates).

- Industry and third-party references: Investopedia (Dollar Index, DXY), Reuters (FX coverage), Titan FX in-house trading conditions and economic-calendar data.